Rise up! How high could US bond yields rise?

Global bond yields have started to lift over the past year after several years of trending down. This post examines how structural and cyclical factors have affected US bond yields over recent years and what a “normal” level of US bond yields might look like going forward.

We can’t blame inflation for lower bond yields

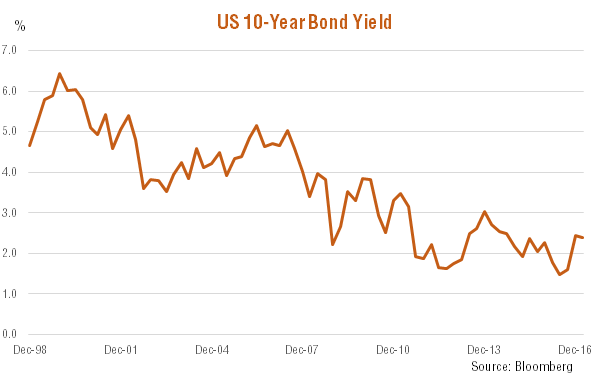

As seen in the chart below, US 10-year government bond yields have trended down over the past few decades, from an average of around 4.75% between the late 1990s until just before the financial crisis, to around 2.25% since early 2011. Yields reached an historic low of 1.38% in July 2016. Since then yields have lifted back up to around 2.6% due to policy tightening by the Federal Reserve and expectations of fiscal stimulus from US President Donald Trump.

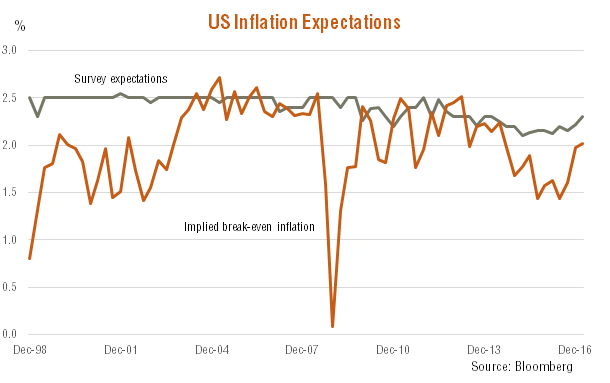

But despite all the talk of low inflation, it’s perhaps surprising to observe that reduced inflation expectations don’t appear a major driver of the decline in bond yields in recent years.

Indeed, as seen in the chart below, long-term inflation forecasts (from professional analysts regularly polled by the Federal Reserve Bank of Philadelphia) have dropped only modestly in recent years – from around 2.5% to 2.25% in the aftermath of the financial crisis. The implied break-even inflation rate (based on the difference between nominal and indexed 10-year bond yields) has also remain broadly steady, albeit somewhat lower and more variable than the survey-based inflation expectation – due to the added liquidity premium that attached to nominal bonds over (less liquid) indexed bonds.

Weaker economic growth only partly explains lower real yields

As seen in the chart below, if we subtract long-term professional forecasters’ inflation expectations from nominal bond yields we can derive a measure of implied “real” bond yields – which have declined from an average of around 2% prior to the financial crisis, to around zero in more recent years. What accounts for this decline, and can these factors last?

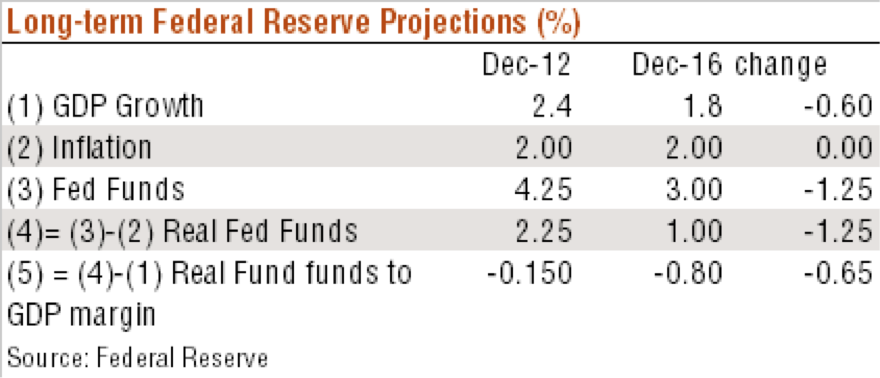

One factor that would most clearly support a structural decline in real bond yields is lower potential economic growth. In fact, the table below details changes in long-term forecasts for economic growth, inflation and the federal funds policy rate by Federal Reserve members between December 2012 and December 2016. As seen, even in only the past four years, long-term expectations for annual US economic growth by Fed members has declined from 2.4% to 1.8% – a 0.6%p.a. decline. Population ageing and weaker trend productivity growth appear to account for the growth slowdown. All else constant, this decline in growth expectations would justify a lowering in real bond yields of around 0.6% – due to a lower implied real Fed funds policy rate.

But as is also apparent in the table above, with inflation expectations unchanged, Fed members have also effectively dropped their implied long-run real fed Funds policy rate by 1.25pp – from 2.25% to 1% – twice the decline implied by the decline in trend GDP growth. Fed members seem to believe that the “neutral” real Fed funds rate is now somewhat lower relative to trend economic growth than has been the case in the past. One possible explanation could be more cautious attitudes by households toward the use of debt due to both population ageing and the lingering shock of the 2007-08 financial crisis.

We can’t forget about the term premium!

If the Fed is right and the long-term nominal Fed funds rate in coming years will be around 3% (1% real given 2% expected inflation), it suggests nominal 10-year bond yields will need to be at least this level – if not somewhat more. After all, relative to simply investing in cash, holders of long-term debt face day-to-day capital volatility and longer-term uncertainty with regard to the future level of interest rates and inflation – as such they typically demand a risk or “term” premium for effectively lending on a longer-term basis.

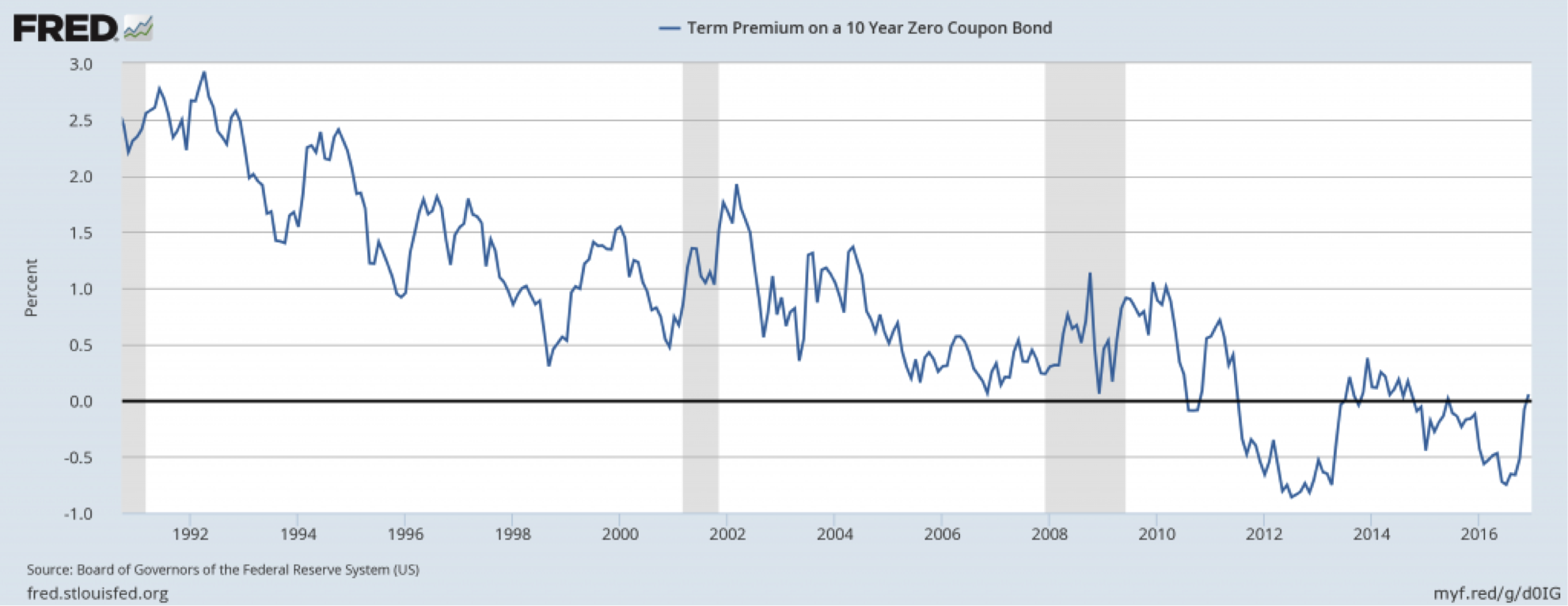

Studies which attempt to estimate this term premium, however, note that it tends to be quite cyclically volatile but has also tended to trend down in recent years. As seen in the chart below, one estimate suggests the term premium has in fact been negative in recent years – perhaps reflecting the Fed’s QE program – but has recently lifted back toward zero. Given this volatility, it’s hard to know with clarity what the term premium will tend to average in coming years, but a reasonable guess is that in more normal times it will be at least 0.5%.

Fair-Value US 10-Year Bond Yields around 3.5%

All up, the above analysis suggests that a reasonable “fair-value” estimate for US nominal 10-year bond yields over coming years – allowing for structural changes – is around 3.5%. This reflects an assumed long-run “neutral” Fed funds rate of 3% and a term premium on 10-year bonds of around 0.5%. At around 2.6% at present, this suggests US 10-year bond yields have already moved about half-way from their mid-2016 low toward their long-term fair-value, but further yield gains seem likely in the year ahead. That said, a much larger rise in yields – back to the levels that prevailed prior to the financial crisis – seems unlikely given contained inflation expectations, weaker US potential economic growth and a notable drop in the Fed’s perceived neutral real Fed funds rate

Original blog here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

1 topic

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management