RBA loses housing debate

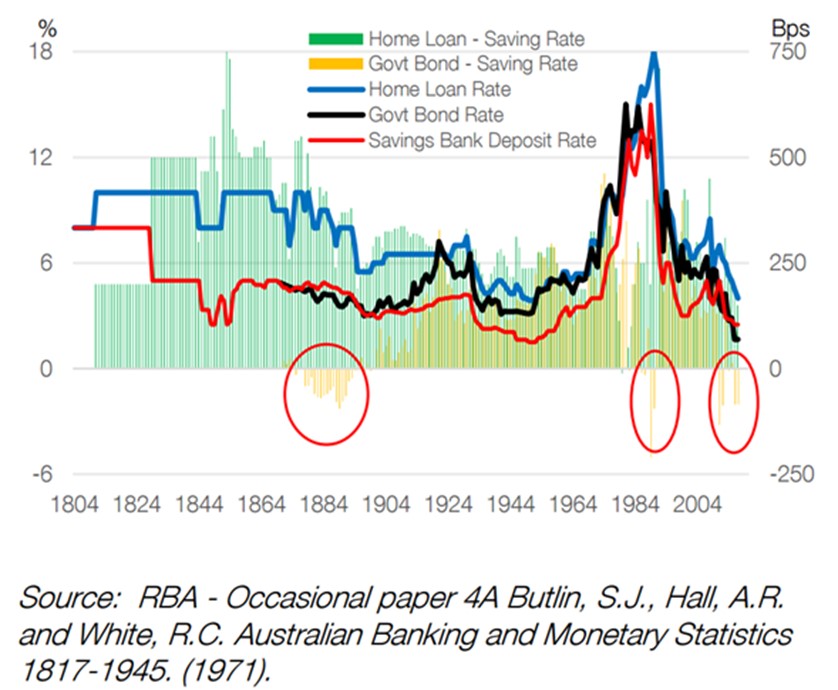

In The AFR I argue that the ABS house price index results released this week show that "the crazy, multi-week debate we had last year on the accuracy of Australia's house price data was—as we argued—a furphy designed to rationalise, or distract attention from, the otherwise irrational rate cuts bequeathed on borrowers in May and August that simply blew a bigger bubble". I go on to assert that the aggressive constraints on credit creation that APRA is having to impose on banks to thwart the RBA's cheap money policies will have no affect at all on non-banks, which are bouncing back care of a booming securitisation market (as we predicted last year). And after reviewing fascinating new data published by CBA on home loan rates over the last 200 years (yes, they are among the cheapest ever seen today despite an economy that is growing normally), I suggest that there is little value left in credit markets other than the major banks' senior bonds and their hybrids. Click here to read full article for free; excerpt below:

"As expected the ABS's quarterly index results have started converging back in-line with the 10 per cent dwelling price inflation recorded by the daily hedonic CoreLogic index (after adjusting for an upward revision due to a sample enhancement in April). The 2016 house price growth is especially sprightly considering home values had already leapt 28 per cent between January 2013 and December 2015 (according to both the ABS and CoreLogic). Rewind back to mid 2016 and the Reserve Bank of Australia was advising any journalist who would listen to ignore the rapid rise in the timelier CoreLogic index, which had for a decade been its favoured gauge, because an expansion in the sample of sales included in this index---the largest of any proxy published---created a one-off 0.8 per cent revision in April that upgraded the preceding 5 years of growth. Over the 12 months to September 2016 the ABS's index implied house prices were inflating at a benign 4.1 per cent clip compared to CoreLogic's friskier 7.1 per cent (netting out the revision). Yet as Goldman Sachs highlighted this week, the December jump in the ABS numbers to around 8 per cent annualised is "consistent with our preferred measure of house prices from CoreLogic [with] the higher frequency data from the latter suggest[ing] house prices have continued to reaccelerate into 2017". CBA's economists concurred, commenting "today's [ABS] data shows that both measures are headed higher, just at slightly different rates"...The only other assets I like with any "credit beta" are highly liquid and secure senior-ranking bonds issued by the major banks, which are insulated from a rating downgrade if Standard & Poor's lifts Australia's economic risk score (only an unlikely sovereign downgrade will nudge them to A+). If you can invest in them, I also don't mind major bank hybrids that offer "spreads" above the cash rate 150 basis points above their post-crisis "tights" in mid 2014. Most other non-government bonds have rallied in price such that their spreads have compressed back to, or through, those expensive 2014 levels, which for mine is a technical profit-taking signal."

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The shift toward scarcity: a playbook for a new era of investing

Talaria Asset Management