News Corp: Approaching an inflection point

News Corp, the global diversified media and digital real estate services company, today reported financial results for the fourth quarter and fiscal year ended 30 June 2018. We've pulled out the key highlights here, and share our view of the stock.

Overview of the numbers

For FY18, News Corp (NWS) delivered an 11% increase in revenues to $9.02 billion, and a 21% increase in EBITDA to $1.07 billion. On an adjusted basis (excluding FX, acquisitions & divestitures) revenue was up 2% and EBITDA increased 6%.

Non-recurring items were a material drag on statutory earnings (net loss $1.4bn), primarily driven by the $998m goodwill write-down on Foxtel & Fox Sport, which was associated with the merger of assets.

Free cash flow was $249m compared to $113m in the prior year, this was despite a 42% uplift in capital expenditure. Capital expenditure is forecast to remain elevated in FY19 with further investment required in the recently consolidated Foxtel/Fox Sports.

3 Key Highlights from the result

1) News & Information Services reported in FY18 a 1% uplift in revenue, whilst EBITDA declined 5% on the prior year. Declining revenues in print advertising and News America Marketing were partially offset by the growth in digital advertising revenues in the Australian, UK and US newspaper mastheads. Circulation and subscription revenues increased 5% reflecting the improved reach of digital subscriptions. Digital revenues represented 30% of News & Information revenue base compared to 26% in the prior year.

2) Digital Real Estate Services continued to generate strong revenue up 22%, driven predominately by REA (+27%) and Move (+15%). It is worth noting that Move’s revenue growth moderated in the 4th Quarter reflective of slowing US housing volumes.

3) Significantly, this is the first time that NWS has reported the Foxtel/Fox Sports merger as a consolidated entity. Post-merger, NWS owns 65% of the combined group entity, with Telstra holding the balance. Consolidation of Foxtel should be the first step in unlocking value.

As anticipated, operating momentum remains challenging for Foxtel, faced with a combination of lower subscribers & ARPU, and higher sports programming costs. Foxtel’s successful bid for the cricket rights is earnings dilutive but importantly bolsters its sports credentials by offering a full calendar of major sports. Importantly, NWS confirmed Foxtel will release a sports streaming service in the second quarter. Over the short term, it is hard to see any meaningful improvement in operating trends. Nonetheless, meaningful cost synergies should be realised by combining Fox Sports and Foxtel.

The rise of proposed merger activity amongst legacy media companies (Fox/Disney, Fairfax/Nine) typifies traditional media’s need to gain scale in content to more effectively compete with tech companies such as Amazon and Netflix. Inherently tech companies are valued on growth, not earnings, which provides them an unfettered licence to spend on content. A key challenge for Foxtel is how it reshapes its consumer offering in content and distribution to stem its decline in subscribers and ARPU. Hence, any meaningful re-rating of Foxtel requires signs of stabilisation in operating metrics.

What the market is overlooking here

The immense power unleased by a small number of social media companies in disrupting “traditional” media is well understood. The ability of social media platforms to harvest vast sources of data for advertisers has provided unprecedented challenges to traditional media business models.

Notwithstanding this, there are growing signs that NWS is making positive headway in its subscription and digital advertising revenue.

This is is despite the headwinds of tightening data protection laws as “fake news” and the misuse of personal information proliferate. As laws such as the EU’s General data Protection Regulation (GDPR) and the ACCC’s inquiry on the conduct of digital platforms suggest growing recognition that social media companies are facing greater scrutiny. Thus, the practice of taking limited responsibility for what appears on Facebook and other social platforms no longer sounds plausible. Ironically, Facebook is using advertising billboards to promote their social credentials that “fake news” is not a friend.

The premium “content” offered under the News Mastheads of the Australian, The Times and Wall Street Journal, are increasingly resonating with readers. We would contend that greater value will be ascribed to “premium content” reflected in the continued growth in both subscriptions and advertising for News and Information Services.

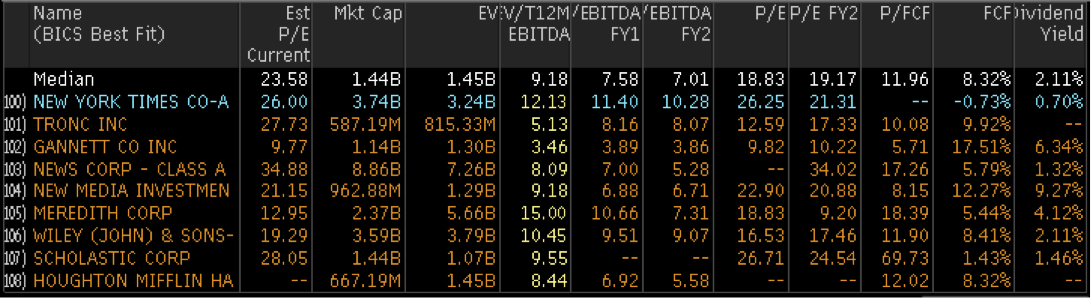

The New York Times (NYT) provides a useful precedent in illustrating that traditional media assets are not only sustainable but critically can show meaningful improvements in sales and earnings momentum. Such improvement has translated into ascribing a sizeable re-rating in NYT’s EV/Earnings multiple.

Source: Bloomberg

Our investment View on News Corp

There has been a perennial fascination that value exists with NWS on a sum-of-the-parts valuation. The catalysts for closing the value gap have remained tantalisingly elusive.

Our sense is that NWS is approaching an inflection point in stabilising its News & Information business. A concerted focus to expand its digital audience through premium content is making tangible progress.

Yet, historically the market has ascribed a low multiple to a declining or low growth challenged business. Further signs of progress with its digital transformation could warrant ascribing a higher multiple to News & Information business.

With Digital Real Estate exhibiting continued strength, particularly in REA, and top line trends in Realtor showing further progress (earnings not disclosed), NWS remains a cheap way to gain exposure to this theme.

Whereas ascribing a higher value to a consolidated Foxtel requires evidence that its decline can be arrested.

As we move deeper into a period of extended equity prices, finding value in an absolute sense is becoming more challenging.

Within this contest, Newscorp's valuation metrics, on a sum-of-the-parts basis, and its robust balance sheet underpin its investment proposition.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO (Asia Pacific) for Canaccord Genuity.

1 topic

2 stocks mentioned

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management