Livewire's Christmas Cracker #1 - 'Next year will be electric'...

In our new 'Christmas Cracker' series, each morning through to Christmas we will bring you a top insight from one of our contributors. These will be diverse and could be a macro call, sector view, stock idea, or even some useful tech. Today's insight is from Romano Sala Tenna at Katana Asset Management.

Next year will be electric..!

As I wrote recently, 2017 will go down as the year that vehicle manufacturers’ commitment to electric vehicles (EV’s) transitioned from niche to mainstream. Vehicle manufactures from BMW to Volvo drew a line in the sand and irreversibly committed to a new paradigm. Yes this will take time to play out, but this thematic will run for more than 30 years.

In terms of the best way to capitalise on this theme, we believe that companies that produce copper, nickel, graphite, lithium and cobalt will all benefit. But it is this latter speciality metal, cobalt, that we think holds the most promise. The reasons behind this are now well documented: scarcity, concentration of supply and sovereign risk. 60-65% of all production is sourced from the DRC; 93% of which is for China.

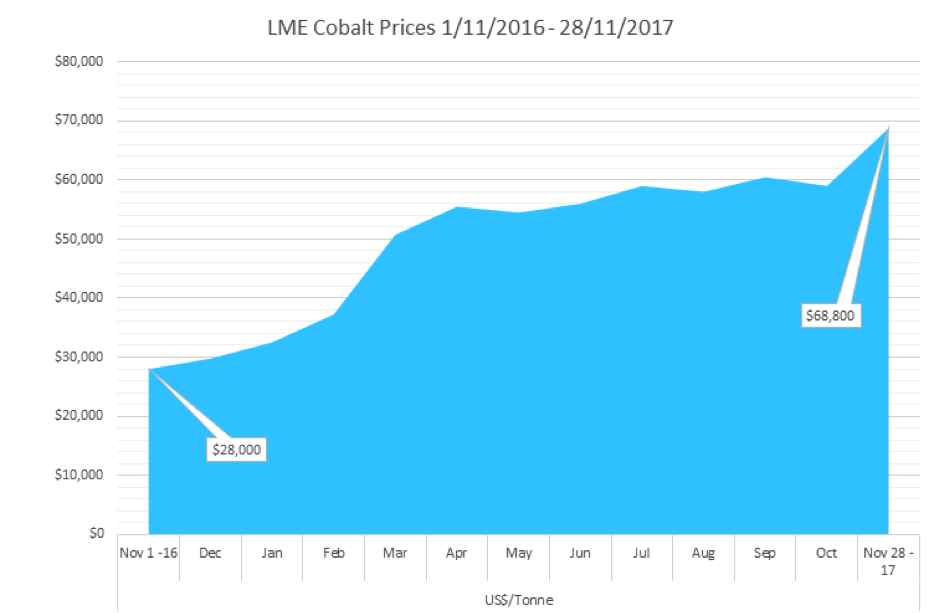

When combined with compounding demand, the outlook is extremely robust. At a growth rate of 10% per annum, the known reserves will be consumed in less than 19 years. If demand grows slightly faster, at 15% per annum, existing reserves will be consumed in just 15 years. And this realisation is being reflected in the price, which reached $US68,500 per tonne last week, to put it up by over 140% in a year.

Of course with most products, the cure for higher prices is higher prices; i.e. the strong returns on offer lead to a wave of new projects and supply. But cobalt is scarcer than any other commodity of note that we follow. And importantly, economically viable projects are even rare. Most deposits in Europe and North America have ultra thin ore widths, low tonnes and high levels of deleterious metals such as arsenic.

In the early stages of a major thematic this is largely irrelevant. All cobalt stocks with a reasonable market capitalisation and some good hits (however modest) are likely to appreciate rapidly, as they are now. But in the coming months, ‘serious’ investors will focus on those that are most likely to succeed through to production.

Two that stand out from the crowd

The first of these is Aeon Metals Ltd (AML), which owns the Walford Creek deposit north of Mount Isa. Walford Creek is the largest sulphide (copper) cobalt resource in Australia. This is a large-scale ore body extending over 20km and up to 300m deep. There is a high-grade core of 0.16% cobalt and 1.25% copper. Recent drilling results have been the best to date and are likely to add to the size of the resource.

The second company is Celsius Resources Ltd (CLA), which is less advanced but even more promising, as a pure play on cobalt. CLA is working towards their maiden resource in Namibia, where mineralisation has been intersected over 15km with potential strike of over 100km. This is a large-scale resource, with average cobalt grades tracking 0.13% to 0.17% plus copper credits of around 0.5%.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

1 topic

2 stocks mentioned

1 contributor mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management