Luxury Home Prices Tanking

In the AFR I reveal that luxury home values are tanking, particularly in ultra-high-end beach-side suburbs like Sydney's Palm Beach, and then unveil our new hedonic regression index for mortgage default rates---a global first---that shows that RMBS arrears are increasing sharply in contrast to what the likes of S&P claims via its SPIN Index for all public RMBS deals (click on that link to read for free or AFR subs can click here). Brief excerpt:

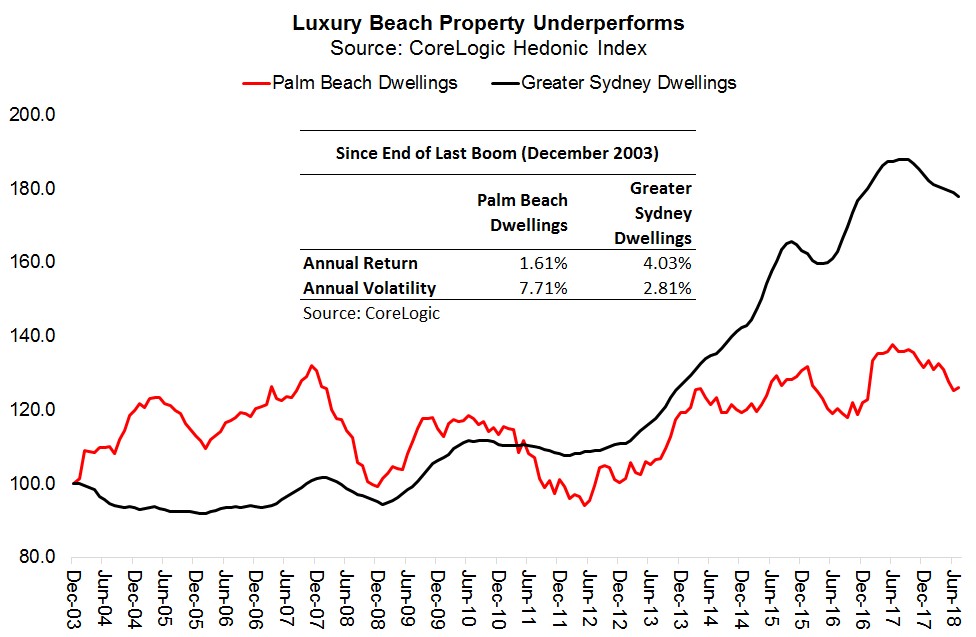

Since the end of the 2003 housing boom, Palm Beach property has delivered miserly capital growth of just 1.6 per cent annually (see first chart). If, on the other hand, you were diversified across Sydney, which has a median $1 million house price that is one-third the cost of the standard Palm Beach abode, you would have earned capital returns north of 4 per cent annually. That is, mass-market Sydney houses have provided 2.5 times the upside of their dearer “Palmy” counterparts.

It is actually worse than this. And that is because high-end housing is also riskier than the cheaper stuff precisely because it is a thinner market. There are, by definition, multiples the number of buyers that can afford to shell-out $1 million as opposed to $3 million.

This manifests in higher price variability: whereas Sydney homes display capital return volatility of only 2.8 per cent annually (assuming you have no leverage), Palm Beach properties exhibit volatility that is 2.7 times higher at 7.7 per cent annually.

Some might question whether this is good or bad volatility—one does not mind high returns if the downside is limited. Unfortunately, Palmy owners tend to suffer far worse during downturns.

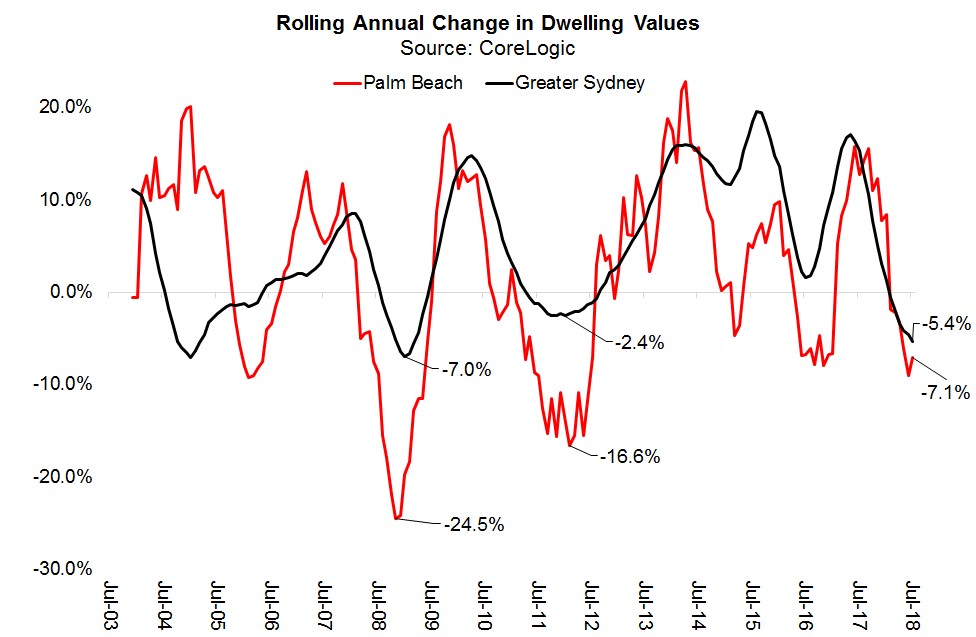

In the 2008 global financial crisis, Sydney homes lost 7 per cent of their value. In contrast, the Palm Beach holiday house market slumped a staggering 25 per cent. This was emulated again between 2010 and 2012: while the broader Sydney market only fell 2.4 per cent, Palmy property dropped 17 per cent.

Since the Sydney housing market peaked in September 2017 (we called the end of the boom in April 2017), the value of bricks and mortar has contracted 5.4 per cent. Palmy homes have followed suit, losing 7.1 per cent. If the last three downturns since 2007 are any guide, there is a decent chance Palmy properties will continue to free-fall until they have corrected some 15 per cent to 30 per cent.

These insights also hold when we examine the entire luxury market. Since 2003, the middle 50 per cent of homes ranked by value have outperformed the top 25 per cent by a cumulative 12.8 per cent in pure capital gain terms according to CoreLogic. If we used total returns the gap would be larger again given luxury homes typically provide terrible rental yields vis-à-vis median priced properties.

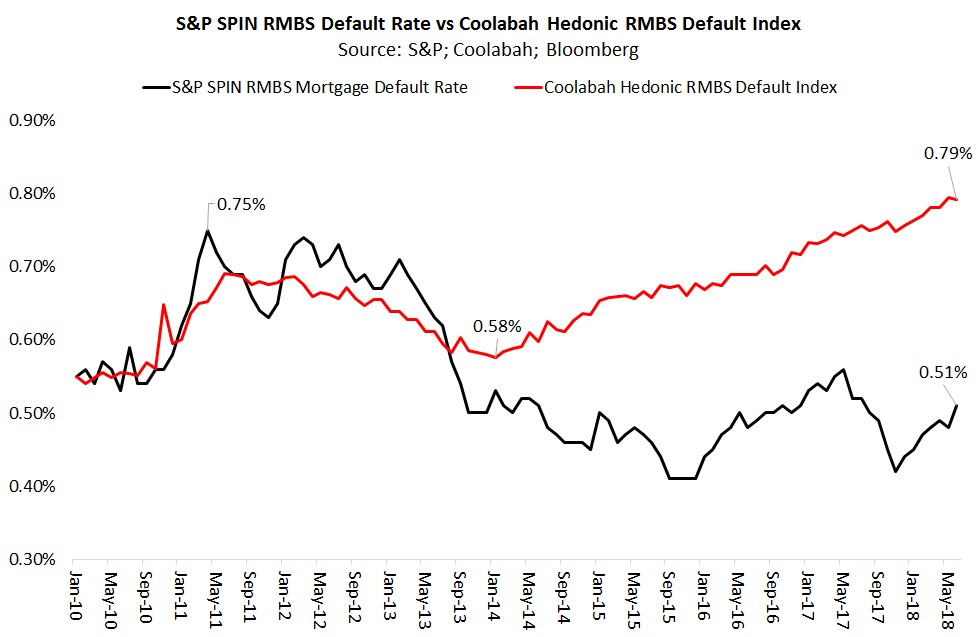

Hedonic models can be harnessed to address other interesting questions. There has, for example, been a huge surge in the supply (or issuance) of residential mortgage-backed securities (RMBS) in recent times. An RMBS bond is simply a portfolio of home loans originated by a bank or non-bank that is then sold to institutional investors.

When promoting these deals, banks and non-banks often cite the exceptional default performance of Aussie RMBS as documented by Standard & Poor’s index. According to S&P, the 90 day default rate on publicly issued prime RMBS deals in Australia has fallen from 0.75 per cent in 2011 to 0.51 per cent today. Many issuers crow about these benign numbers when trying to convince investors to part with their money.

We have several problems with these claims. First, they do not reconcile with the RBA’s data on 90 day default rates on all bank balance-sheets, which have been clearly climbing since 2015 from around 0.4 per cent to over 0.6 per cent currently.

Second, they are inconsistent with the demonstrable uptick in the major banks’ reported arrears.

Finally, we believe S&P’s data are afflicted by compositional biases akin to those that plague median house price indices. In every new RMBS deal the portfolio is initially default free (i.e. only performing loans are selected). Default rates then normally peak after about 3 years.

As the new deals are added to S&P’s RMBS universe, they artificially depress the reported default rates precisely because they are free of arrears. The same problem afflicts sales-based median price indices: if lots of cheap properties sell during the quarter, the index will report an artificial loss when prices could have been appreciating.

This source of bias is acute right now because the new supply of RMBS deals has boomed by a factor of four in 2017 and 2018 over levels recorded in prior years. Apparently bank balance-sheets and Japanese investors have been gobbling up the assets on the presumption they are nearly risk-free.

To address these concerns, I asked my data science team to build a new regression-based hedonic index for Australian mortgage defaults similar to the method CoreLogic uses for housing.

This index is based on public "prime" RMBS deals and controls for several key variables, including: the weighted-average life of the loans at the issue date; the weighted-average loan-to-value ratio at the issue date; the months since the RMBS deal was issued; and other factors.

In my final chart you can see that this hedonic RMBS default index, which is the first of its kind to be published globally, shows an unambiguous increase in the 90 day default rate for Aussie RMBS from 0.58 per cent in 2014 to almost 0.80 per cent today. While this contrasts strikingly with the decline in S&P’s index, it very closely maps over to the RBA’s time-series of defaults. (You would expect the level of defaults to be slightly higher than the RBA’s because of the presence of non-banks in the sample.)

Now it is important to point out that while this newly documented increase in Aussie RMBS arrears should give investors pause, the actual levels remain very low by global standards. And while I like RMBS as an asset-class, I am happy to stay out of the market for another 12 months until falling house prices, higher arrears, and the surge in supply forces spreads wider.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

3 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment