Resource stocks haven't run their race yet

Over the past quarter, much of the small-cap index outperformance over large caps has been due to the excellent returns of small resource companies. Given their cyclical nature, is that a reason to look elsewhere? The following note makes it clear that we think not.

Junior resources in best shape for a decade

To recap an observation from mid-2017, we remarked that as a group, resource stocks were more conservatively capitalised than industrial names (ie. when looking at net debt/market cap and other leverage measures) and carried more cash. In fact, the quality and financial strength of the small resources sector has not been as strong in over 10 years.

In our view, this balance sheet strength means these companies as a group are well placed to sustain a downturn, and furthermore, worthy of investment provided that desirable growth attributes that we seek are present at an attractive valuation.

Index has just started to turn back up

While there was a significant move in the Small Resources Accumulation index in the back half of last year, the longer term chart of this index shows that it is still at a relatively low level.

Indeed, the relative performance between small resource companies and small industrial companies is stark.

The question of course is, can the recent rally in resources continue? And consequently, should you have a meaningful exposure to the space?

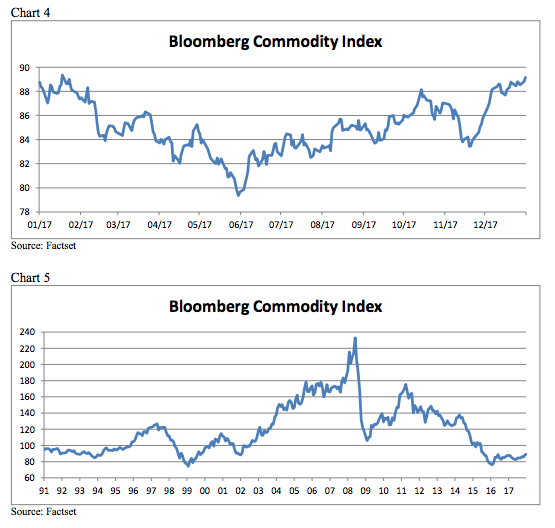

Commodities just starting to bounce

In answering the above questions, it’s constructive to understand where we are in the cycle, and the drivers of performance. A key input and driver of resource company valuations is obviously commodity prices. While the Bloomberg Commodity Index (a broadly diversified commodity price index) in Chart 4 shows that commodity prices have bounced off their lows in recent months, the longer term view (Chart 5) highlights that the index has barely bounced in the context of the last 25+ years.

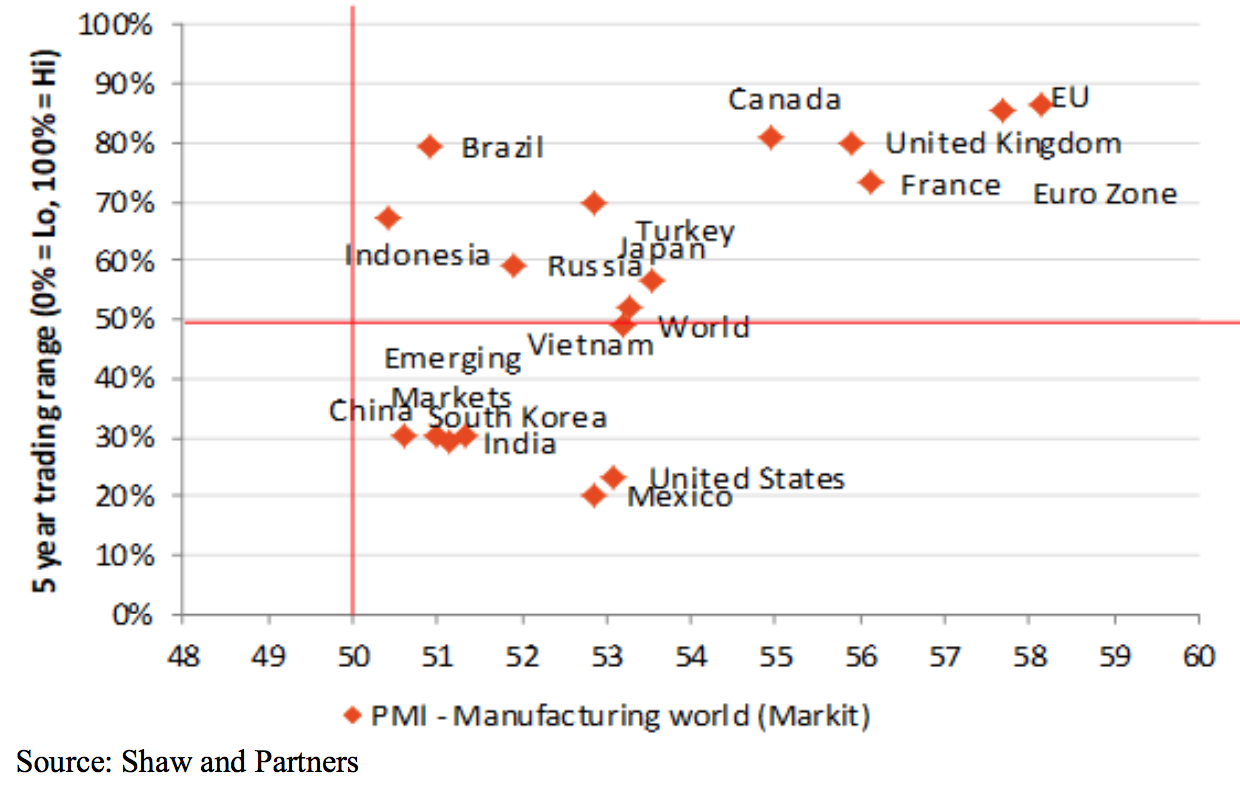

Synchronous economic expansion in all key economies

The reason for recent commodity price improvements is reasonably clear. The economic backdrop is supportive with synchronised global growth for the first time in years. Economic reforms in China, and Trump’s corporate tax cuts in the US help further. All major PMIs are in expansionary territory – a reading >50. In this environment, demand for various commodities tends to be high, exerting upward pressure on prices.

The improvement in commodity prices has unsurprisingly coincided with the improvement in share prices of resource companies.

Back to the question of whether the Small Resources index can continue to rally, we are of the view that it can. When considering that commodity cycles can last several years, and that commodity prices are reasonable from a long-term perspective (plus the valuation of resource companies are certainly modest compared to many industrial companies), we feel that a meaningful exposure to (growth-oriented) resource companies is still warranted.

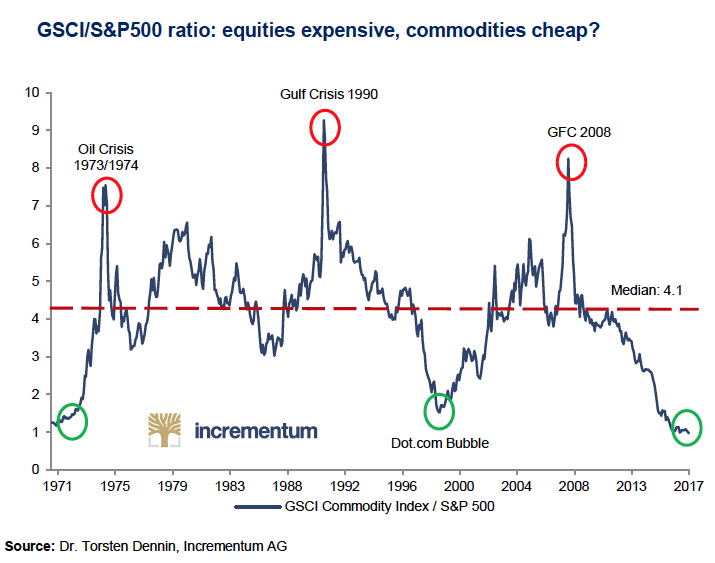

Commodities very cheap relative to equities

It’s worth keeping in mind one of our favourite charts (below) which shows the relative performance of the S&P GS Commodity Index vs the S&P500. The chart illustrates that we are currently at a multi-decade extreme with commodities as an asset class having underperformed (US) equities for around a decade. This looks like a turning point with commodity prices in our view likely to outperform.

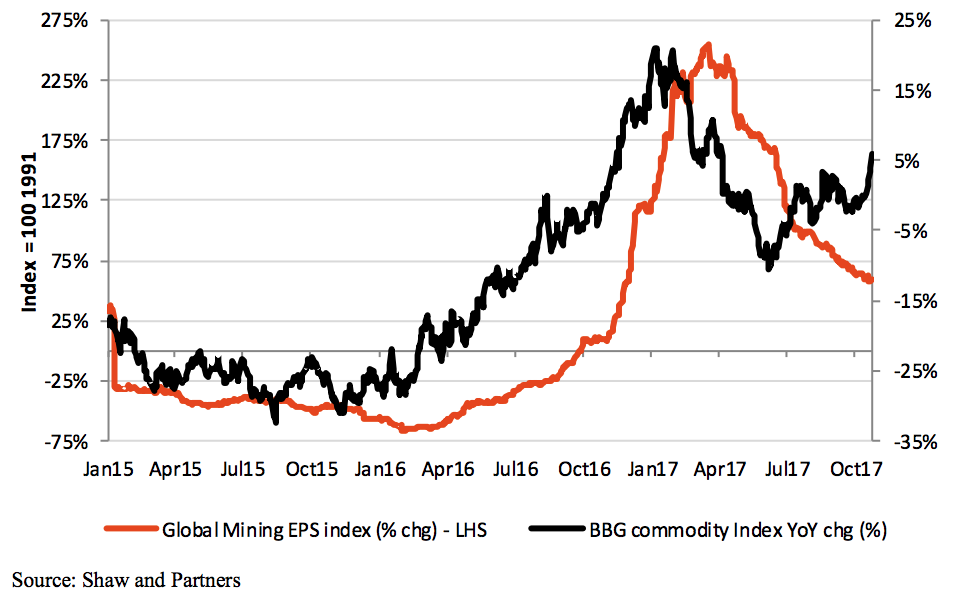

Earnings upgrades coming?

Finally, a brief comment on earnings. We believe that the next leg of a resources rally will require an improvement in earnings to justify further price performance. While this hasn’t begun in a wholesale way, the next chart shows that the rate of decline in the Global Mining EPS Index has moderated.

However, an improvement probably not too far away given recent moves in commodity prices (indeed, positive EPS revisions can be seen from the likes of BHP Billiton and Rio Tinto).

Note that the Bloomberg Commodity Index (measuring commodity prices) year-on-year change in the chart above has recently started to show a positive return, again suggesting that meaningful EPS improvements are close.

We would expect EPS upgrades to drive valuation metrics of resource companies higher, and thus continued share price performance.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

5 topics

2 stocks mentioned

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

Expertise

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

Expertise

Comments

Comments

Sign In or Join Free to comment