Millenium Services - A Stock on a PE of 3

It’s been a while since I bought a stock trading on a PE multiple of 3x. There was one in 2012. Another in 2015. Both were, with a bit of luck, multi-baggers.

Maybe they show up every three years because if Millenium Services Group (ASX:MIL) hits it's FY19 guidance then the stock is trading on a PE of 3x.

That kind of value can compensate for a lot of less than ideal characteristics, of which MIL has its share. It comes with the territory of buying stocks that are this cheap.

But it means the company doesn’t have to do much for the stock to re-rate. If they can hit FY19 guidance, generate the same level of cashflows they’ve generated in the last two years and pay down some debt, then MIL has a real shot at being a multi-bagger.

Here’s why I think MIL looks interesting.

![]()

The Millenium Story

MIL provides commercial cleaning and security services to blue chip property owners across Australia and New Zealand. Scentre Group, Lend Lease, JLL, QIC, Stockland, AMP Capital, Mirvac, Apple, Myer – essentially all of the big names are clients.

It’s a fairly unexciting, low growth industry having grown at about 2-5% per annum over the last few years. 90% of revenue is contracted over 3-5 years (with options to extend) providing good visibility.

Since all clients are blue chip, bad debts are essentially nil. The tricky part is managing working capital – payment terms are monthly but if a Scentre Group or Lend Lease want to hold out on their bill for a week or two there’s probably not much you can do.

So it is a decent business when run well and should be a strong cash generator, as it has been in recent years.

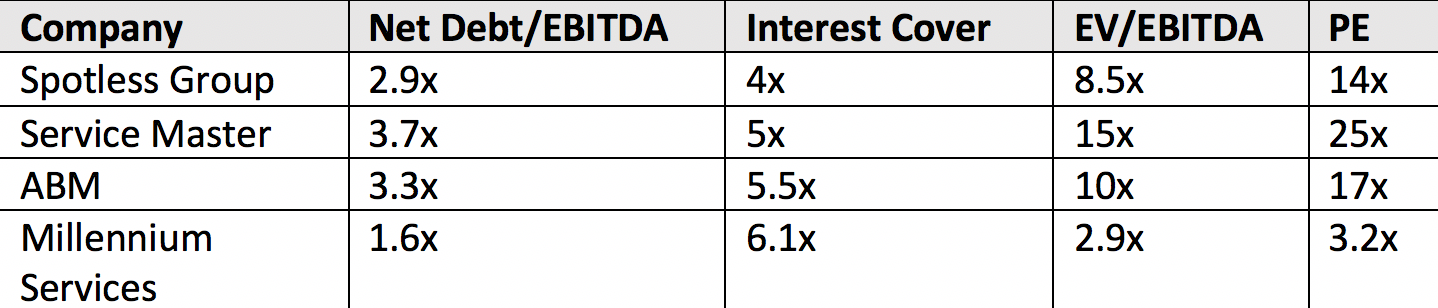

You’ll find plenty of comparables that trade on market multiples. Downer (ASX:DOW) paid ~14x NPAT for Spotless (ASX:SPO), or 12x EV/EBIT.

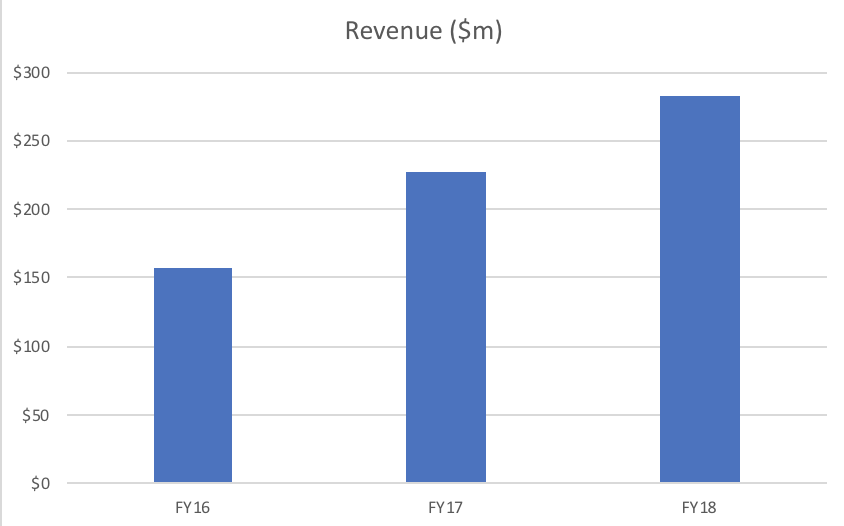

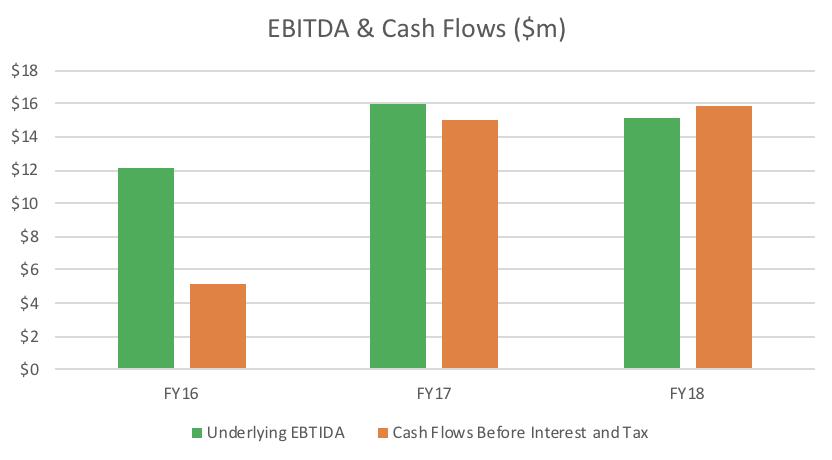

Since listing, MIL’s revenue and EBITDA have grown from $120m & $7.2m in 2015 to $282m and $15.1m in 2018. It hasn’t happened in a straight line but the business has grown without any dilution to shareholders and with decent cash generation along the way.

In that context it might seem odd that the stock has fallen from the IPO price of $2.25 all the way to 55c.

In that context it might seem odd that the stock has fallen from the IPO price of $2.25 all the way to 55c.

The problem is that ever since MIL listed in 2015 they’ve developed a bit of a track record for missing guidance. The most recent miss was FY18 where EBITDA guidance started at $20m and came in at $15m.

The market did not respond kindly. Throw in the fact that they had taken on debt to fund an acquisition (Airlite) in WA, the removal of the dividend and a number of messy one-offs and the 50% decline since results makes a bit more sense.

The Bears Are Winning, For Now

Basically, the previous team was too optimistic in their assumptions. They assumed they would renew more contracts and win more new ones than they actually did.

There is pressure on margins too. As contracts come up for renewal it is pretty standard for these big clients to try to squeeze out some additional margin from their service providers.

A 6 year renewal of the Scentre Group in FY18 and a number of other key renewals clearly had an impact on gross margin. The top 10 customers represent 75% of revenue so what the big clients choose to do has a significant impact on performance.

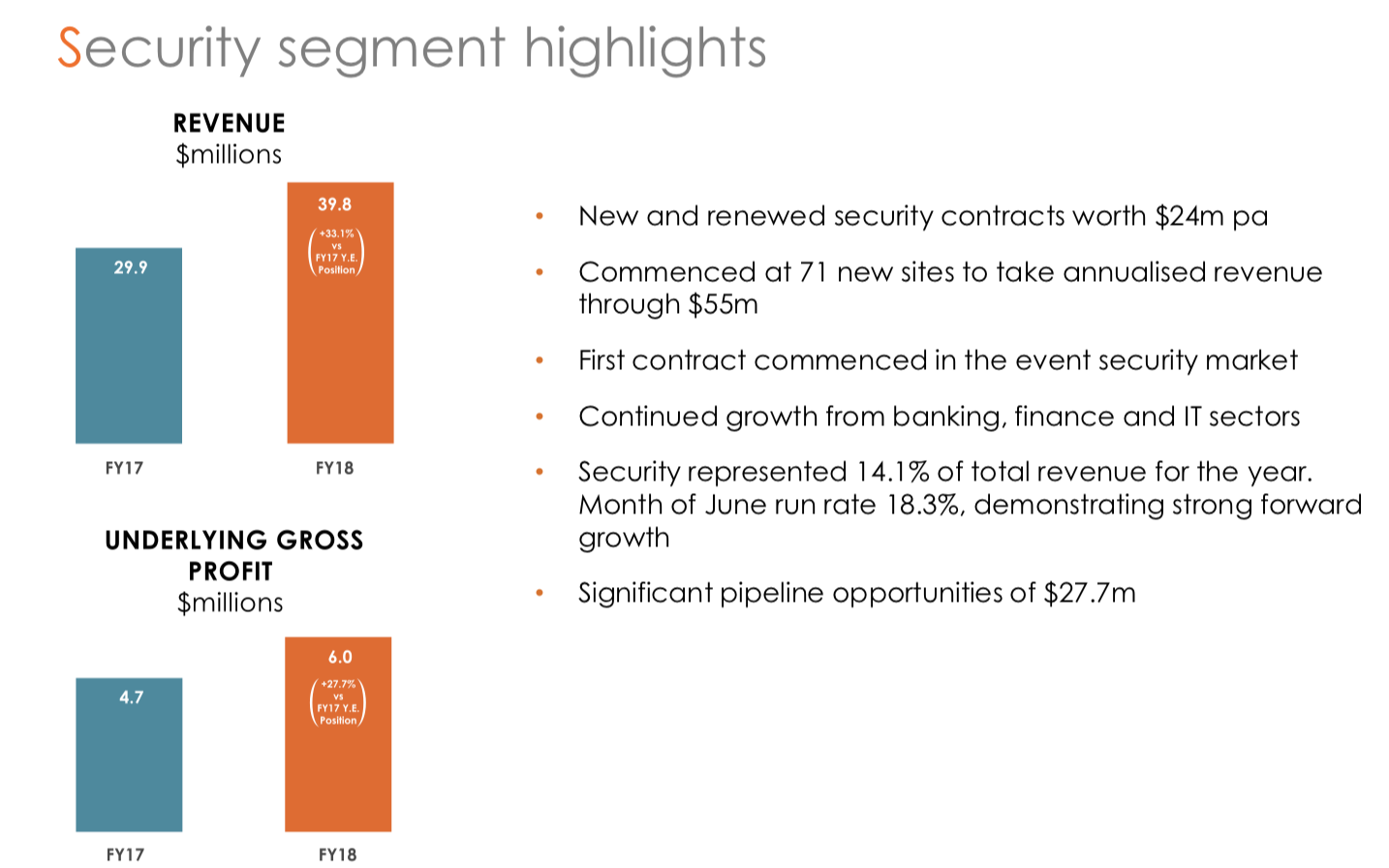

Security is a good news story for MIL. The division is growing at >30% and currently generates annualized revenue of $55m. The CEO comes from a security background and is pretty intent on growing the business to 30% of total revenue.

But the increased spend on personnel to bulk up the security business coincided with the other issues outlined above and further hampered the FY18 result.

They also spent more than usual on CAPEX, paid last year’s large dividend and had an abnormally high tax bill, all of which reduced free cash flow. That likely made a few in the market a little concerned in the context of the $24m of net debt on the balance sheet.

So the bears are clearly winning. The business has been through a rough period and has disappointed investors along the way.

But the current stock price appears to be more than compensating for the above. If MIL can show any signs that earnings are stabilizing and the new management team can start to transition to growth over the medium term then the stock won’t stay at 3x earnings.

And there are definitely some green shoots coming through.

A Bull Among Bears – Some Positive Signs Emerge

Margin pressure is real and so long as the client base is predominantly large property owners it isn’t going to go away anytime soon. But the way it works is that margins get crunched down on renewal and then the service providers, like MIL, work to increase the margin over the length of the contract which has agreed upon annual price increases.

The bulk of large contracts have now been renewed meaning a decent portion of the margin impact is accounted for. The margins on these renewals will slowly trend up over time, offset by any further renewals at lower margin.

There is also an attempt to diversify into new sectors including entertainment, commercial and industrial which together make up more than 25% of the >$160m contract pipeline.

We touched on security earlier. It is growing nicely and should continue to do so. It is also less capital intensive (less equipment required) and is not experiencing the same margin pressure as the cleaning business. The investment into the team to build this business has been made, meaning overheads won’t need to increase as quickly as security revenues grow.

The CEO is well regarded. He built and sold SECUREcorp for $150m before coming across to MIL. He’s spent a long time renewing the team and building new systems.

There is now a significant opportunity to digitize what has largely been an entirely manual business with >140 back office staff. Overheads will continue to trend down and management have indicated that every 1% reduction in staff costs will result in +$2m of EBITDA.

The Airlite acquisition gave them a national presence and wins with Myer, Apple and Vicinity are examples of this advantage in action.

They’ve built centralized bid teams and are taking a more economic approach to pricing. Recent wins show they can still secure new contracts on good margins and the exiting of marginal or loss-making contracts will improve working capital.

They’ve also gone from 20 tenders per annum when the CEO joined last year to now pumping out 450 annually.

One positive side effect of missing guidance and the market dumping your stock is that management have apparently learnt from past mistakes. Their approach to guidance has become more conservative.

They are now guiding to $290m-$310m of revenue and $15.5m-$17.5m of EBITDA for FY19.

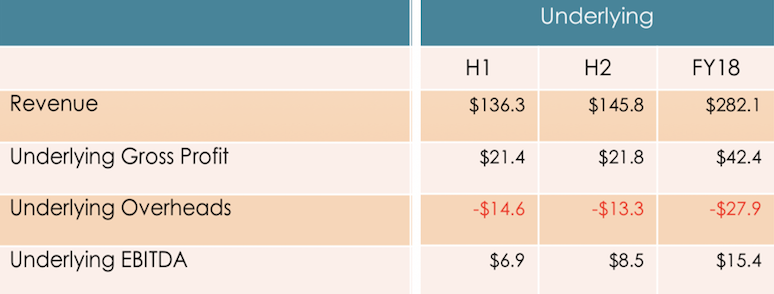

If you look at 2H18 they did $145m revenue and $8.5m EBITDA, meaning FY19 guidance is assuming a continuation of that run-rate and is not pricing in any growth.

We’ll look closer at guidance in a moment but it does appear that the new management team are trying to get a better hold of managing market expectations than occurred in prior periods.

The debt is an important issue. Net debt was $24m at 30 June 2018 consisting of $19m used to fund the acquisition of Airlite in Perth (paid down from $25m) and the balance in working capital facilities.

That looks high in contrast to the company’s current $25m market cap. And it certainly should come down to more comfortable levels.

But it represents 1.6x net debt/EBITDA and >6x interest cover. That doesn’t immediately strike you as excessive. Both are within their covenants. Many peers are more highly geared.

ANZ removed the headroom in their acquisition facility and doubled the size of their working capital facilities, essentially saying new acquisitions are off limits until you pay down the debt. As an aside, ANZ is a recent new contract win for MIL.

So debt is higher than ideal and increases the risks involved. However, this is a business that generated $15m of operating cash flow before interest and taxes in each of the past two years.

If they can sustain that sort of cash generation then the current debt is certainly serviceable.

And as debt levels are reduced the leverage in the equity value is significant. You can get real multiple expansion on the equity as the balance sheet is strengthened.

A business like this with a healthy balance sheet likely deserves a multiple of >10x.

Aligned Interests and Supportive Register

The Chairman, who is also the Executive Chairman of McGrath Nicol, has spent well over $3m acquiring shares on market at prices north of the current share price. He is sitting at 4.9% and presumably can’t buy any more as he would lose the ‘Independent’ tag.

Microequities went substantial in May and own 5%.

David Lamm of Kentgrove Capital and NGE Capital (ASX:NGE) went substantial in September with 7%. You can read NGE’s views in their latest Investment Update.

While I certainly can’t speak for their intentions it is nice to have a couple of well-known savvy managers buying at recent prices.

The other big shareholders are the vendors. One was selling above $1 but has become a buyer again. The intentions of the others are unclear but one would have to think that at these prices you would be running the numbers as to the possibility of taking it private. The original vendors have >40% of the stock.

My view, and what I would put to the board, is that a well managed capital raising at the right price would bring forward significant value. Off the back of confirmed guidance at the AGM there is a good chance the stock would re-rate closer to $1 - or 6x earnings - perhaps higher if commentary is positive.

At which point raising say, $4-$6m, along with debt reduction through free cash flows would have net debt/EBITDA move towards 1x – a comfortable level. Removing all debt concerns would put the business in a position to command a multiple closer to that of the market.

It would also bring forward the resumption of dividends. MIL already have $8.4m of franking credits on the balance sheet. They have a stated policy of paying out 40-60% of sustainable earnings.

It would not be hard to imagine that with a sturdy balance sheet and the return of dividends that the stock could trade on 12x earnings. That would see it trading near $2 based on FY19 guidance.

Capital H has a decent sized position in the stock and would certainly be supportive of something structured in this manner.

But they can cross that bridge when they get to it. The point is that having supportive shareholders like Microequities and Kentgrove Capital, as well as directors with significant skin in the game, makes value accretive corporate actions like these a possibility for the board to consider when the time is right.

Valuation

I’ve mentioned MIL being on a PE of 3x throughout this wire, so let me break down the numbers.

Start by believing management when they say they have learnt their lesson and now want to under promise and over deliver. We’ll assume they come in bang in the middle of their $15.5m-$17.5m EBITDA guidance.

$16.5m of EBITDA. CAPEX in FY19 will be “materially lower” (see FY18 conference call) than the $3.8m in FY18, call it $3m. Interest expense will be similar at $2.2m.

That would produce cash PBT of $11.3m. There are some tax losses to utilize but we’ll normalize for the full tax rate.

Cash NPAT would be $7.9m. There are 46m shares on issue, for EPS of 17c.

A PE of 3.2x based on the current share price of 55c. EV/EBIT of 3.6x.

An acquirer would be generating annual returns of >25% and have a 3-4 year payback period before any synergies, of which there would be plenty (see the Downer/Spotless example).

Essentially if you believe management’s guidance is reasonable then the stock is a bargain.

Take that 17c of EPS. Apply a multiple of 6-8x, which seems reasonable given current circumstances, and we have a share price of $1.00-$1.40.

As debt is paid down there is further room for multiple expansion. One could argue the $8.4m of franking credits need to be included in the valuation too.

But that is all a bit too easy. It’s worth breaking guidance down further to understand the assumptions driving it and form a view around what is reasonable.

FY19 guidance assumes zero growth over FY18’s run-rate. It accounts for security revenue of its current $55m annualized level and a flat performance for the cleaning business of around $240m.

Some of the margin impact from a high number of renewals in FY18 have already come through, shown in the reduced 2H18 gross margin (15.7% vs 14.9%). There are $50m of renewals coming up in FY19. By definition MIL’s guidance assumes they retain all of this, but they also assume they don’t win any new contracts.

It is unlikely that they don’t win any new contracts at all in FY19. They won $116m in new contracts last year, for a net gain of $52m. They were already +$5m in net wins for FY19 when they reported in August. You can’t simply annualize that figure but it’s a positive sign.

Given they are pumping out 450 tenders a year you’d have to think some of those are successful.

It is also unlikely that they lose all of the $50m of revenue up for renewal, although they are likely to lose some given their stated intention to only bid at a defined premium to WACC (other bidders may not be so rational). Typically these contracts are assigned on an asset basis, not a portfolio basis. So MIL might win, for example, 10 of the 40 assets in a big property group’s portfolio. At renewal they might retain half, lose the other half and then have some of those lost replaced by assets in a different location.

The risk in the renewals is 1) a change in the mix rather than the loss of all the revenue and 2) a margin crunch. The latter can be accounted for by assuming a hit to gross margins on these renewals in our forward numbers.

Let’s try to be really conservative.

For example, assume that MIL renew half of the $50m up for grabs and win no more revenue than the net +$5m already won in FY19 (i.e any new contract wins hit the revenue line in FY20). Then assume they take a 5% margin hit on the renewed contracts.

The timing of contract awards and any additional project work (typically billed additional to contracted revenue) would impact the revenue realized, but the above would equate to revenue of around $270m and gross profit of $39m. Overheads are running near $26m, for EBITDA of $13m. Using the previous assumptions for CAPEX, interest and tax it equates to cash NPAT of around $5.5m, or 12c EPS.

PE of 4.5x. EV/EBIT of 4.9x.

It’s an example of the kind of margin of safety that appears to be on offer here. MIL could miss guidance by some margin and the stock still looks cheap.

Turnarounds, Inflection Points and Timing Your Entry

Turnarounds can be lucrative. Particularly those with a bit of debt because it tends to crunch the equity value when the market gives up on the stock but works in reverse as the balance sheet deleverages.

Low single digit multiples compensate you for a lot of problems. Sometimes you get paid to buy what the market hates. Occasionally you’ll get paid very well.

Of course, MIL is an early stage turn around. Turn arounds have risks and so do businesses with geared balance sheets. They are also notoriously hard to time.

Usually you’d want to see some catalysts to push the stock higher and unlock what appears to be clear value. But sometimes the catalyst is simply the extreme pricing discrepancy and it just takes the market waking up to it for the stock to start to move higher. I think MIL may be a candidate for this.

They’ve now built the team required to get the job done. The business has a history of producing good cash flows sufficient to move the balance sheet into healthy territory.

As they do, and particularly if they can show signs that FY19 is a consolidation year from which to grow, then it won’t stay at 3x earnings. Meanwhile the market has given up on it and is pricing in near zero chances of success.

That’s why MIL looks interesting.

Disclaimer: The information above is based on the research and opinion of the author and is not intended to be viewed as financial advice. You should complete your own research and seek professional advice before making any investment decision. Capital H holds share in Millenium Services Group.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund.

Previously worked for Pie Funds and Bligh Capital.

2 topics

4 stocks mentioned

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment