New Macquarie Hybrid Cheap or Expensive, Depending on Perspective

Macquarie Group Limited (MQG) has cheekily launched an offer for a new Additional Tier 1 (AT1) capital hybrid security, to be listed under the ASX code MQGPD, which is not refinancing an existing maturity but rather appears to be an attempt to front-run the federal election and tap into cash being made available by two major bank maturities in March ($660m WBCPD on March 8 and circa $750m NABPA on March 20).

MQGPD is preferred equity that sits between subordinated bonds and ordinary shares in Macquarie’s capital structure with a 7.5 year expected repayment (or call) date in September 2026 and mandatory conversion into Macquarie shares in September 2029 if it is not called.

Based on current major bank hybrid spreads on the ASX, Coolabah Capital Investments (CCI) has the fair value credit spread for MQGPD at around 4.30% above the bank bill swap rate (BBSW), which is greater than the 4.15% spread that Macquarie is proposing to pay. (While unlikely, it is possible a broker might be prepared to offer an investor a small rebate on some of their commissions that could potentially lift the expected spread to attractive levels.)

If we price the security off Macquarie’s current ASX AT1 curve, fair value drops to 3.85% above BBSW, and MQGPD suddenly looks quite cheap. We discuss this alternative perspective in more detail later.

Macquarie hybrid credit spreads have been trading inside, or expensive to, the major bank hybrid curve in recent times because they offer the highest unfranked, or cash, yields in the market. Indeed, the 5.28% total cash yield on MQGPD before any franking would make it the best total return offered on any major bank or Macquarie hybrid security.

If we value this security on a bottom-up basis using our Merton models, we get a minimum fair value credit spread of 3.96% above BBSW accounting for Macquarie’s leverage and making conservative assumptions about the risk of default and recovery. Specifically, we shock Macquarie's equity volatility since 2000 by one standard deviation and assume a 0% recovery rate. MQGPD’s slated 4.15% margin above BBSW looks reasonable in this context.

Macquarie has a higher-rated AT1 security with a similar expected maturity in the institutional US dollar over-the-counter market, which is currently offering a 5.33% spread above BBSW after swapping it back into Aussie dollars. This is obviously more than 1.15% per annum above the spread Macquarie is proposing to pay on MQGPD, which makes the new deal appear dear. For what it is worth, when we apply a multi-factor regression to Macquarie’s USD hybrid, we find that it is about 35 basis points cheap in spread terms to its USD fair value curve.

In summary, for non-taxpayers who worry that they will not be able to get cash refunds on franking credits if Labor wins the election, the Macquarie hybrid may be enticing. For normal taxpayers, it looks expensive relative to major bank spreads on a risk-adjusted basis.

1. New Money Deal Size is Likely to be Large, not Small, at Over $750m

MQGPD comes only eight months after Macquarie issued its MQGPC security in July 2018, which like this deal was marketed as being only “small” but in the final analysis was upsized to a decent $1bn issue.

Brokers are once again claiming MQGPD will be modest, but with the initial guidance signalling a deal over $500m, which is more likely to land in the $700m to $800m range, all of which will be crucially “new money” (given there are no rolls of existing cash from an upcoming Macquarie maturity), this transaction will, in fact, be as large in new money terms as the last three major bank deals from NAB, Westpac and CBA.

This will likely create attractive switching opportunities as brokers (irrationally) sell cheaper major bank hybrids to buy the more expensive Macquarie hybrid (on a risk-adjusted basis) in order to capture their sales commissions, which savvy investors can capitalise on.

2. Implied Macquarie Group Hybrid Rating of BB- is Two Notches below Major Bank Hybrid Ratings of BB+

Macquarie Group’s issuer credit rating with Standard & Poor’s is only BBB, which is two notches below the major banks’ stand-alone credit profile (SACP) ratings of A- and five notches below the major banks’ AA- issuer credit ratings.

This means the implied S&P rating for the new MQGPD hybrid is a fairly frisky BB-, which is two notches below the major banks’ hybrid ratings of BB+. Importantly, if S&P lifts Australia’s economic risk score, as it has said it is trending towards doing (consistent with our long-held forecasts), this will increase the major banks’ hybrid ratings to BBB- into the all-important “investment-grade” band (as a result of their S&P risk-adjusted capital ratios rising above 10%), but it will have no impact on Macquarie’s hybrid ratings, which will remain in sub-investment grade territory.

Put differently, there are clear credit rating upgrade prospects that will reduce major bank hybrid risk premia that are not presently accessible with the Macquarie hybrid.

3. Multiple Call Dates Create Extension Risk but No CET1 Equity Conversion Trigger is a Positive

The new MQGPD hybrid is callable in September 2026 (or otherwise, in March 2027 or September 2027), and these multiple call dates create greater extension risk than a normal major bank hybrid where there is typically only one call date for Basel III securities.

MQGPD qualifies as Additional Tier 1 (AT1) regulatory capital under the Basel III capital framework, and mandatorily exchanges into equity in September 2029. It can be converted to equity or written off by APRA if a “non-viability” event occurs, where APRA judges that without conversion or write-off, Macquarie Group would not be viable.

Notably MQGPD does not contain the “capital trigger” clause that most other Australian bank hybrid securities have, as the issuer is a group entity, rather than Macquarie Bank, where the latter is regulated by APRA as an Authorised Deposit-taking Institution.

With a normal major bank hybrid, the security is automatically converted into shares if the Common Equity Tier 1 (CET1) capital ratio falls to 5.125%, which is roughly half the larger banks’ current CET1 ratios. This risk is not present in MQGPD.

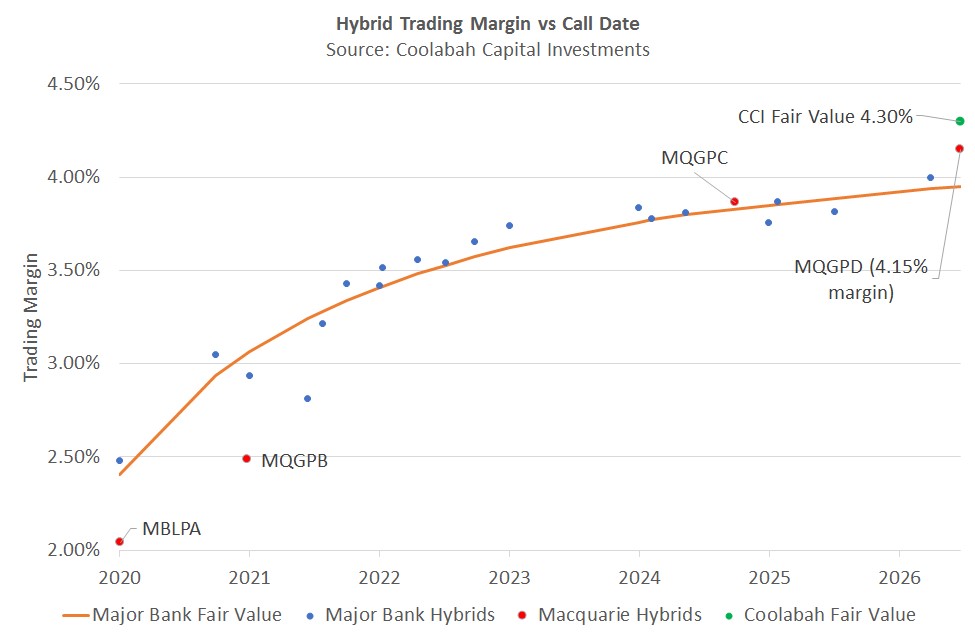

4. MQGPD Looks Expensive Compared to CCI’s Fair Value of 4.3% Above BBSW

Macquarie proposes to pay quarterly distributions based on a partly franked spread of 4.15% above the three month bank bill swap rate (BBSW). BBSW is currently 1.90%, which implies a total current running yield of 6.05% annually.

A major bank hybrid with 7.5 years to call would currently demand a spread of 3.95% over BBSW. Ordinarily, we would require a hefty ~0.35% (or 35 basis point) premium above this to assume Macquarie Group risk. We verify this required premium by looking at the historical trading ranges for regional bank hybrids over their major bank equivalents, and while there are always periods where regional bank hybrids are in higher or lower demand than major bank securities, we have found this framework to be broadly accurate over time.

Furthermore, MQGPD is notionally rated two notches below major bank hybrids (BB- versus BB+), and the liquidity of non-major bank hybrids is usually lower than that of the majors

All else being equal, this means the minimum credit spread we would require to invest in the deal would be around 4.30% above BBSW, some 15 basis points above the expected 4.15% spread, shown below.

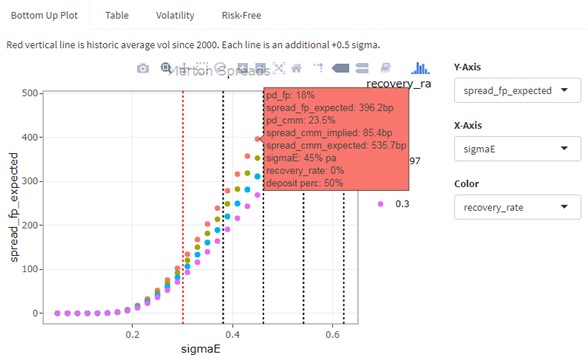

5. Bottom-Up Merton Analysis of Minimum Required Risk Premium is 3.96% Above BBSW

On a bottom-up basis, we apply our customised first-passage Merton model to quantify the expected probability of default and loss associated with MQGPD. This model requires us to input balance-sheet leverage data and historic equity volatility. We take average volatility since 2000 and increase it by one standard deviation to proxy for APRA declaring a non-viability event well ahead of equity being fully wiped out. We further assume a 0% recovery rate on MQGPD. On this basis, the fair value credit risk premium is 3.96% pa above BBSW.

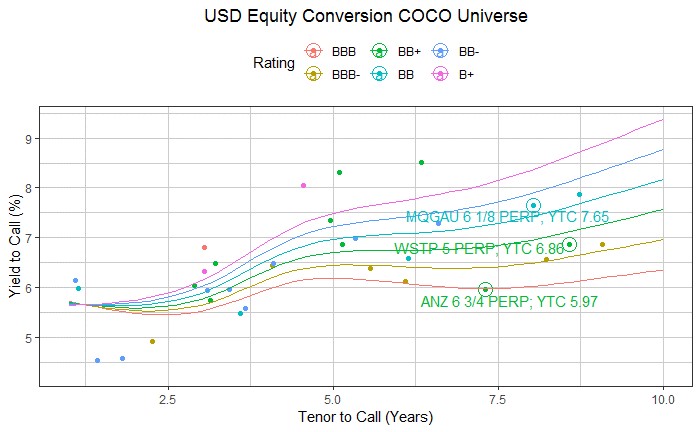

6. USD Curves Imply this AUD Hybrid is Expensive

Macquarie has an AT1 hybrid security issued in the institutional US dollar market that provides an important comparison. The security is callable in March 2027 (so with a similar tenor to MQGPD) and pays a fixed 6.125% semi-annual coupon (unfranked). It is rated ‘BB’ by S&P, thanks to the issuer being the London branch of Macquarie Bank, so is one notch higher quality than MQGPD’s BB- rating.

Accounting for interest rate differentials and the cross-currency basis markets, the USD security currently offers an equivalent Australian dollar yield of BBSW plus 5.33%, notably some 1.15% pa higher than the proposed MQGPD spread.

Macquarie’s US dollar hybrid is also cheap compared to other US hybrids. Measured on a yield to call basis, the security offers a 7.65% yield, compared to our fair value of 7.30%, which is computed using a multi-factor regression model that takes into account the characteristics of the USD hybrids universe, including tenor, rating, issuer region, and the reset margin that applies after the first call date.

7. Cheap Compared to Macquarie’s Curve and on a Cash Basis

Macquarie is one of the few hybrid issuers that does not fully frank its distribution payments (due to its offshore income that does not generate franking credits).

Macquarie hybrids are currently franked at a 45% level, which means that quarterly distributions are made up of only 13.5% franking credits and 86.5% cash (this compares with 30% franking credits for most other hybrids).

This is vital for some investors, because if the ALP win the coming federal election, their policy to remove the ability of non-taxpayers (or low-taxpayers) to claim cash rebates on franking credits is at risk of becoming law (though we expect it to ultimately be further watered down or rejected in the Senate). For those who are affected by this potential policy, the low franking rate significantly improves the value of the security.

This feature explains why Macquarie’s existing hybrids have been recently trading at spreads tighter than major bank hybrids over the last year (since the ALP announcement in March 2018).

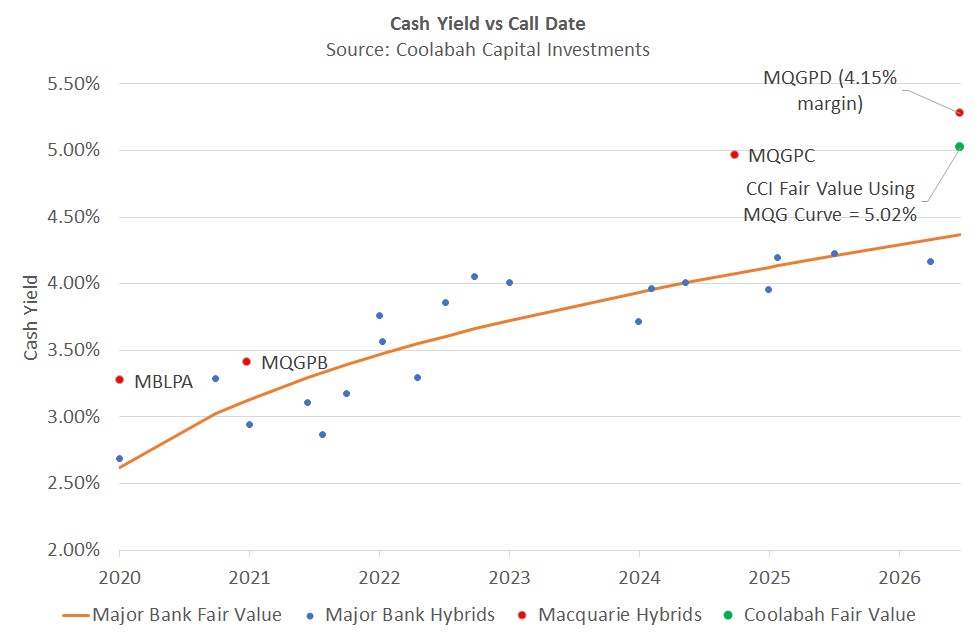

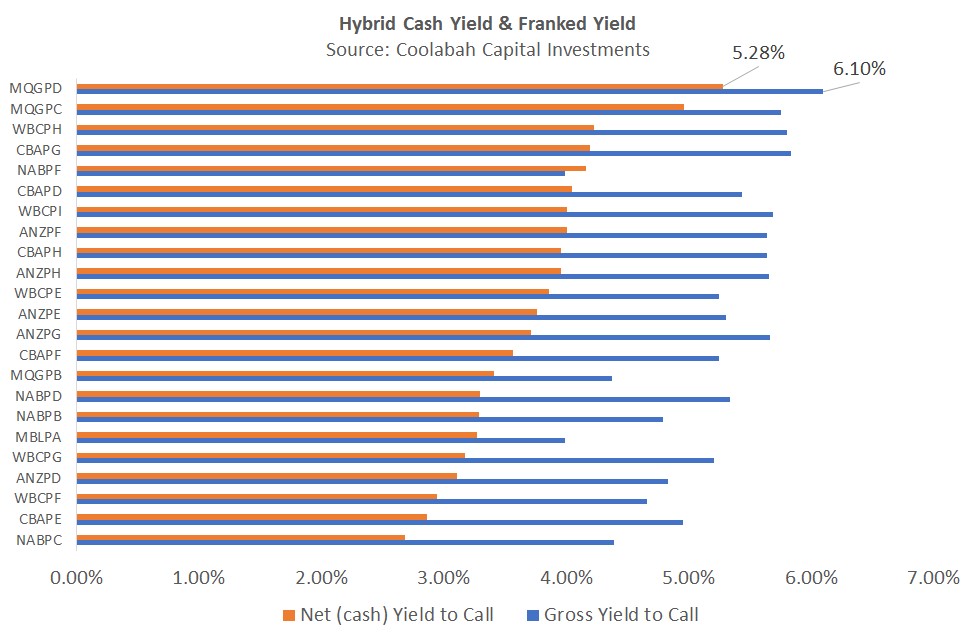

On a cash-only basis (ie, ignoring the value of franking credits), Macquarie’s hybrids are offering by far the highest yield to call in the sector, reflecting their relative immunity to the change in franking policy, as shown in the chart below.

Indeed, the cash-only yield to call of MQGPD, were it to issue at the assumed 4.15% above BBSW, would be 5.28%, the most generous in the sector. If we interpolate off existing Macquarie hybrids, fair value for MQGPD is 3.85%, making the proposed 4.15% spread look very cheap. That 3.85% fair value equates to a total cash yield of 5.02%, shown on the chart below.

8. Other Considerations

While this new issue was not widely expected (not being a refinancing), the supply/demand outlook for the hybrids market is still positive. Macquarie have timed this issue to take advantage of $660m of WBCPD flowing back into bank accounts as the remainder of that security is called in early March, as well as the circa $750m of NABPA investors that have chosen not to exchange for NABPF units.

Arguably Macquarie have also timed the issue to take advantage of the demand for high cash-yield securities prior to an expected Federal election in May. Later in the year, there are almost $1.4bn of ASX-listed hybrid and debt securities due to mature or to be called, none of which are likely to be refinanced on the listed market, all of which raises the demand for remaining hybrid securities.

Finally, Macquarie has been relatively untouched by the Royal Commission into Banking and Financial Services, and has posted consistently superior return on equity to the major banks with an outstanding risk management framework that has avoided any material problems over the last 40 years.

Disclaimer: This information is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment