Should the Reserve Bank of Australia give people money?

Anthony Doyle

Firetrail Investments

Many of us are now familiar with the impact of low interest rates on our savings. For those unhappy with the meagre return on cash and term deposits, spare a thought for those in Europe, Japan or Switzerland where official interest rates are negative.

Whilst the very idea of a negative interest rate confuses most Australians, imagine a world where borrowers are paid to take out mortgages. A mortgage with a negative interest rate means the borrower will pay back less than they borrowed. If this seems fanciful, it isn’t - last year a Danish bank launched the world’s first negative mortgage. This is possible because Danish banks can borrow from institutional investors at a negative rate, and simply pass on a less negative rate to their customers. The world of banking has been turned upside-down.

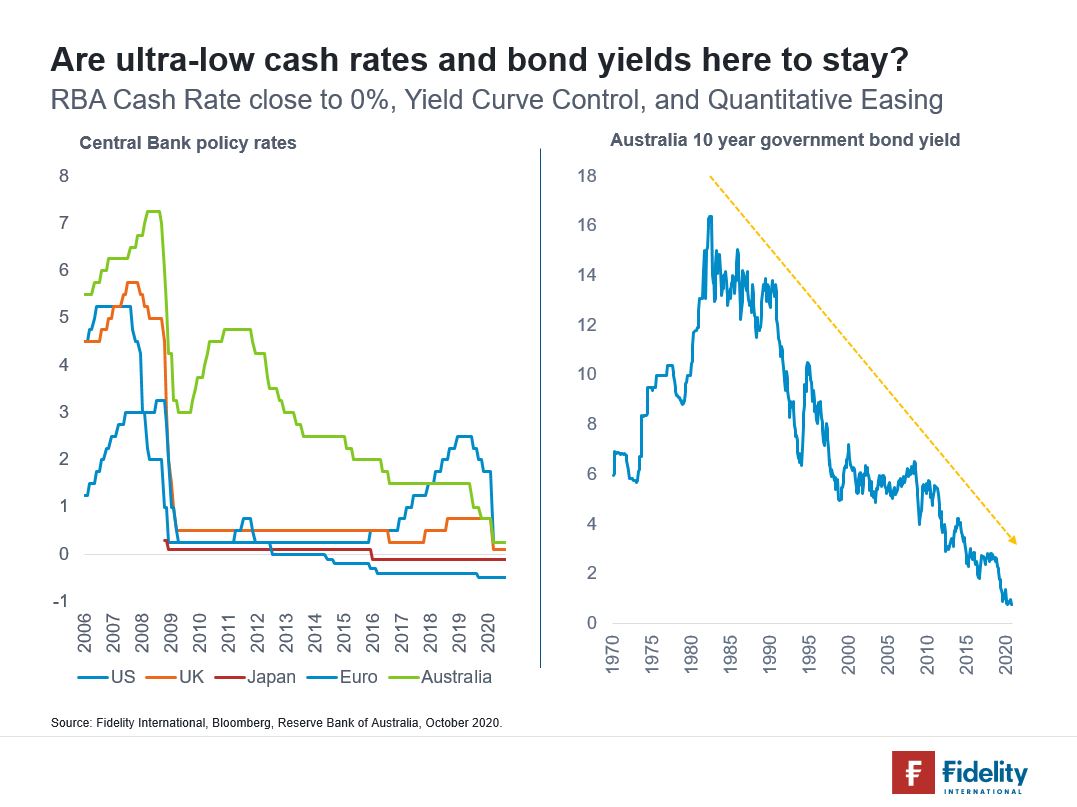

In addition to negative interest rates, central banks are quick to point out that they have developed a range of “unconventional measures” to support their economies. “Forward guidance”, “Yield Curve Control” and the “Term Funding Facility” are a few of technocratic sounding terms that the Reserve Bank of Australia has recently adopted in addition to reducing the Cash Rate to an all-time low of just 0.25%. Speculation continues to grow amongst RBA watchers that further monetary easing is inevitable as the economy struggles to generate inflation in an environment of deteriorating labour markets, weak wage growth, and rising insolvencies.

Central banks hope that unconventional monetary policy will lead to higher aggregate demand and higher inflation by reducing yields on government debt, which is a reference point for long-term borrowing by the private sector and households. But government bond yields are already very low, and it appears that the availability of credit is not an issue today. Instead, we are likely to see asset price inflation, as investors are increasingly herded into riskier asset classes to generate positive real returns. This of course benefits the owners of financial assets, which tend to be wealthier households who have the capacity to invest, while poorer households see their living standards stagnate.

It also appears that younger workers will be hit particularly hard by the Covid-19 crisis. Younger workers make up a large proportion of the workers in the most affected sectors like entertainment and recreation. Academic studies in the US have shown that being unemployed while you are young has long-term implications for future earnings. These earnings losses appear to be the result of lost work experience, falling labour market skills, relatively lower perceptions of labour market worth, and the negative connotations that unemployment has with employers.

So how can policy support those who are most impacted by the current crisis?

Australians are already familiar with the response of the Labour government after the global financial crisis - it sent people money. Today, fiscal policy has done a lot of the heavy lifting, with over 3 million Australians on the JobKeeper allowance which is due to end entirely in March 2021. However, could the central bank assist in financing payments to Australian households, potentially assisting in returning the real economy to growth?

In this scenario, a central bank could finance the transfers to households by creating electronic money, just like it currently does with quantitative easing or yield curve control. Rather than rely on the banks to lend the money, why not simply deposit it in the accounts of citizens on low incomes? In the spirit of the equality debate, higher earners or those whose income has been unaffected by the current crisis would not qualify.

Arguably, “helicopter money” would provide a more effective short-term aggregate demand hit than traditional quantitative easing, without the negative impacts on income inequality. So, what’s the problem?

Critics of helicopter money suggest that the multiplier effect - the amount of additional GDP created for every dollar of spending - may be less than has historically been the case, limiting the demand boost. Additionally, recipients may choose to pay down debt rather than spend the money. Finally, the independence of the central bank may be called into question leading to negative financial consequences such as rising bond yields and a much weaker currency.

Another more recent phenomenon has been development of central bank digital currencies (known as CBDCs). The Swedish Riksbank is already looking at developing a technical solution for Swedish Krona (the e-krona), the US Federal Reserve is “committed to understanding how technological advances can help the Federal Reserve carry out [its] core missions”, while the RBA thinks that “it will be important to closely watch the experience of other jurisdictions that are considering implementing CBDC projects”. In 2030, will every Australian have an account at the RBA? This could pave the way for the RBA to raise the money supply during the next downturn in an attempt to raise inflation and lower unemployment rates.

If this all sounds fanciful, Former US Federal Reserve Chairman Ben Bernanke has described helicopter money as a “valuable tool”. He has also noted that “under certain extreme circumstances—sharply deficient aggregate demand, exhausted monetary policy, and unwillingness of the legislature to use debt-financed fiscal policies—such programs may be the best available alternative. It would be premature to rule them out.”

When interest rates are close to zero, strange things happen. Australia is late to the low-rate party, giving the RBA and Federal Government some valuable insights into the unintended consequences of quantitative easing and unconventional monetary policy. Monetary policy’s huge distributional consequences and far reaching side effects will have important ramifications for Australians over the next decade. Direct transfers of money to those in our society that are suffering most as a result of the current crisis may be the best way of supporting the Australian economy.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire