Our 2018 investment anti-forecast – Forget forecasts

It is a continuing curiosity of investing that people can be so obsessed with trying to predict the future yet at the same time find it so difficult to think beyond the present.

It is a continuing curiosity of investing that people can be so obsessed with trying to predict the future yet at the same time find it so difficult to think beyond the present.

The start of January traditionally sees many investors trying to fill the blank slate the new year represents with forecasts of what the coming months will bring.

Ever the contrarians, here in the Global Recovery team, a more recent tradition has seen us offering up our own new year ‘anti-forecast’, which is intended to illustrate the dangers and indeed utter pointlessness of trying to predict the future.

Predicting the future is pointless

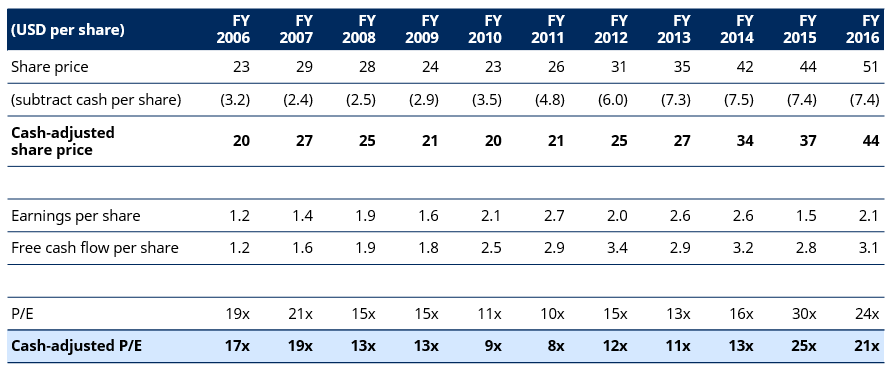

As 2018 begins, then, we find ourselves looking backwards rather than forward – and specifically to 2013, when we built up stakes in Microsoft and a number of other technology names that are not usually associated with the world of value investing.

Five years ago, however, they certainly were as the wider market was just not interested in what it saw as ‘old tech’ businesses.

Convinced the cloud would change everything and personal computers were history, investors were steering clear of Microsoft and its share price was consequently very depressed.

The wider market could not envisage a time when the company’s fortunes would ever improve – but of course that is precisely the sort of situation that attracts our attention here in the Global Recovery team.

A classic 'value trap'?

Where many investors saw a classic ‘value trap’ – a company that is cheap but for a good reason – in Microsoft, we saw a well-capitalised, financially strong business for which the wider market had some very low expectations.

Fast-forward five years and today, of course, Microsoft is doing very well – and, on a price/earnings ratio of some 30x (a valuation measure where lower figures represent better value), it is now three times as expensive as it was in 2013.

The point here is not to preen about an investment that has worked out very nicely for our portfolios and our investors but, rather, to highlight that only one thing has materially served to move Microsoft’s valuation, and thus its share price, over the intervening years.

What it does, its structure, its financial strength – these are all largely as they were in 2013 – and all that is really different is people’s expectations for the business.

Microsoft share price

Past performance is not a guide to future performance and may not be repeated.

Past performance is not a guide to future performance and may not be repeated.

Source: Bloomberg, and Schroder analysis. As at March 2017. For illustrative purposes only and not to be considered a recommendation to buy or sell.

In effect, it is only how people feel about Microsoft that has changed – and, of course, emotion is what a value approach to investing seeks to remove from the equation.

Furthermore, one of the exciting aspects for value investors is the knowledge that if you buy a financially strong business for which the wider market has low expectations, the associated risk is what is known as ‘asymmetric’.

Asymmetric risk

If the share price does fall, it can fall no further than zero and yet, on the upside, the sky is – potentially, at least – the limit.

What is more, things only have to grow less bad – a slight lessening of negativity or a small positive surprise – to make a lot of money. Sure, you do not know exactly when that will happen – as we keep on saying, nobody can tell the future – but that is why you have to buy in when a good business is very cheap.

On the flipside, of course, if you choose to buy into a growth business with high expectations – and thus a high valuation – some amazing things have to happen for its share price to grow much further … and, even then, it only grows into the price you are being asked to pay today.

In the first 'value' instance, the difference between current price and fair value offers a greater chance of upside, in the latter 'growth' instance, a greater chance of downside.

Why did we buy Microsoft?

So what our 2018 anti-forecast boils down to is that our decision to buy Microsoft was unfazed by what everyone else was forecasting.

What mattered to us with Microsoft – and indeed with any other investment we make – is it was financially strong enough to give it the best chance of reaching what we calculated to be its fair value rather than what the rest of the market thought it was worth.

It is a continuing curiosity of investing that people can be so obsessed with trying to predict the future yet at the same time find it so difficult to think beyond the present.

For further insights from Schroders Australia, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

1 topic

1 contributor mentioned

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

Expertise

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment