Market correction: What does it all mean?

Craig James

CommSec

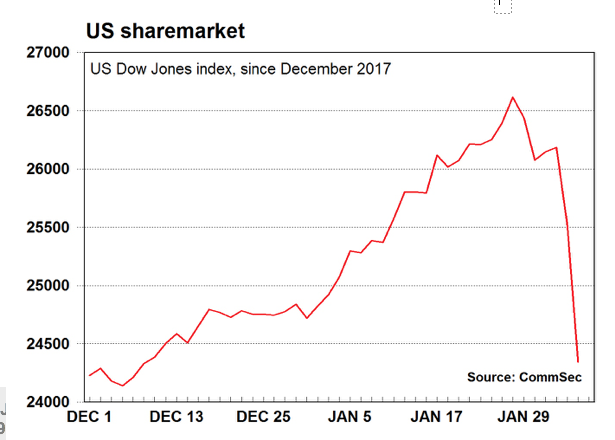

The US Dow Jones has fallen by over 1,800 points or 7.1 per cent over the past two days. After hitting record highs on January 26, the Dow Jones index has eased to 2-month lows.

What do the figures show and what does it all mean?

Some would say that it has been a long time in coming. That is, a pull-back in the US sharemarket after stellar gains for months. Well on Friday that pull-back started and it continued on Monday. The Dow Jones has now fallen by over 1,800 points or 7.1 per cent. So where does that take the market back to? Actually only to the levels of December 8, around a two-month low.

So what has prompted the declines for key US share indexes – declines that have spread to other markets in Europe and Asia? One influence was the latest US jobs report. US non-farm payrolls (employment) rose by 200,000 in January, ahead of forecasts for an 180,000 gain. The jobless rate was unchanged at 4.1 per cent as expected. But the key result was wages or average earnings, up by 0.3 per cent after a 0.4 per cent gain in December. That put annual wage growth at an 8-year high of 2.9 per cent.

That’s right, strong US economic data was one factor prompting a sell-off in stocks. The worry was that stronger wage growth could lead to higher prices (inflation). And that could lead the Federal Reserve to be more aggressive in lifting rates.

Now higher interest rates aren’t necessarily bad news if prompted by a stronger economy. But if rates rise it could lead to slower consumer spending, slower demand for new homes and slower growth in profits, thus affecting share prices. Here the concerns relate more to the Federal Reserve hiking rates too aggressively, thus slowing the economy too much. If the rate hikes are measured, keeping economic growth and inflation on a sustainable footing, it is actually a positive development.

Also in terms of the sell-off it has to be remembered that US shares were priced for perfection at around 19 times earnings. The more ‘normal’ relationship is for shares to be around 15 times earnings. Still, US companies have produced stellar earnings over the reporting period. So it is understandable that some ‘irrational exuberance’ would emerge.

Thomson Reuters notes that half of the S&P 500 index companies have reported earnings. So far 78 per cent have beaten expectations whereas a more normal season is for around 64 per cent to beat forecasts. Analysts now believe that fourth-quarter earnings will be up 13.6 per cent on a year ago, up from 12 per cent on January 1.

It’s also worth noting that the bulk of the high-profile companies have now reported earnings. On Thursday, Apple, Amazon and Alphabet (parent of Google) all reported earnings after the bell (close of trade). Exxon Mobil and Chevron reported earnings on Friday.

As noted, earnings growth has been good. But investors question whether the good times will continue at the same pace or whether now is a good time to book some profits. And that makes sense – there are fewer good reasons to buy, but some reasons to sell.

Take Apple, its latest quarterly revenue was US$88.3 billion, an all-time record and up 13 per cent on a year ago. Cash levels lifted to a record US$285.1 billion. But Apple shares fell 4.3 per cent on Friday. Analysts were disappointed with product sales and the forecasts for future sales. In short, analysts wanted more.

What are the implications?

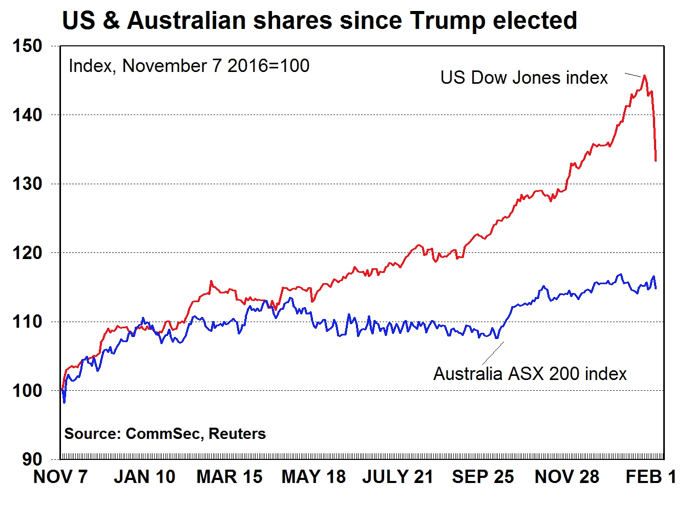

The Australian market – like many other global sharemarkets – has under-performed the US market over the past year. And sharemarket valuations are less lofty in Australia. Still, as was shown on Friday, the old-adage still applies: ‘when the US sharemarket sneezes, the rest of the world catches cold’.

The important point is that economies are in far stronger shape than they were a year ago or five years ago. Economies are growing at a faster rates and profits are rising. Technology is driving down costs and cheaper prices for a raft of goods are buoying consumer purchasing power.

The Aussie dollar eased to below US79 cents and the weaker currency (down from recent highs above US81 cents) will assist exporters and globally-focussed companies.

The Reserve Bank meets today. Rates will remain on hold. If new problems were to arise in the global economy, the Reserve Bank is well placed to cut rates. But the chances of rate cuts are still low. The concern for the Reserve Bank has been the slow growth of wages and prices. If a little more inflation was to emerge in the US and spread across the globe, it would be considered a positive, not negative, development.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth Securities, interpreting big picture economic and financial trends for customers, clients and staff. Previously I was Chief Economist at Colonial and have worked at the Australian Financial Review as a senior writer.As well as providing presentations to staff and clients and commentaries on financial and economic trends, I appear regularly in the electronic and print media.I have worked in banking, finance and journalism for 38 years.I hold both Bachelor and Master degrees in Commerce (Economics). Both degrees were undertaken at University of NSW. I am an Adjunct Professor at Curtin Business School in Perth.

2 topics

Craig James

Chief Economist

CommSec

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth...

Expertise

No areas of expertise

Craig James

Chief Economist

CommSec

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment