Rio: A bit of a mood killer

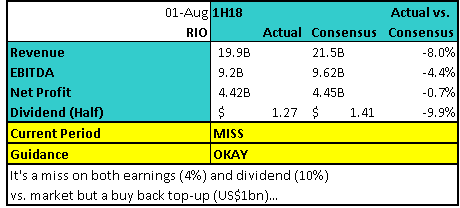

Rio Tinto (RIO) reported 1H 2018 results after market with a number of clear takeaways. This was a weaker than expected result pretty much across the board from an 8% miss on the top line down to a 4% miss at the EBITDA level and a lower than expected dividend.

While the result was a solid uplift year-on-year, the momentum on the half was clearly an issue, particularly in iron ore which has weighed on the overall numbers. 6 from the last 8 interim reports from RIO have surprised on the upside leading mostly to positive moves in the stock price.

Wednesday evening’s result should lead to weakness, particularly given recent share price strength plus some divergence from underlying commodity prices. Importantly, recent trends have shown that selling persists following a disappointment like this, so it could take some time before Rio retests its recent highs.

Where was the BIG capital management initiative?

There are some offsets in the result that are positive and these mostly come around capital management initiatives with an additional share buy-back of $1.0B, to be undertaken on the London listed shares. Importantly, this is on top of their current buy-back programme with about $1.4billion of that one remaining i.e there is now a big $2.4bn buy back in place, however given the level of asset sales they have had – about $8.5bn in the past year, there is clearly more room to move, and the market was looking for some more clarity around when and how that might happen.

The balance sheet for RIO is in tip-top shape, with gearing languishing at just 10%. They have clearly outlined plans for CAPEX which was below market expectations, and they’re flush with franking credits which may lose appeal if Shorten gets the top job at some stage next year.

They announced an expansion of an existing program but nothing earth shattering as the market had hoped. It will happen, and it will be supportive of the share price when it does. The question now is, from what level will the shares be supported?

Is it still a buy?

Taking a step back and thinking about the results with a wider lens, they did confirm the upward trend the company has followed since early 2016, with profit growth at ~12% on the year, dividend growth of ~15% on the year while debt remains low.

This is a good story and the journey is not yet over, however the market has simply gotten ahead of itself. Shaw’s very well regarded Mining Analyst Peter O’Connor has RIO in his buy bucket, and I think that’s the right call on a 12 month view, however buying higher lows rather than new highs is the way to play this (and other commodities at this point in the cycle).

Rio Tinto (RIO) Chart – targets $74 on the downside

But remember…

At some point inflation will rear its head if global growth continues at its current clip, wages will rise and central banks will be forced to jack up interest rates further, an environment where commodities and the companies that mine them do well.

While its hard to sugar coat a soft result, Rio is a stock to buy into weakness, with our technical target sitting at $74.00, or ~9% lower.

--

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

2 topics

1 stock mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment