ServiceNow: mission-critical, with no competition

The digital transformation of the enterprise is a long-term trend which is now accelerating as a direct consequence of the COVID-19 pandemic. Privileged business models operating with the benefit of this structural tailwind, therefore, should be considered carefully for investment opportunity. ServiceNow is rare in that it operates a privileged ecosystem business model, built in software – which carries superior economics, delivering mission-critical building blocks required by the enterprise and has no meaningful competition today.

ServiceNow owns enterprise services

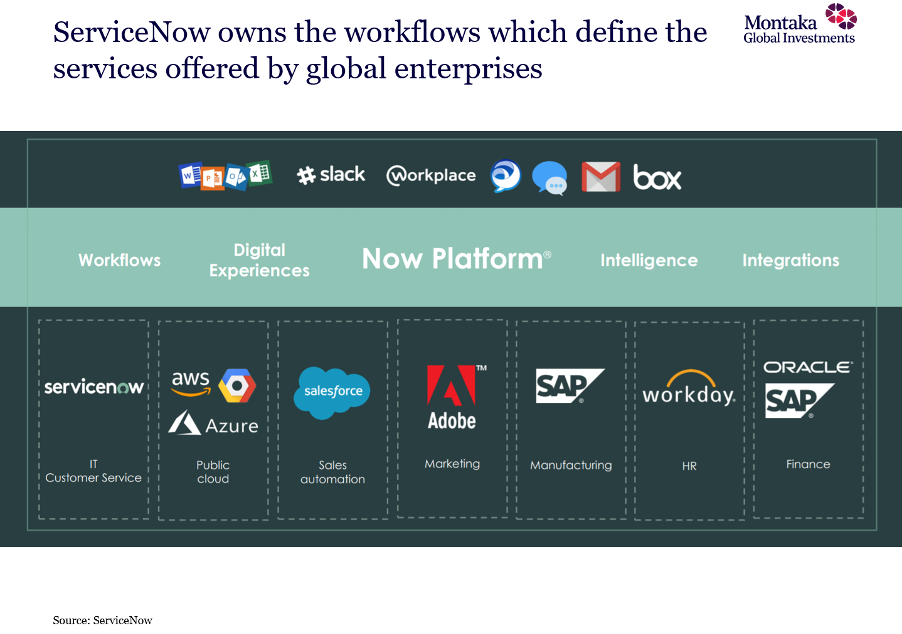

Thinking abstractly, the operations of any enterprise is simply a large collection of services. A service typically takes the form of human employees interacting with a multiple software applications in a pre-defined manner (called a workflow).

In most large enterprises, these workflows are defined and delivered by ServiceNow. The services that are delivered are measured, evaluated and optimised by ServiceNow. Unlike most software applications, ServiceNow is not trying to disrupt other enterprise application. ServiceNow is aiming to become the “operating system” of the enterprise – enabling employees to more efficiently deliver services across all functions, as illustrated below.

Importantly, all of ServiceNow’s applications (as well as those developed by third parties) are built on its Now Platform – a single platform, with a single data model on a technology stack owned by ServiceNow from the application layer all the way down to its datacentre infrastructure, located all over the world. It is one of the few technology businesses not reliant on the hyperscale cloud providers today.

ServiceNow serves more than 6,000 of the world’s largest enterprises today, including Goldman Sachs, JP Morgan, Disney and even the US State Department. It consistently delivers a best-in-class 97% retention rate. And interestingly, 80% of its new business which drives its 30% p.a. top line growth stems from existing customers – as they leverage the Now Platform more fully throughout the internal enterprise operations.

ServiceNow generates cash flows of the highest quality

There are three key reasons why ServiceNow’s cash flows are of the highest quality: (i) ServiceNow’s core workflow offering is mission-critical in the enterprise; (ii) ServiceNow operates with no meaningful competition; and (iii) ServiceNow extracts far less value than it adds.

To demonstrate the latter point, ServiceNow’s largest customers spend around $20 million per annum, far higher than the average ~$1 million per annum across all of its customers. But for these large customers, the $20 million annual payment to ServiceNow is in the context of an IT budget greater than $8 billion!

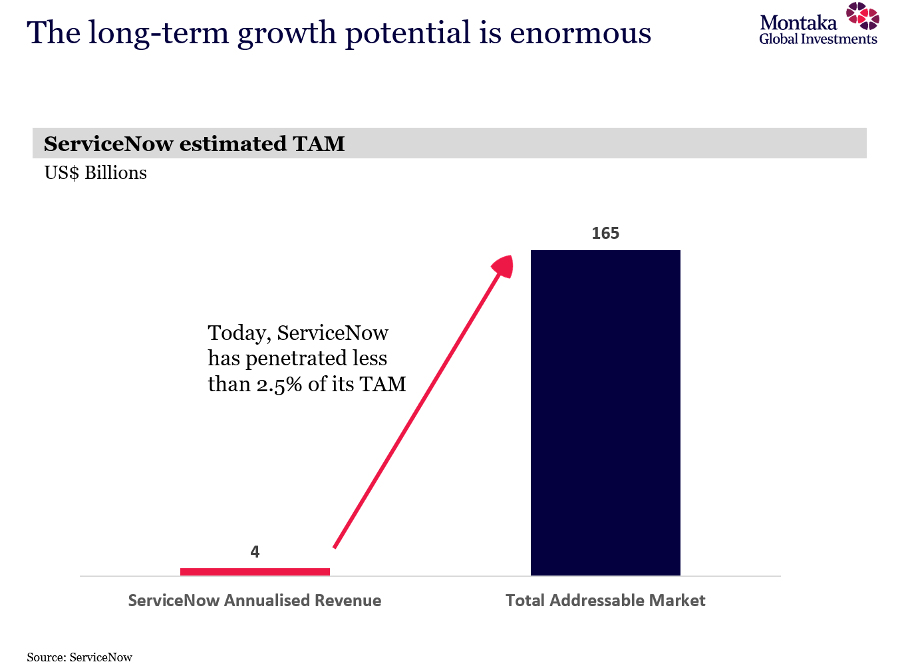

We believe ServiceNow extracts far less value than it adds. And the company believes this too, pointing out that for every $1 spent by a customer, roughly $5 of productivity gains are created. And in the context of an estimated $165 billion total addressable market (versus company annual revenues of just $4 billion today), one can see a very long runway ahead for growth.

ServiceNow’s cash flows are of the highest quality because they are resilient, predictable and growing. And through this lens, there is genuine question to be asked about the appropriate discount rate that should be applied to the valuation of such cash flows – especially in the context of an interest rate environment that will very likely remain near zero for the foreseeable future.

ServiceNow’s advantage will extend with its data

Given ServiceNow’s complete ownership of its Now Platform across the entire technology stack, it owns a particularly privileged data set on the world’s largest enterprises from which it can (and does already) develop predicted AI-based tools to further enhance the value proposition of its applications for its enterprise customers.

For example, ServiceNow has only recently rolled out its AI-enabled virtual agents, predictive intelligence and performance analytics tools in its core IT service management product – and already 80% of new customers are opting for this higher-value offering. But the existing customer base remain only 15% penetrated today – a penetration level that ServiceNow confidently believes will evolve to 100% over the coming years.

We seek to own the long-term winners in attractive markets. And we believe there is a very high probability that ServiceNow will remain a winner in enterprise services and workflows for decades to come.

* * *

Compound your wealth over the long-term

Montaka Global Investments provides investors the opportunity to compound wealth over the long term through disciplined global investment strategies and a sophisticated approach to risk management. Click 'FOLLOW' below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

4 topics

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets