Resources v Industrials – a Growth vs Value conundrum

The significant outperformance of Resources over Industrials since February 2016, is a major factor contributing to the recent underperformance of Value managers like IML, compared to Growth and Momentum strategies which I discussed in a recent wire.

Resource stocks by virtue of their nature fit the designation of chasing growth. IML always takes a cautious view on Resources given their high volatility and unpredictable earnings. Resource companies’ earnings and dividends remain beholden to the movement in underlying commodity prices, which remains totally unpredictable – as clearly seen in the last few years in the wild swings we have seen in the prices of commodities such as oil and iron ore.

In January 2016 commodity prices reached decade lows (yet still above longer-term averages), beset by global oversupply, tepid economic growth and significant concern for China’s financial markets. However, the Chinese Government responded with significant amounts of stimulus which helped many commodity prices to rapidly recover and in turn to a significant rally for Resource companies.

IML has always preferred to invest in a diversified portfolio of good quality Industrial companies. This method of investing in quality Industrial companies allows us to model out the earnings streams of these companies into the future with some degree of certainty. Such a diversified portfolio of good quality Industrial companies will also provide a predictable income stream in the form of dividends over time.

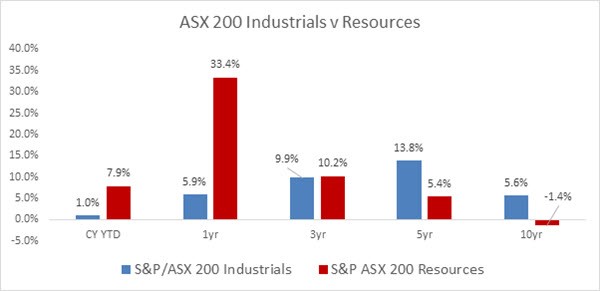

While at times a difficult market for value investors, we remain confident in our long-term approach and point to figure 1 below highlighting the long-term performance of the Industrials and Resources sectors. It is worth highlighting that the Resources sector returns are negative on a total return basis over 10 years.

Figure 1: ASX Industrials v Resources

Past performance is not a reliable indicator of future performance. Source: Dow Jones S&P Indices, 31 May 2018

What are we buying and why?

We have been buying the following companies on current share price weakness, companies which we believe have very resilient earnings, and strong management teams, yet whose share prices are all being impacted by factors which, in our view, are temporary in nature. We believe these investments will serve IMLs portfolios well in the longer term.

Amcor

A resilient global packaging company which is currently under pressure due to higher input prices and uncertainty around their emerging markets businesses. Amcor generates strong cash flows and has been relatively inactive on M&A for a while now as target businesses have been excessively priced. If reasonable acquisitions don’t eventuate, the focus will return to capital management which has been a key facet of Amcor’s strategy for capital deployment in the past.

Brambles

A global pallet pooling business, currently trading on 16.5x PE, with benefits still to come from productivity increases in its US pallet business. Brambles’ share price is currently trading lower because of fears that increases in lumber and transport costs will impact margins.

Pact Group

A rigid plastic packaging company which has diversified their business into contract manufacturing and materials handling. Concerns around organic growth from recent results have weighed on the share price, however we think Pact has a very strong management team, and is a durable business which can grow earnings over time via continued cost-outs and bolt-on acquisitions.

Caltex

A leading fuel distributor in Australia with a hard-to-replicate infrastructure network across the country. The share price has been weak of late due to slower near-term earnings growth as refining margins have declined and the company transitions from a franchise model to company operated.

Transurban

A toll road operator with a quality portfolio of roads spanning Sydney, Melbourne, Brisbane and the US, currently offering investors a 5.1% dividend yield with strong growth. Transurban’s share price is currently weighed down by uncertainty surrounding the WestConnex sale process.

Tabcorp

Has high quality, long term licences underpinning its franchises. Its key assets are its lotteries, wagering and gaming services businesses which are generally defensive in nature and highly cash generative. The short-term pressures on the share price mainly relates to its wagering business where yields and revenues are being adversely affected by a combination of unfavourable racing results, and competition intensifying ahead of the implementation of ‘point of consumption’ taxes across multiple states. We expect these issues will normalise over the medium term.

We continue to remain disciplined in continuing to focus on the fundamentals of all the companies we invest in and we seek to not over pay for companies that are often over promising and on companies where the outcome is often far from certain. With many companies’ valuations stretched, we continue to believe that portfolios underpinned by value and quality stocks remain the best place to be.

For further insights from IML's investment team, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality and value'.

Anton arrived in Australia in the 1980’s and was soon drawn to the sharemarket at a time when high-flying entrepreneurs dominated the headlines. His passion for investing in the sharemarket has not waned and he continues to put his considerable experience and the important lessons learnt over the last three decades to mentor the IML investment team and to deliver to clients' expectations.

1 topic

6 stocks mentioned

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Comments

Comments

Sign In or Join Free to comment