Seven factors driving the gold price

Gold’s surge into the $4,000s highlights powerful demand drivers, supply limits, and why the metal remains both compelling and volatile.

Is the gold boom turning to a bust, or is this only the first phase of a much bigger cycle? The bull case depends on why you own gold and how you choose to hold it. The “what” and “how” matter as much as the “whether.”

Gold is a greater fool investment

I'm going to start with a huge disclaimer. Investors buy gold not because they expect a return from it, but rather because they expect other investors to want to pay more for it in the future.

The real problem with gold is that these arguments work at almost any price. If you are buying gold because you expect central banks to buy gold then it doesn't really matter whether the price is $3,000 or $30,000.

Gold is especially jumpy when narratives collide. And at the moment the narratives are mostly all heading in the upward direction. Inflation scares, geopolitical shocks, currency swings, and central bank headlines all land in the price at once.

Gold demand is driven by investors and central banks, whose buying and selling decisions have far greater influence than traditional uses such as jewellery or technology.

Total annual supply from mines and recycled gold is around 5,000 tonnes. Jewellery and technology demand is 40% of that. The rest is from investors and central banks.

And occasionally investors and central banks sell and turn into net sellers, which can cause big changes in the gold price.

The Seven Reasons People Own Gold

There are several motivations behind owning gold, and in today’s market, most of these factors are pushing in the same direction—upward.

1. Anti–US Dollar Position

Gold is priced in US dollars, so a weaker dollar generally supports stronger gold prices. As a globally recognised asset, gold’s value often rises when investors seek alternatives to dollar-denominated holdings.

A weak US dollar recently has been a key driver of the gold price.

2. Inflation Hedge

Gold’s reputation as an inflation hedge is better in legend than practice.

Gold was an extraordinarily great inflation hedge during the high-inflation 1970s. It was a terrible inflation hedge in the 1980s and 1990s where inflation was lower than the 1970s, but still high.

Still, many investors hold it as protection against the long-term erosion of purchasing power. High inflation expectations have contributed to the higher gold price.

3. Safety Trade and Geopolitics

In times of market turmoil or geopolitical instability, gold is viewed as a “safe haven” asset. Its physical, finite nature gives it appeal when confidence in financial systems weakens.

With Trump throwing most of the traditional world order into chaos, gold as a safety trade has continued its appeal.

4. Tail-risk Insurance Hedge

Some investors hold physical gold as insurance against societal breakdowns—such as war or infrastructure collapse—believing it could preserve value even if traditional systems fail.

Having said that, if you worry about war, grid failure, cyberattacks, or sanctions, the form of your gold matters. An ETF won’t help you if markets close and ATMs are down. Small-denomination physical metal is more practical in a true emergency.

Are these risks higher than in the past? Maybe. I will suggest social media is increasing the number of information echo-chambers. Which means the perception of this risk is probably higher.

5. The “Greater Fool” Factor: investors

At times, gold rallies are fueled by speculative momentum, where investors buy simply because they expect other investors to buy at higher prices later.

Investment demand has been particularly high for the last nine months.

6. Central Bank Demand

Central banks have become major gold buyers, with holdings now exceeding US Treasury exposure.

This trend has been driven since 2022 by concerns over asset seizures (as seen with Russia) and a shift toward de-dollarization amid trade and political tensions.

But Trump and his tariffs have created an increased demand in 2025. When countries see how Trump treats allies like Brazil or Canada, you can understand why they might want to diversify away from US dollar assets.

7. Return to a Gold Standard

While unlikely, some political figures—such as Donald Trump—have floated ideas about relinking currency to gold. Even if remote, speculation about such possibilities can move markets.

These seven drivers are currently aligned, explaining the exponential rise in gold prices. However, unlike stocks or property, gold lacks a clear fundamental valuation metric—its worth is simply what someone is willing to pay.

Gold Supply and Production Constraints

Gold is inherently difficult and expensive to mine, and no major new discoveries are expected to dramatically increase supply in the near term.

Unlike commodities such as iron ore, gold production is fragmented across many small-scale mines, often with low ore grades. This structure limits the industry’s ability to rapidly ramp up output in response to rising prices.

For existing producers, especially those with low costs, rising gold prices add less leverage than investors might expect—because margins are already high, an extra dollar in price doesn’t translate into large percentage profit increases.

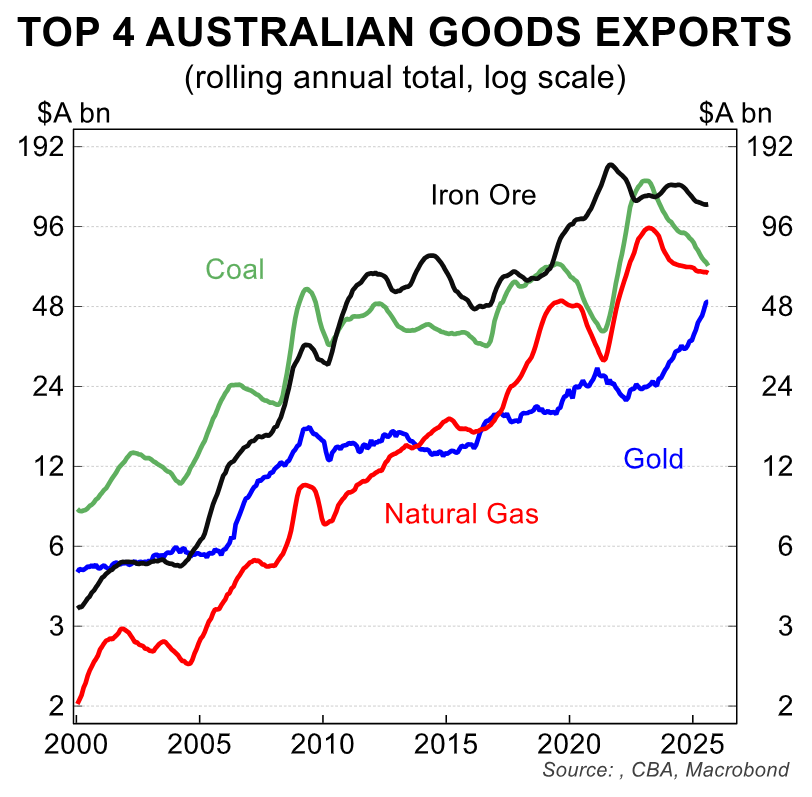

Gold’s Impact on Australia

Gold is a major Australian export, and if current prices persist, it could rival coal, natural gas, or even iron ore in export value.

However, Australia is not the world’s top gold producer, unlike its dominant position in iron ore or gas. Even a substantial increase in gold exploration spending—say, tripling to $5 billion—would still be modest compared to mega-projects like the $50 billion Gorgon gas project, meaning gold’s macroeconomic impact remains limited.

How to Invest in Gold

Investors can gain exposure to gold in several ways, each offering different levels of risk and potential return.

Investing in gold directly will get you maximum exposure to gold price movements. In contrast you will usually find that gold miners generally lag the spot price during sharp moves, both up and down. Their share prices tend to reflect a trailing average of gold—often over 12–18 months—rather than the immediate price. Sustained high prices are needed before miners fully catch up.

Direct Gold Bullion

Buying physical gold or bullion ETFs provides direct exposure to spot prices—either in US dollars or in Australian dollar–hedged versions. Our portfolios offer both as a tilt for investors.

Gold Mining Stocks

Mega-cap producers are diversified global miners with strong balance sheets and multiple operations. Their size reduces single-mine risk but limits upside leverage.

Mid-cap producers (typically valued at $5–10 billion) operate fewer mines and are often takeover targets during bull markets.

Small-cap producers tend to operate a single mine and carry higher operational and geopolitical risk, requiring careful diversification. Typically you will get more leverage to the gold price - both on the upside and the downside.

Explorers have no current production and are focused on proving reserves—these are high-risk, high-reward plays suitable only for deep research or diversified baskets.

Our portfolios allow investors to add more of the first two categories to their account.

Currency Hedging Decisions

Australian investors can also choose whether to hedge gold exposure to the AUD. Keeping it unhedged provides exposure to both the gold price and potential US dollar strength, while hedging separates the gold trade from currency fluctuations.

Inflation Protection

Will gold “work” as an inflation hedge? It depends. Gold does well when inflation surprises to the upside or when inflation fear rises faster than real yields. It does less well when inflation is high but stable, especially if real rates are positive and rising.

The 1970s were a poster case because inflation kept surprising. In the 1980s and 1990s, central banks were credible, sold gold, and ran tighter money. Inflation did not save gold holders then. Context matters.

If your motive is inflation hedging, define the horizon. For a one- to two-year insurance policy against upside surprises, gold can help. For a 10-year, set-and-forget CPI hedge, gold is not a clean instrument.

Final Thoughts

Gold has no cash flows. That is both a feature and a bug. It is money-like, but it is not money. It does not grow earnings. There is no discounted cash flow anchor. That makes debates over pricing slippery.

If your thesis is “weak USD,” the logic for gold at $2,000 is the same as at $5,000. If your thesis is “central banks will keep buying,” the logic scales until central banks stop.

Guardrails

When assets are untethered to cash flows, you need guardrails. Here are three:

- Position sizing. Use gold as a diversifier, not a core growth engine. It protects the rest of the portfolio; it does not replace it.

- Timeframe. Match the instrument to the thesis. Fast moves: bullion. Sticky regimes: miners.

- Triggers. Gold should be an investment, not a religion. Write down the conditions that would make you add or trim—USD trend, real rates direction, ETF flow momentum, and confirmed central bank buying.

Reduce exposure if you see:

- A decisive turn higher in real yields while ETF flows roll over. That’s a double hit.

- Clear evidence that central bank buying is slowing or reversing across multiple jurisdictions.

- A sharp, durable USD rally on renewed US growth leadership and policy clarity.

Add exposure if you see:

- A risk-off shock where gold lags at first as investors sell everything to raise cash. That dip often reverses as the bid for safety returns.

- Policy signals that elevate gold’s symbolic role or constrain dollar liquidity to allies.

- A period where spot holds high long enough to push analyst decks up, but miners have not yet re-rated. That timing window can be attractive.

These findings were originally featured on Episode 392 of Nucleus Investment Insights, where we took a look into the gold boom.

Take us on your daily commute! Nucleus Investment Insights is available in Podcast form on iTunes and all major Android Podcast Platforms, including Spotify.

Be sure to subscribe to our channel on YouTube to get notified whenever we're going live.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

........

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

5 topics

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Comments

Comments

Sign In or Join Free to comment