Ramsay Healthcare (RHC): Why we remain short

Charlie Aitken

Aitken Investment Management

Ramsay Healthcare (RHC) is a core structural short in the AIM Global High Conviction fund. The five bear points we have consistently pointed to are:

- Expensive: more than double its long-term price to book ratio (currently at 6.5x book value vs. long-term average of 2.9x)

- Regulatory Risk: review into Prostheses pricing could have major impact on profitability. Along with tariff cuts in France & UK

- Management Change: Managing Director Chris Rex unexpectedly stood down in February after 10 years in charge

- Significant Insider Selling: MD & CFO sold $27m and $7.5m of shares respectively

- Competitor Downgrades: biggest competitor, Healthscope (HSO), has experienced management turnover, earnings downgrades and significant insider selling

AIM continues to have a cautious view on market darling Ramsay Healthcare (RHC) and feel it has further to fall in the months ahead. While the stock has fallen around -17% from this time 12 months ago, our argument would be that RHC has simply gone from “very expensive” to “expensive”. The AIM Global High Conviction Fund remains short RHC shares feeling consensus earnings and the multiple the market is currently paying for those ambitious current consensus earnings estimates remain too high.

The chart below shows consensus FY18 P/E for RHC. It’s really only dropped a few P/E points from 12 months ago and is the same as the start of this calendar year. It’s worth remembering this P/E is set off “E” which we think will prove ambitious.

When you’re a high P/E stock priced for “great expectations” you need to consistently deliver those expectations or more. That’s what Treasury Wine Estates (TWE) has done for example. However, RHC failed that test in its FY17 earnings which have seen analysts reduce FY18 estimates by around -5%. The numbers RHC delivered for FY17 were “messy” but well below expectations any way you cut them.

The five reasons we gave you for our short in RHC are described above, but we can add one more now, “earnings downgrade cycle” which is arguably more important than anything in a high P/E growth stock. When the consensus earnings revision cycle turns negative you need to be very, very careful. This is because the market will currently reduce the P/E of the company as earnings revisions turn negative. It’s a double whammy where a good recent example would be Domino’s (DMP) in the two charts below

Consensus DMP FY18 EPS forecasts have dropped over the last 12 months by -8.3% and the FY18 P/E has fallen by -36%.

This is the danger of investing in “growth at any price” companies. If the tide turns there simply ISN’T a marginal buyer because they simply don’t represent “value” until a price a “value” investor would consider. Australia in particular sees these situations occur all the time. The narrow nature of the Australian equity market drives institutional investors to pay up for growth where they can find it. However, when the tide turns these stocks hit an air pocket until they fall enough to represent value. In Ramsay’s case, 23.5x P/E for FY18 is not value and our view is RHC will continue to experience a P/E de-rating.

The other thing to remember is Ramsay’s tight register. This tight register with a low free float, driven by the Paul Ramsay Foundations 32% holding, exacerbates both the upside and downside in the stock. Domino’s also has a 25% shareholder that contributed to exactly the same phenomena, while Gerry Harvey’s 30% holding in Harvey Norman makes the register easier for hedge funds to short. The point is tight registers work very well in the earnings upgrade cycle, but against you in the downgrade cycle.

In terms of Ramsay specific issues it was both the quality and quantity of their FY17 earnings that underwhelmed. Again, that is a problem in a high P/E stock.

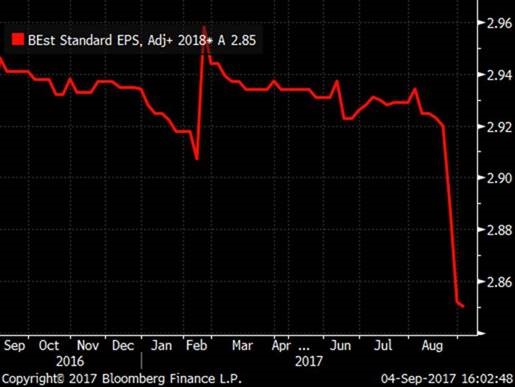

There appear two items that need to be “normalised” to genuinely determine what the “underlying” profitability performance was. The first is an increased over FY16 of the change in value of RHC’s deferred tax assets and liabilities of A$12.8m due to a tax rate change in France was recognises in Core NPAT which is arguably a “non-recurring” event, as well as non-assessable items in Core profit of A$8.3M. The second is the reversal of $10m of provisioning expenses. These expenses were in legal, compliance and insurance provisions.

What analysts are now pointing to is that if FY17 Core NPAT is “normalised” for a deferred-tax FX change and provision reversals, along with RHC’s noted -1% FX impact, then constant FX NPAT for F17 was A$519M or growth of +7.9%. This “growth” includes an estimated $30-$40m of global procurement savings and $25m of abnormal Australian cost-out. Therefore, an argument can be presented that RHC’s “organic” NPAT growth in FY17 was negative, if you take the view these variables are one-offs.

Under that “negative” organic growth profile for FY17 assumption it then brings into question RHC’s guidance for FY18 of “+8-10%”. To us, that seems very optimistic particularly under a scenario of peaking Australian hospital margins.

According to Bank of America Merrill Lynch analysis Australian hospitals earned +13% EBITDA margin 10 years ago. Now its 18% to 20%. +3.5% average revenue price growth from health insurers, 4% industry average surgeries volume growth over the decade to FY16 drove up margins. In FY17 price growth was about +2.5% and surgeries volume growth +3%.

From this point on however there is no evidence to suggest that volume growth nor health insurer pricing will appreciably rise, while the government is working to reduce prosthesis funding and by inference RHC’s rebates. It would appear industry dynamics are shifting and we expect the market to apply a lower P/E to RHC to reflect these growing risks.

This is a very important point on Australian hospital margins peaking for RHC as Australia is the star of the RHC show and the real reason for the big P/E multiple. RHC has “diworsified” overseas and its offshore businesses generate significantly lower returns than its Australian business. European growth will continue to be negative due to tariff cuts and we believe the market applies a 9x EV/EBITDA multiple to the offshore RHC business vs the 16.5x EV/EBITDA multiple implied for the Australian business. There is clear risk to the downside to the implied Australian multiple.

The simple question becomes is it prudent to pay 23x current consensus FY18 estimates for a stock that just missed earnings for the first time in years and has entered an earnings downgrade cycle?

AIM’s answer is no and we expect consensus earnings estimates to fall from 286 to around 270c over the next 12 months. As that happens we expect the P/E to concurrently fall from 23x to 20x and that equates to a price target of $54.00 for RHC. Yes, we think there’s potentially another $10.00 downside in RHC shares over the next 12 months.

Just because a stock is in a “defensive” sector such as healthcare doesn’t mean its share price is “defensive”. In Australia some of the biggest blow ups in recent times have been in “healthcare”, with stocks like Healthscope (HSO), Mayne Pharma (MYX), Sirtex (SRX) and the IVF names all falling sharply as both earnings and P/E have fallen.

To us RHC doesn’t look “defensive”, with a result that delivered both qualitative and quantitative issues and led to earnings downgrades.

Since the result a block of 790,476 RHC shares were sold through JP Morgan. This number is very similar to the last disclosed number of 804,017 shares the outgoing Managing Director owned. If the outgoing Managing Director has “cashed in all his chips” it could hardly be seen as a vote of confidence in RHC.

You may well look back and see the CEO change and large insider selling was a signal the best of growth and P/E was behind this stock. So far our thesis on that has been right but AIM believes there’s further to play out here over the next 12 months and we remain short RHC shares.

Aitken Investment Management is a Global High Conviction Fund led by Charlie Aitken. For more information please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire