Linkers surge on UK inflation shock: a British history lesson

The events surrounding Brexit have spun off many important lessons for markets, not least of which is the importance of considering all possible outcomes when assessing risk in financial markets.

One of the more obscure lessons of Brexit however is still very much in the making. This lesson relates to the rarely appreciated qualities of a peculiar backwater of the government fixed income universe, known as inflation linked bonds, or more affectionately, linkers.

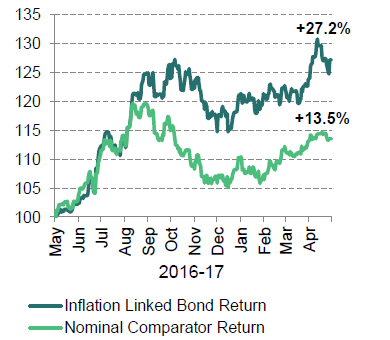

The lesson is simple enough: returns on UK inflation linked bonds have surged, with a currency-hedged return for Australian investors of 27% over the past year. Investors with unhedged currency exposure would have benefited even more from the UK Pound depreciation as well.

UK government bond returns (hedged to AUD)

Returns of this magnitude are rare for any asset class, and almost unheard of in the low risk, highly liquid government bond markets of the world’s safest and most stable sovereign countries.

The trigger for these bumper returns was a pronounced shift in inflation expectations, large enough to be called an inflation shock.

This is an event that has been seen only rarely in the history of financial markets, and hasn’t been observed in over 30 years, yet is also extremely damaging for investors.

The cause of this inflation shock was a sharp collapse in the value of the UK currency, pound sterling, as markets began to lower their expectations of economic growth in the Brexit aftermath. With the UK facing larger tariffs for its export goods, its currency will likely experience a drop in demand once Brexit occurs. This explains the fall in the current exchange rate.

The knock-on effect from a weaker currency is imported inflation: that is, a weaker exchange rate raises the price of consumer goods which, in the case of the UK and most other advanced economies, are largely sourced from abroad.

This expectation of a sharply lower currency, and sharply higher inflation in future, means that assets indexed to inflation can be expected to perform much more strongly than otherwise, resulting in the bumper 27% return.

Importantly, only inflation linked bonds provide direct indexation of their return to inflation.

Many other inflation hedges are available, such as property, infrastructure, and even blue chip equities. However these all provide a heady dose of high-growth exposure, which tends to drown out any inflation hedging they may offer.

For the specialist investors who trade government linkers, these developments are of great interest as they are rarely observed “in the wild.”

They also provide real-world proof of the unique properties of inflation linked bonds. Until now, these properties have been largely academic, as they haven't been observable in the universe of historical investment returns used to set return expectations.

Financial market historians know that one must look back a number of decades to the major inflation shock in the 1970s, or to emerging markets such as Zimbabwe, to identify earlier inflation shocks.

The applicability of these instances to modern advanced economies seems remote, so the recent experience of the UK is an important reminder that linkers can still deliver in spades for investors.

How was the 27% return on UK linkers achieved?

The 27% return on linkers deserves further elaboration given the sheer magnitude of the return on a low-risk government bond asset.

Inflation linked bonds pay a real yield and an inflation indexation, and as such their values are sensitive to changes in real yields and changes in inflation expectations.

A fall in real yields will make existing bonds with higher coupons more valuable, thus boosting their returns (and vice versa). Likewise a rise in inflation expectations will provide a larger indexation in future, also making existing bonds more valuable.

UK linkers benefited from both effects over the past year. Real yields declined by about 80 basis points, while inflation expectations rose by about 50 basis points (exact amounts vary depending on maturity).

Given the very long duration of the UK linker universe, at around 23 years, this was enough to deliver a 13.5% return from real yields, and a 13.6% return from inflation expectations.

Can the UK experience be repeated elsewhere?

The events in the UK may seem isolated, and not likely to be repeated elsewhere.

However, any long-duration linker market that experiences the same shocks to inflation expectations and real yields as the UK can expect to see similar performance outcomes.

This is comforting, as the UK experience provides evidence that inflation linked bonds perform exactly as expected in delivering robust protection against inflation surprises.

How likely this is in other markets such as Australia is something that will only be known in the fullness of time. That said, the tendency of the Australian dollar to trade the full range (and then some more for good measure) means that imported inflation should not be overlooked.

For this reason we continue to favour inflation linked bonds as providing almost bottomless inflation protection, in the event of a true inflation shock.

The starkly different performance on offer from linkers, especially in contrast to other growth-oriented inflation hedges, means they deserve worthy consideration in diversified portfolios.

As Brexit and the modern British history lesson has shown, one never knows when the unexpected can happen, and a 27% return might be just around the corner.

Ardea Investment Management

May 2017

The information in this article has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this article, whether express or implied, including the case studies, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Ardea Investment Management (“Ardea”) (ABN 50 132 902 722, AFSL 329 828), Fidante Partners Limited (“FPL”)(ABN 94 002 835 592, AFSL 234668) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, neither Ardea nor FPL nor any of their directors, officers, employees or agents accepts any liability (whether in negligence or otherwise) for any errors or omissions contained in this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional fixed-income investments because it is independent of the prevailing interest rate environment and how bond markets are performing.

Ardea IM believes the pure relative value opportunity set is a proven reliable source of returns because it is driven by structural market inefficiencies that create new relative value mispricing opportunities to profit from. Ardea IM focuses on delivering consistent volatility-controlled returns in order to strictly limit performance volatility and prioritise capital preservation, irrespective of the market environment.

2 topics

Ardea Investment Management

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional...

Expertise

Ardea Investment Management

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional...

Expertise

Comments

Comments

Sign In or Join Free to comment