Making Italy Great Again

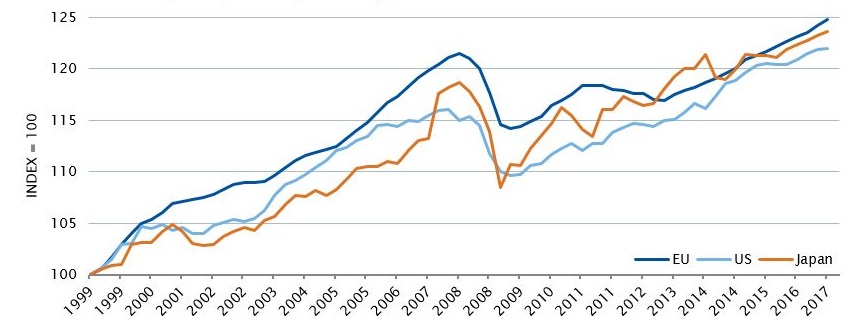

The European Union (EU) has often been described as an economic impossibility, however a conclusive and over-looked fact remains, that since the birth of the Euro, the EU has produced a better growth outcome than the US and Japan (Chart 1).

Chart 1: Real GDP per capita - EU, US and Japan

Source: OECD, Morgan Stanley

Observing only the experience of the past five years might lead to the conclusion that Europe is structurally flawed. However, this overlooks the 18 year history of superior growth in real GDP per capita. Within the larger picture of course there are smaller episodes of over and underperformance and although recency bias can dictate, we all remember post 2008. During that time Europe faced an unusually rare back to back recession with many of the reasons for the second recession being directly linked to policy errors specific to Europe. We have previously commented on some of the ways that Europe can overcome these short comings – ‘The million euro question facing the EU‘.

Firstly, the European Central Bank (ECB) initially failed in its role as the lender of last resort, providing insufficient liquidity to a banking system that faced solvency issues. Liquidity crises can take down solvent banks, but during the crisis the ECB reacted slowly and turned a controllable liquidity crisis into a potentially catastrophic solvency crisis. Secondly, and thereafter, the EU was slow to resolve solvency issues across its banking system and this led to a moribund recovery over the last seven years, which finally in 2016 turned upwards outpacing the United States in terms of real growth.

The US Federal Reserve (or Fed) and Treasury were much quicker to react in 2008 and better understood the risks within the shadow banking systems. The Fed’s quantitative easing (QE) program became essentially an asset transfer mechanism whereby the Fed created liquidity and transferred this to the banking system via large scale purchases of US government bonds. Bank solvency was managed through the US Treasury’s injection of public funds into the balance sheets of large US banks.

As mentioned above the Chart 1 above illustrates that the EU has produced a better growth outcome than both the US and Japan. We like to use real growth per head because it actually determines wellbeing and living standards and the best resolution mechanism of indebtedness for a society as a whole. High nominal growth via inflation may sound appealing to a highly indebted society, but it misses the point that one person’s debt is another’s asset. Inflation reduces the burden on debtors by robbing creditors – not a great longer-term wealth creation outcome.

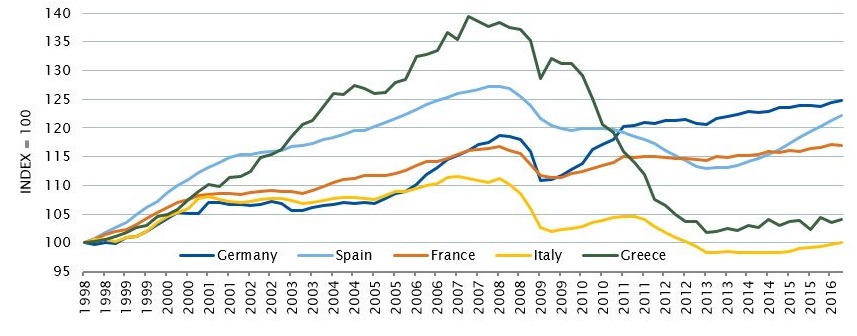

Chart 2: Real GDP Per Capita

Source: OECD, Morgan Stanley

Chart 2 illustrates real GDP per capita for several European countries and tells us a very interesting story, where some countries over time have lagged. Very interestingly in the early periods of the Euro, Germany lagged due to a combination of high unemployment from the post reunification phase which led Germany to enact sweeping structural labour reforms in 2002 to improve competitiveness (in 2015 Italy modelled it’s version of labour reform on this German framework). But post the GFC, the recovery in both Italy and Spain lagged as seen in the real GDP per capita chart.

However, in 2013 Spain achieved a remarkable recovery in real GDP per capita whilst Italy unfortunately did not. Spain through the assistance of the European Union rebuilt the capital positions of its banking system.

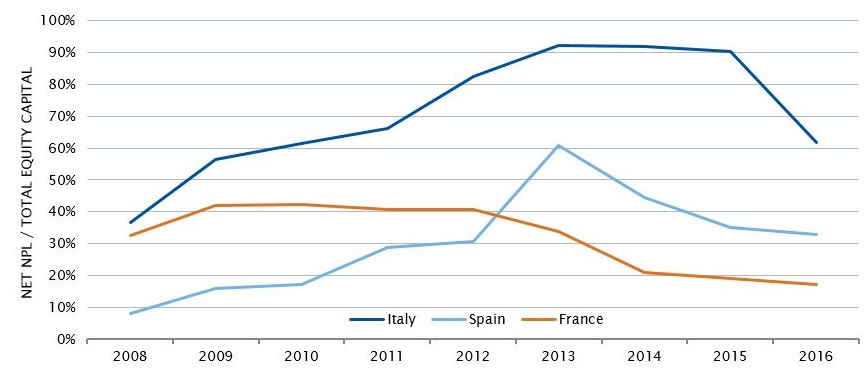

Examining net non-performing loans (NPL) to the total equity capital in the banking system demonstrates that Spain managed to restore solvency, something that has alluded Italy until now. Based on our calculations, Italy required approximately EUR55 billion of additional capital to restore confidence and health. Through a combination of private and public market solutions, Italy has finally restored solvency albeit at a snail’s pace. It would be a bold statement to say the Italian banking system is now healthy but it’s far closer to being so than it was in the past.

Chart 3: Net NPL / Total Equity Capital

Source: Bloomberg

Italian net NPL to total equity capital is now at the same point it was for Spain in 2013 (see Chart 3). Whilst this doesn’t guarantee that Italy will exhibit the same growth trajectory, it is important to recognise that the obstacles to growth are being lowered at a time when market sentiment towards Italy is still very negative.

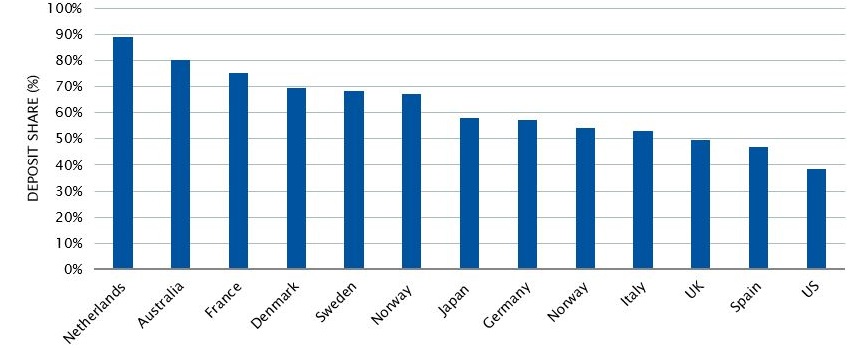

For example, through the process of raising capital and forced mergers, the Italian banking system is now more consolidated compared to Spain (see Chart 4).

Chart 4: Deposit Market Share of Top 4 Banks (%)

Source: BAML

For over 18 months Antipodes Partners has been highlighting the opportunities within European domestic industries and, in particular, the banking sector. ING Groep has been a core outperforming holding within portfolios and European banks now on average are priced at ~1.1x Book (see ‘ING Groep – a leader in digital distribution‘). Italian banks, however, remain at a significant discount, trading at ~0.7x Book, reflecting thus far lacklustre growth and ongoing “tail risk” concerns. Growth recovery will be critical for Italy now and would further help Italian banks build further capital and continue the recovery.

Antipodes Partners’ Italian bank portfolio exposures include Unicredit and Mediobanca with each business highly differentiated in its own right.

To learn more about Antipodes Partners, visit antipodespartners.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed Fund) active-ETF (ASX: AGX1). Through these vehicles, investors can access portfolios of attractively priced global businesses with strong long-term growth prospects. Antipodes was established in 2015. The investment team operates from offices in Sydney and London.

2 topics

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed...

Expertise

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed...

Expertise

Comments

Comments

Sign In or Join Free to comment