RBA's dilemma: Aussie interest rates among the highest in developed world

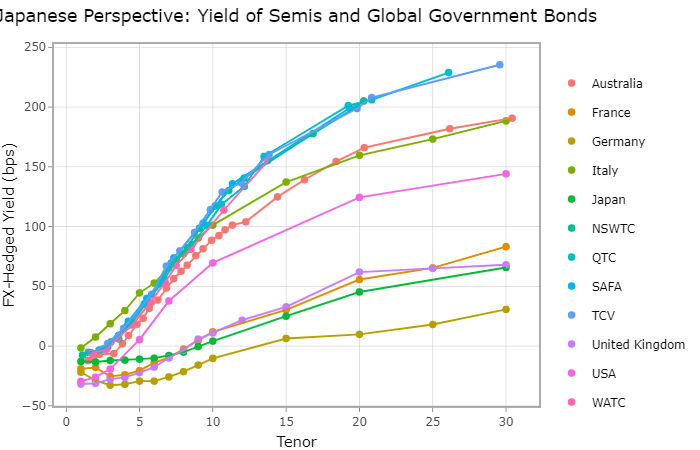

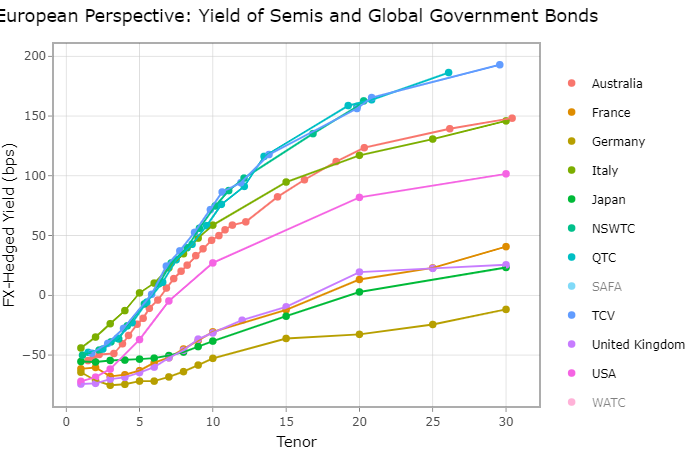

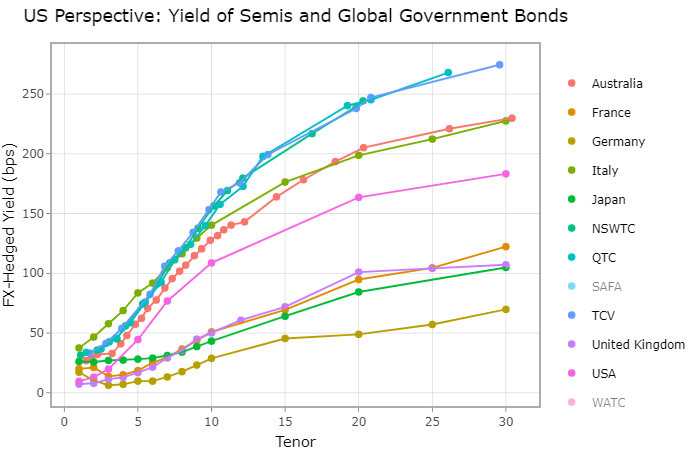

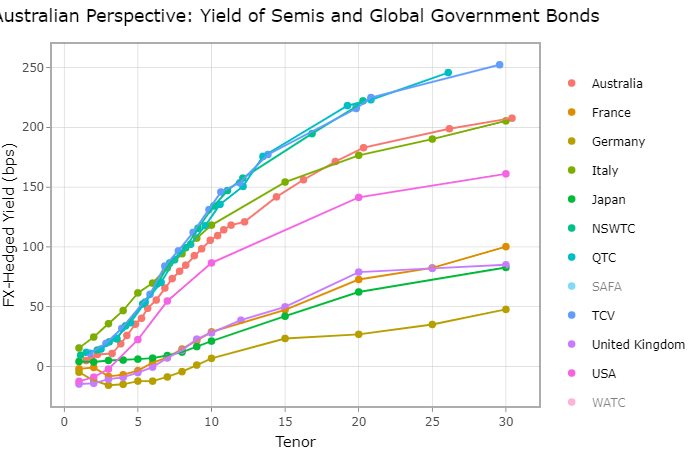

The RBA's dilemma is very neatly explained by these charts, which are screen-shots from our internal systems (see below). They show that the interest rates on both Australian Commonwealth government bonds and State government bonds (semis) are the highest in the world in Aussie dollars or when hedged into pretty much any currency, including USD, JPY and EUR...

The semis are the three blue/green lines up the top of each chart. Australian Commonwealth government bonds are the second-highest pink line in the chart. The vertical axis shows the yield that a Japanese/European/US/Australian investor gets hedging these bonds into their own currency. The horizontal axis shows the time to maturity in years out to a maximum of 30 years.

It is quite remarkable to see the interest rate on Commonwealth government bonds (pink line) hedged into USD/JPY/EUR (or held in AUD) is actually on par with if not superior to the yield offered by BBB rated Italian government bonds (the green line just below it), which are a favoured high-yielding asset for bank liquidity books in Europe and some central banks.

Yet what really stands out are the interest rates on Australian State government bonds (semis). Despite being rated AA to AA+, which is in line with the ratings on US and UK government bonds, Aussie semi yields in outright terms or hedged to JPY, USD, or EUR are among the most attractive high-grade sovereign securities you can find.

The problem is that these high yields attract foreign buyers, which in turn puts upward pressure on the Aussie dollar. This then places downward pressure on economic growth and slows Australia's recovery from the COVID-19 crisis and the path back towards full-employment, which is the RBA's main aim right now.

One recent example of this was a new 2025 bond issue held today by the Victoria government agency TCV, which attracted a record of $6.6 billion of bids from investors for a deal that was ultimately sized at $2.5 billion. It performed well on the break, tightening as much as 3 basis points. And it was reported that foreign central banks, attracted by the world-beating yields on Aussie semis, were some of the buyers...

The RBA's dilemma is what to do when its current quantitative easing (QE) program expires in April. This $100 billion initiative has been crucial in keeping our government bond yields, and the Aussie dollar, much lower than what they would otherwise be.

There is no doubt that in the counterfactual involving no RBA QE both our interest rates and the exchange rate would be trading materially above their current levels.

The RBA has more or less committed to expanding its balance-sheet such that the Australian economy is no worse off than other countries in terms of the competitiveness of our exchange rate and risk-free rates (or the governments' cost of capital).

As most would know, the challenge for the RBA is that the vast quantities of QE launched by other global central banks make Australian bond yields look very attractive on a relative basis compared to the suppressed yields available on alternatives overseas.

Another driver is, of course, simply the fact that Australia has outperformed pretty much all of the other major powers in terms of its ability to effectively eradicate COVID-19 and normalise our way of life.

The first QE 1.0 program initiated in November 2020 has been an experiment of sorts, partly for the RBA to understand the impact of its purchases on market function and liquidity. One concern mooted late last year was that the RBA's purchases of semis might adversely impact secondary liquidity because of the scarcity of bonds available.

This has proven to be quite the furphy: in practice, the RBA has been offered massive quantities of semis that are multiples the value of the bonds it has purchased, so much so that it has consistently bought these assets very cheaply on spreads (prices) that are wider (below) the prevailing spread (price) on the day. In fact, it did exactly this today.

Economists like Bill Evans at Westpac and his peers at ANZ and NAB expect the RBA to extend its current asset purchase program beyond May. While the RBA's overnight cash rate has reached its lower bound of 0.1%, and the banking system is awash with more funding than it needs via the RBA's $200 billion Term Funding Facility, extending the current QE program for another six months seems like a very sensible strategy.

One important feature of the RBA's QE program is that it does not raise the same financial stability concerns that reducing its cash rate has historically done. Because almost all Australian home loans are either variable rate or short-term fixed-rate, the level of longer-term 5 year to 10 year government bond yields does not have any real impact on housing market dynamics.

Access our intellectual edge

Coolabah Capital Investments is a leading active fixed income manager, specialising in liquid, high grade credit. Our large investment team covering Sydney, Melbourne, and London is equipped with deep quantitative credit research capabilities. Click the ‘CONTACT’ button below to get in touch with us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment