Now is not the time to be a hero

For a while it looked like nothing could derail the constant drive higher in asset prices as central banks worked out that with quiescent inflation they could continue to print money to support markets. It was often speculated that a black swan event like a viral pandemic could derail the economy and markets, but no one gave it too much consideration. Enter the Novel Coronavirus (COVID-19) and in the space of month the world has undergone a titanic shift. Everyone is likely overloaded with information on the virus at this stage, needless to say that it appears to be highly contagious, and is potentially fatal.

Since the outbreak originated in Wuhan, China authorities have shut down Hubei province and much of the country. This appears to have been effective in containing the virus with a marked slowing in new infections and a fall in active cases. The chart highlights the peak in active cases in mid February.

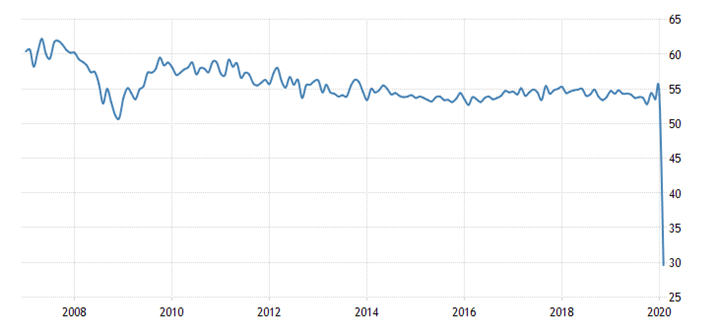

However these actions have had an enormous economic impact in China, which is beginning to ripple around the world. The most recent manufacturing survey highlights the collapse in economic activity in China, which is the largest in history, being even greater than during the GFC.

China NBS Manufacturing PMI

If you think that chart looks a little ugly, the non-manufacturing PMI is far worse.

China NBS Non-Manufacturing PMI

The sort of containment action undertaken by China has been effective, but comes at a huge economic cost. What’s not clear is whether the virus will re-emerge once life goes back to normal. Given its quite lengthy incubation period and high proportion of asymptomatic carriers that is a distinct possibility.

Of greater concern for the global economy and markets at the moment is the accelerating spread of the virus outside of China. Hotspots have sprung up in South Korea, Iran and Italy with further transmission from there to Europe and the rest of the world. What is readily apparent is the high level of global travel that occurs in the modern economy and how our very way of life makes it almost impossible to contain. Western governments now face the tough choice between the significant economic cost of stringent quarantines and the significant cost in human life in allowing it to continue to spread. It is unlikely that Western governments will have the political appetite to shut the economy down like China has, so the accelerating spread in cases outside of China depicted in the following chart likely has much further to run.

Whilst it looks likely that there will be a tragic loss of human life in the coming months, it most certainly won’t be the end of the world. From an investment perspective we are facing a likely global recession and we need to know how deep and how long. Past viral outbreaks such as SARS have been reasonably minor with only a passing economic impact, however this appears to be something more substantial. On the positive side we could see more effective treatments or vaccines developed, but this will take time. Once we move past efforts to contain the virus, human nature tends to be adaptive and life will move on, even while the virus is still lurking. The danger to the economy is that the world is more fragile with the amount of debt built on cheap money in recent years. The short-term economic impact could feed through to business stress, unemployment and a negative credit cycle. Markets are unprepared for this, even after the sell-off in recent weeks.

Will central banks come to the rescue?

There is likely to be a policy response at some stage to the deepening crisis. Markets have already factored in rate cuts, of which some were realised recently, but lowering interest rates at this stage will do nothing to stop the spread of the virus and will have little economic impact given that monetary policy is currently transmitted through pumping up asset prices. Central banks may even hold back from cutting, waiting for a time when the little ammunition they have left can give a boost to confidence. Fiscal stimulus of some form will likely be required, but the capacity for indebted governments to deliver it may be a challenge. The nature of the economic challenge that lies ahead will most likely depend on the political battle to allow central banks to finance deficit spending.

From an investment perspective it is always tempting to buy panic selling, but the current market gyrations remind us more of the beginning of the GFC, than one of the minor panics we’ve had along the way since then. Now is not the time to be a hero, but to look to preserve capital. This is harder than it sounds when the market is trading at record valuation multiples. It is not that difficult to identify economically sensitive companies with travel and tourism being at the top of the list, but they have already been hard hit and may not have more downside than the rest of the market.

Similarly, defensive sectors like healthcare and supermarkets should be reasonably immune to the economic shocks but are trading at record multiples. If markets become dysfunctional then they may not prove to be safe. Ironically, companies that have faced structural headwinds like media are trading at low multiples and may be more resilient in a market sell-off, or the economic shock could be the straw that breaks their backs.

The outlook for Australia is clouded

Australia is obviously very sensitive to Chinese and global growth through its resources sector, but the outlook is also clouded here. Iron ore has held up well even though China’s steel mills are operating at reduced capacity because domestic iron production has been wound back even further. The strong balance sheets in this sector could prove defensive in a short recession with a sharp rebound and plenty of stimulus, or they could be the most exposed to collapsing demand. Appropriate positioning at the moment is to reduce risk, maintain diversification and take a defensive stance.

Sell-offs are inevitable – stay invested

We know that sell-offs are inevitable and the longer your holding period, the better the outcomes. While our focus in the short term remains on preserving capital, we do see a material opportunity as the fallout from this pandemic recedes. There will be plenty of opportunities to buy good businesses at more attractive prices in the coming months.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sean is a fundamental and quantitative equities investor, with more than 20 years of experience managing Australian equity investment portfolios. Prior to forming Sage Capital, Sean was Portfolio Manager at Tribeca Investment Partners and AMP Capital

Featuring

Sean Fenton,

Sage Capital

Sean is a fundamental and quantitative equities investor, with more than 20 years of experience managing Australian equity investment portfolios. Prior to forming Sage Capital, Sean was Portfolio Manager at Tribeca Investment Partners and AMP Capital

........

This information is provided by the Investment Manager, Sage Capital Pty Ltd ACN 632 839 877 AR No. 001276472 (‘Sage Capital’). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 (‘Channel’) is Sage Capital’s distribution partner. This information should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units in the Fund and does not take into account your particular investment objectives, financial situation or needs. Past performance is not indicative of future performance. All investments contain risk. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the Product Disclosure Statement available from www.sagecap.com.au and www.channelcapital.com.au.

5 topics

Sean is a fundamental and quantitative equities investor, with more than 20 years of experience managing Australian equity investment portfolios. Prior to forming Sage Capital, Sean was Portfolio Manager at Tribeca Investment Partners and AMP Capital

Expertise

Comments

Comments

Sign In or Join Free to comment