Ramsay: The world has changed

Craig Collie

Regal Funds Management

We think Ramsay is one of Australia’s great corporate success stories. Since starting with a single hospital in Sydney’s North Shore in 1964, the company now operates 235 hospital facilities across Australia, Asia and Europe to be one of the largest listed hospital groups globally. It’s market capitalisation is $11.5b and stock price is up nearly 50-fold since it listed with 11 hospitals in 1997. Its success, in our view, has been built on three factors: operational excellence, aggressive and well-executed facility (brownfield) expansion, and favourable domestic market conditions.

Of the three factors, the most important in our view is market conditions. A competitive advantage for building hospital capacity quickly becomes redundant if there are no new patients to fill it.

Equally, you can be the best operator in the sector, but if industry profitability is declining and you are a large player in the market, it can be difficult to buck the trend. As Warren Buffet once opined:

When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.

And unfortunately for Ramsay, market conditions are in the midst of a significant downturn. This forms the core part of our short thesis on Ramsay, which I will now step you through in more detail.

The core drivers of industry growth are coming unstuck

Between 2006 and 2016 the Australian private health system grew by an average of 8.5% annually. Bulls will tell you this was underpinned by our aging population, a tailwind which will only strengthen as baby boomers enter their 80’s. However, the reality is that the aging tailwind at a macro level is gradual and only adds ~0.5% to growth each year. Industry growth was instead driven by three factors, all of which are now decelerating:

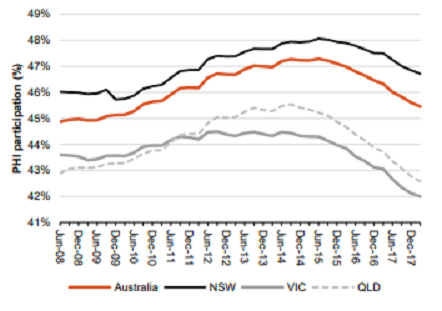

1: Insurance coverage is now falling

In 2006, 43% of Australians held hospital insurance cover. By 2016 this had climbed to more than 47%, and when combined with population growth meant that the number of people in the private system grew by ~2.6% pa. Fast-forward to today and growth of people in the system is zero. Rising co-payments from doctors, strong performance from the public hospital system and steep increases in insurance premiums (the average hospital policy price increased 81% from 2006-2016) has significantly undermined the value of health insurance. And worse still, this data does not capture those who have retained their insurance but downgraded their cover (in 2006 only 7% of policies had procedures excluded from cover vs. 44% today), meaning the effective number of procedures covered by the private system is now in decline.

Hospital insurance penetration is now falling in Australia

Source: APRA, Macquarie Research

2: Price increases for hospitals have nearly halved

Between 2006 and 2016 insurers gave hospitals price increases of ~40% per admission or ~3.5% pa. To provide a sense of how generous the insurers have been, we only need to look at inflation for other health services over the same period; for example pathology 0% pa, radiology 0% pa, GP fees ~+1% pa, France private hospitals ~1% decline pa and UK private outsourcing ~1% decline pa.

However this ‘gravy train’ (for lack of a better term) is fast coming to a close as the decline in insurance membership mentioned above means that insurers have started to get serious about keeping premium prices down. Industry contacts inform us that price increases for hospitals have already fallen to ~2% pa, with further pressure likely if Labor’s premium cap legislation is implemented.

3: Better oversight means doctors are reducing unnecessary operations

Contrary to common belief, the decision whether or not surgery is required is often subjective and contains many shades of grey. When we throw into the equation large information asymmetry seen in health care and strong financial incentives for surgeons to undertake procedures (a procedure can generate more than $20k of income versus as little at $300 if a patient only receives a consult), it is not difficult to appreciate that over-servicing could be a problem in the private system.

Whilst it is difficult to quantify the exact level of over-servicing, estimates are worryingly high. Prof Bruce Robinson, head of the MBS review and ex-Dean of Sydney University Medical School, has stated that 30% of health spend could be unnecessary. Other estimates in the medical literature suggest that more than half of the most common procedures are unnecessary; for example coronary angiography, knee MRI, inpatient rehabilitation and knee arthroscopy.

This is beginning to change however as the behaviour of doctors moves from a position of near-zero oversight to having at least some measurement and monitoring. In recent years we have seen the publication of the Atlas of Healthcare Variation which has informed us (among other things) that surgeons in South Australia are undertaking four times as many knee arthroscopies than their ACT counterparts, and that surgeons in North East Hobart were performing spinal surgeries nearly three times as often as their colleagues in Canberra.

Similarly Medibank has begun publishing intervention and complication rates for common surgical procedures (showing alarming variation in many instances). And in the coming months surgeons will for the first time see their own complication and intervention rates relative to their peers. Meanwhile health analytics company Lorica, which has access to all public and private hospital and specialist data in Australia, can now generate reports examining the quality of each surgeon and hospital in Australia on a range of metrics as specific as length of stay, infection rate and readmission rate. It can also identify which hospitals are systematically pushing their patients into often unnecessary admissions such post-joint replacement rehabilitation.

Unfortunately, consumers do not yet have access to this data, however this is changing as the drive to (at least some) transparency continues to accelerate.

Big data is shining a light on shadowy behaviour - a good thing for consumers but a headwind for hospitals

Ramsay earnings growth to rebase from 15% to 0-5%

Given the above headwinds, we believe industry sales growth will drop from the 8.5% levels seen historically to approximately 4-5% pa going forward.

And in terms of profits the impact will be even greater given the inherent operating leverage in the industry. Back when sales growth was 8.5% it was relatively easy for hospitals to generate 50 bps of margin expansion which, on relatively tight EBIT margins (~11%), boosted earnings growth up to 15% or higher. However with sales growth of 4-5%, margins are likely to stay flat (or even contract) as nurse wages, rents and utility expenses continue to rise. And when Ramsay’s struggling French and UK operations are thrown into the equation, we expect earnings to grow at 0-5% pa going forward, well below historical levels (15%+) and consensus expectations (10% pa).

Other alarm bells

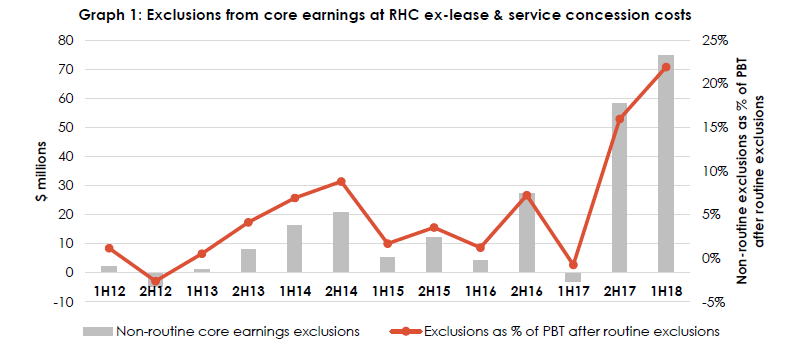

Several other concerns also contribute to our short thesis on Ramsay. Whilst the company met its earnings guidance for FY17 and is on track to do so again this year, it has had to make a number of questionable cost exclusions to do so. In fact the ratio of exclusions relative to PBT has risen from close to zero five years ago to more than 20% at the last result.

Ramsay has begun excluding costs in order to meet guidance

Source: Ownership Matters

Similarly, RHC’s cash flow has deteriorated in recent years. Assuming the trajectory of earnings in 2H18 continues from 1H18, RHC will report adjusted earnings in FY18 ~22% higher than in FY16. However its cash receipts will have declined by 2.6% over the same period. For a company with little (or even negative) working capital, this is hard to reconcile and, like the exclusion analysis above, suggests that real earnings may sit below what is being reported.

Also of concern is the performance of Ramsay’s peers in its key markets. Healthscope, its closest Australian peer, has seen its F19 earnings estimates downgraded by 38% as industry conditions have deteriorated. Similarly Spire, in the UK, has seen 56% earnings downgrades from Analysts, whilst Capio’s French division has seen forecasts for the current year now deteriorate into a loss.

For Ramsay meanwhile, domestic Analysts have only downgraded F19 earnings by 5% from their peak. We agree that Ramsay is a best-in-class operator with strong management expertise. However, given it is a large player in each of its markets, we don’t think it will be immune to the acute deterioration in conditions we have seen in each of its markets.

Postscript: Since RHC’s earnings downgrade on Thursday 21st June, FY19 estimates are still only 6.5% below their peak.

Regal has, or is likely to have in the future, a position in the securities which are mentioned in this article.

Further Insights

For more information on Regal Funds Management, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Craig is a Portfolio Manager at Regal, responsible for investing in health care across Australia and Asia. Prior to Regal, he led Macquarie’s health care research team, worked at Boston Consulting Group and practised medicine in Australia and the UK.

2 topics

1 stock mentioned

Craig Collie

Portfolio Manager

Regal Funds Management

Craig is a Portfolio Manager at Regal, responsible for investing in health care across Australia and Asia. Prior to Regal, he led Macquarie’s health care research team, worked at Boston Consulting Group and practised medicine in Australia and the UK.

Expertise

Craig Collie

Portfolio Manager

Regal Funds Management

Craig is a Portfolio Manager at Regal, responsible for investing in health care across Australia and Asia. Prior to Regal, he led Macquarie’s health care research team, worked at Boston Consulting Group and practised medicine in Australia and the UK.

Expertise

Comments

Comments

Sign In or Join Free to comment