Market risk rises as bitter battle unfolds

The upcoming U.S. Presidential election poses significant ‘event risk’ for global financial markets. This note examines some of the risks and opportunities investors need to be aware of.

Elections are typically a time for caution

United States Presidential elections are held on the first Tuesday in November every four years. Accordingly, the 59th Presidential election will take place on Tuesday 3 November – or in just over one month. At the same time, all seats of the House of Representatives will be contested, along with 35 of the 100 seats in the U.S. Senate.

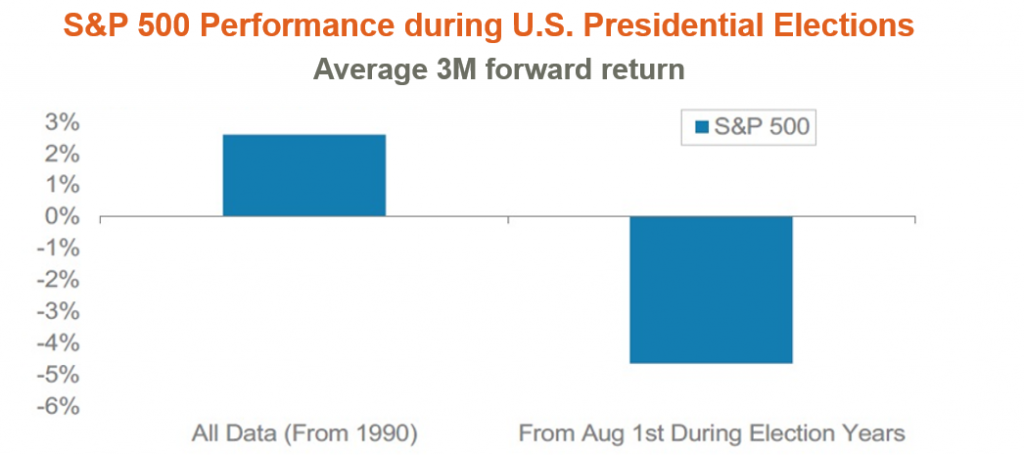

As seen in the chart below, long-run history suggests these election periods are, on average, a time for caution.

Source: Bloomberg, Morgan Stanley Research; Note: we exclude 1996, where polls were never close over the course of the summer prior to the election. Past performance is not indicative of future performance.

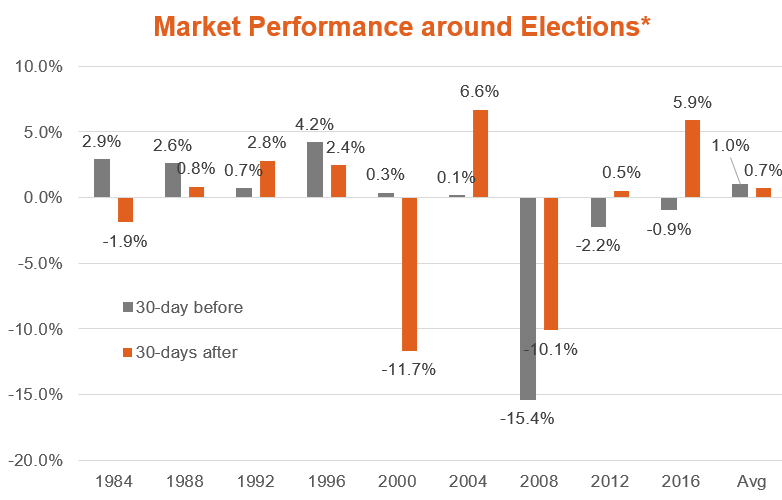

That said, recent history is more equivocal. As seen in the chart below, over recent decades average market performance in the lead-up to an election has not been that much different than the weeks following an election (in fact the average return before the election has been slightly greater). Note, this analysis excludes 2008, when equities were already suffering through a major bear market.

Source: Bloomberg. Average excludes 2008.

As also is evident in the chart above, however, two clear exceptions are 2000 and 2008.

In 2000, stocks slumped by 11.7% in the month following the election, reflecting a period of lingering uncertainty as to the Presidential election result due to court challenges over the legitimacy of certain votes.

In 2008, stocks continued to decline, due both to ongoing economic weakness associated with the global financial crisis, and also because no further fiscal stimulus could be provided until Washington could meet and agree on new legislation in the new year.

2020 risks a combination of both 2000 and 2008 outcomes

This time around, markets face a risk of some combination of both the 2000 and 2008 outcomes. As in 2008, the U.S. economy is in recession and most economists argue more fiscal stimulus is needed. Yet so far at least, Washington has failed to agree on a new support package, and there is a growing risk that more stimulus will now not be possible until the new year when the new President and Congress are sworn into office.

At the same time, there is also a risk of a period of extended election uncertainty if there are court challenges following the vote. In 2000, the Presidential election result was very close, and the Republican party contested the legitimacy of voting cards in certain districts on the basis that they had not been properly completed. Indeed, the term ‘hanging chads’ became famous as the legitimacy of certain punch-hole voting cards was questioned, given the relevant holes had not been completely perforated.

Today, risk is with regard to postal votes, given that they will figure more prominently than usual in this election due to COVID-19 and because the rules relating to what is a valid postal vote can be complex and vary by State – opening up the possibility of legal disputation. Certainly, President Trump seems to be already preparing himself – and the nation – for a fight, declaring “the only way we’re going to lose this election is if this election is rigged.” He has also so far refused to say he will accept the election result, suggesting instead “we’re going to have to see what happens.” He has also explained his desire for a quick appointment of a new Supreme Court judge by arguing “I think this [election] will end up in the Supreme Court…and I think it’s very important that we have nine justices.”

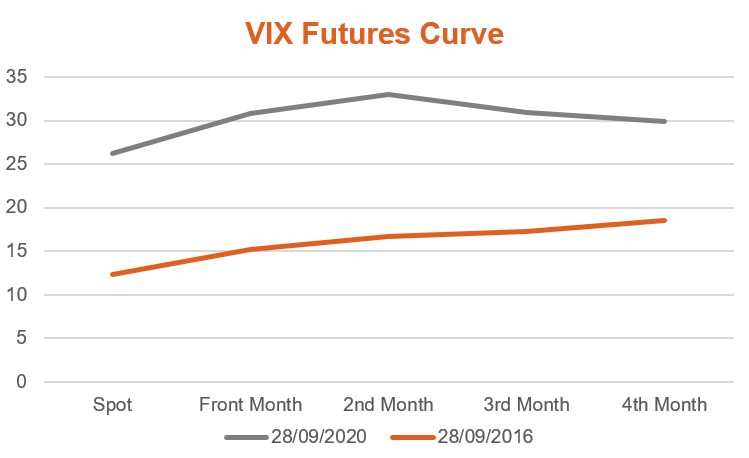

As seen in the chart of S&P 500 VIX futures below, the market has already priced in somewhat more ‘event risk’ around the time of this election than in 2016.

Source: Bloomberg.

The polling remains close

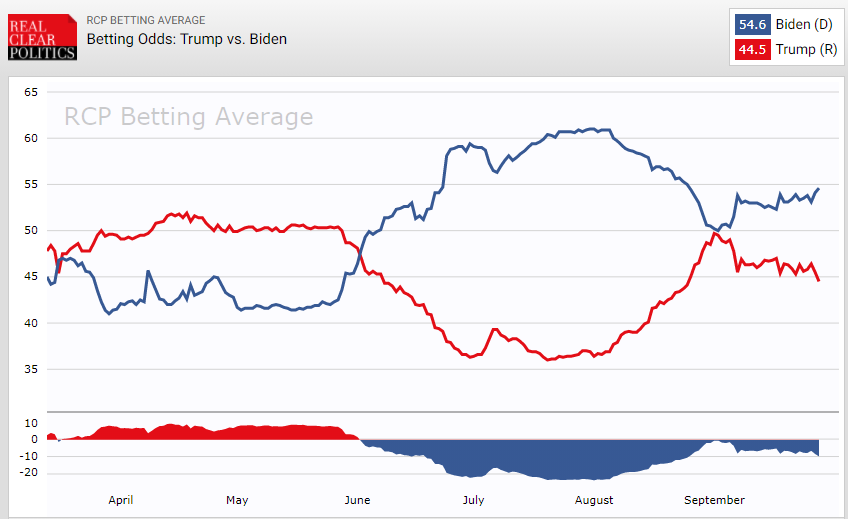

Most polls suggest Joe Biden is the favourite to win the election – but polls were wrong in 2016 and even if they are more accurate today, sentiment can still change in the weeks ahead, as the economy evolves and the U.S. sees how the candidates fare in both the three televised debates and on the campaign trail.

Indeed, odds within betting markets have moved notably in recent months – from Trump being favourite to being a long shot. The odds narrowed markedly by early September, but have since widened again in Biden’s favour.

[Hot off the press – the 1st debate has just been concluded and it seems Biden held up better than many feared – which should improve his odds a bit further].

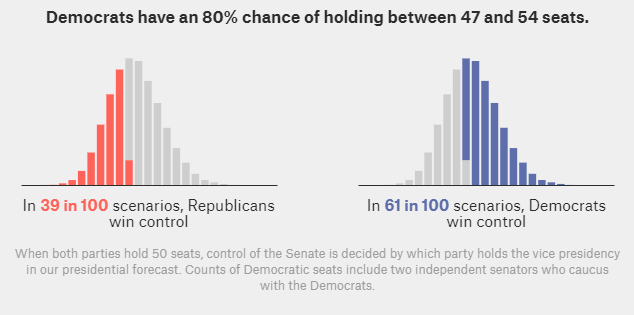

The Senate is also critical

Of course, not only is the Presidential election important – but also that of the Senate. While the House of Representatives appears likely to remain in Democrat control, the Senate’s current Republican majority is under threat. According to a review of national polls by notable forecasting website FiveThirtyEight, the Democrats are on balance (60% probability) expected to win control of the Senate, but the race remains tight.

Senate Polling

Source: FiveThirtyEight.com

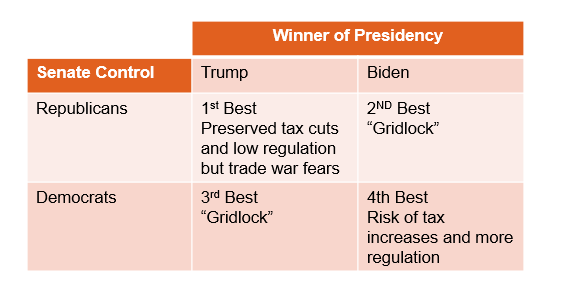

Best and worst case market scenarios

From a purely market or investor perspective, while an extended period of uncertainty and court challenge is the most immediate worst-case scenario, the ultimate best scenario would most likely be if the status quo ultimately prevailed i.e. Trump retained power and the Republicans controlled the Senate. That’s because this would preserve the Trump corporate tax cuts and reduce the risk of more industry regulation – particularly in the dominant technology sector.

That said, a Trump re-election may lead to some market concerns about a re-instigation of U.S.-China trade tensions – though it remains to be seen whether Trump will have much appetite for this issue once it is no longer needed for political purposes.

Markets would most likely be more concerned if current polling is correct – and the Democrats win a clean sweep of both the Presidency and the Senate. The good news is this would likely bring forth major new fiscal stimulus in the new year (directed at households), though it could lead to longer-term concerns that some of the corporate tax cuts under Trump could be reversed. The Democrats will also consider tougher restrictions on technology companies in the area of data privacy and competition.

Last but not least is the intermediate position of Biden wining the Presidency but the Republicans retaining control of the Senate. This is likely the second-best alternative for markets, as it will return Washington to gridlock – and likely reduce its market influence to the usually low levels that prevailed prior to Trump.

Likely best and worst case market scenarios

Ultimately, however, markets learn to live with whoever is U.S. President. Even if the Democrats do enjoy a ‘clean sweep’, the biggest influence on the market in 2021 will continue to be evolution of the economy and COVID-19.

Never miss an insight

Each week I will publish my latest thoughts on the macro events shaping the ETF landscape. To be the first to read my insights, hit the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment