Sigma: The future may be brighter than you think

Sigma is a wholesaler of pharmaceutical products. It acts as an intermediary distributor that buys drugs from manufacturers and sells them to the pharmacies that ultimately dispense these drugs to Australians in need. Some of these pharmacies operate under one of Sigma’s banners (see Figure 1), while others are independently branded. Sigma does not own any of the pharmacies itself.

Sigma also distributes a variety of non-prescription or over-the-counter products, such as beauty and personal hygiene products, many of which are exclusively distributed in Australia by Sigma (e.g. Serum7, Boots Laboratories, and Optiva).

Figure 1: Some of the pharmacies and brands operating under Sigma’s banners

A number of regulations in Australia govern the pharmaceutical industry. One important regulatory outcome for Sigma is the Community Service Obligation (CSO) Funding Pool. This taxpayer-funded pool supports pharmaceutical wholesalers who undertake to supply all of the medicines on the Pharmaceutical Benefit Scheme (PBS) to pharmacies across Australia within 24 hours of an order, regardless of a pharmacy’s location and the relative cost of supply. Participation in the CSO Funding Pool is not compulsory but its existence is a necessary part of ensuring that every Australian has ready access to essential medicines.

Sigma is one of five distributors/wholesalers eligible to participate in the CSO Funding Pool.

Sigma’s revenues come mainly from the sale of products to pharmacies but also from CSO receipts which subsidise otherwise loss-making sales to rural pharmacies and from low-value PBS products.

Some may describe Sigma’s business as ‘boring’, with relatively stable and predictable earnings. It has annual revenues of a little over AUD$4 billion and earns an operating profit margin of between 2% and 2.5% (including CSO receipts). Relative to other wholesalers in Australia, this level of profitability is normal and most would expect Sigma’s revenue base to increase in future, given Australia’s growing and aging population.

Two surprises

A number of unexpected events have conspired to make Sigma’s future far less certain, neither of which have been fully resolved and both of which have contributed to significant share price weakness and uncertainty.

- In May this year, Sigma’s largest customer, Chemist Warehouse Group (CWG), announced its intention to source certain products from a competitor on better terms than Sigma had been supplying them. CWG hoped to cherry-pick its drug procurement; the high-margin drugs would be bought on better terms from Sigma’s competitor and the low-margin drugs would continue to be purchased from Sigma. Quite a sensible commercial strategy, but one that Sigma took offence to as its trading arrangement with CWG was priced based on the entire basket of PBS drugs, not just the least profitable parts. CWG accounts for about 35% of Sigma’s total sales, but less than this in terms of profits, reflecting the favourable trading terms that CWG enjoys. Sigma and CWG have agreed to a temporary fix (presumably even better trading terms) that will apply until their contract expires in 2019. The future post-2019 remains very uncertain.

- In October, AstraZeneca, a large global drug manufacturer, announced it would bypass pharmaceutical wholesalers and exclusively distribute some of its higher value or higher volume products directly to pharmacies using DHL, a global logistics firm. While these products represented only 1% of Sigma’s total sales, this followed a similar decision in 2010 by Pfizer, another large drug manufacturer. Today, fears abound that other drug manufacturers will follow and that Sigma’s network of distribution assets will be bypassed on a much larger scale.

The sharemarket has dished out its own medicine, with Sigma’s share price falling from $1.30 in early May, to 75 cents soon after AstraZeneca’s news was absorbed.At the same time, the broader sharemarket was on a tear.

Acting in uncertainty

Having reflected on Sigma’s performance during the year, two things spring to mind: our sell discipline and our response to uncertainty.

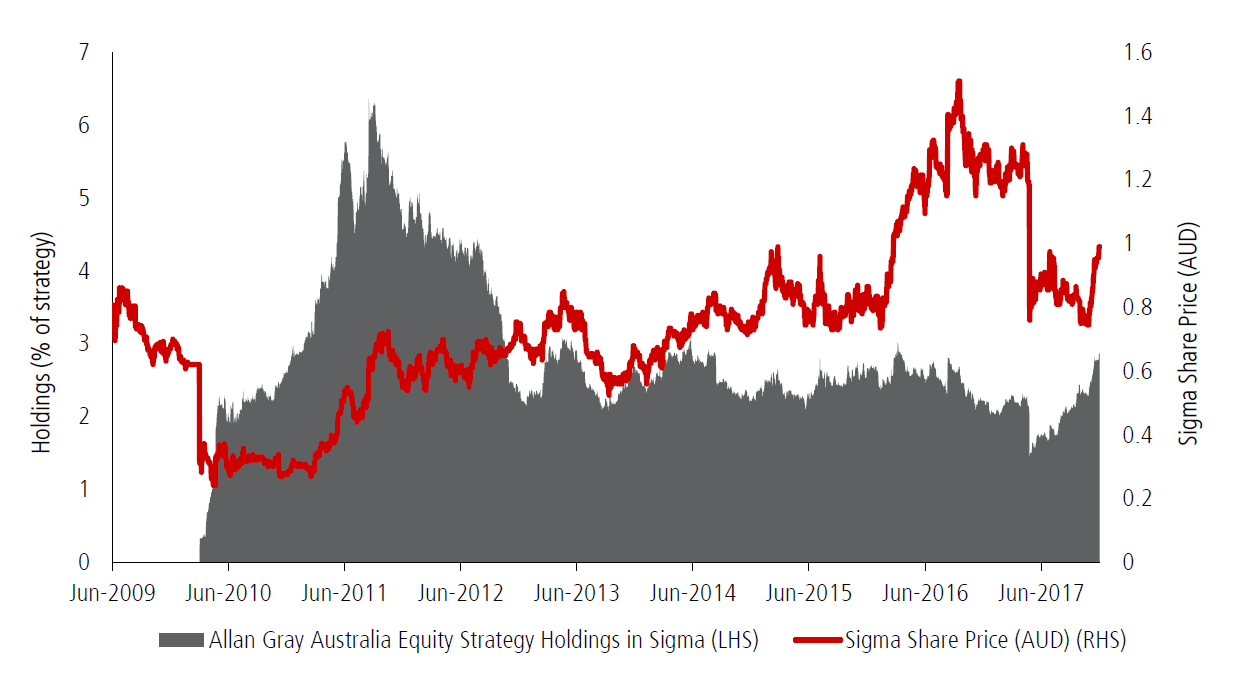

Despite having reduced the weight of Sigma in our portfolio by quite some margin prior to its weakness this year, hindsight tells us we were not aggressive enough. With the share price trading at, or close to, our estimate of fair value in 2016, we should have sold our entire holding. As reflected in Graph 1, we reduced Sigma’s weight in the portfolio from over 6% in 2011 to 2% immediately prior to the onslaught of Sigma’s bad news. We had sold some Sigma shares but, upon reflection, the allure of Sigma’s defensive earnings stream and high calibre management team affected our judgement and we could have sold them all. By late 2016, Sigma was priced for perfection with little upside and plenty of downside. These are the very payoff profiles we try to avoid when we make our first investments in companies.

Graph 1: Portfolio holdings in Sigma Healthcare compared with the share price

Source: 31 December 2017, Allan Gray. The Allan Gray Australia Equity Strategy includes the Allan Gray Australia Equity Fund and Institutional mandates that share the same investment strategy.

Acknowledging and learning from mistakes is important. Equally important is leaving the past behind and assessing an investment based on its future prospects without any emotional baggage. While in hindsight we made a mistake in not selling our entire holding in Sigma, the share price falls following bad news and great uncertainty forced us to look at the company again with fresh eyes and a clear mind. Sigma’s underperformance is a stark reminder of the discount the sharemarket places on uncertainty, particularly when investors have come to expect the opposite.

Seizing the opportunity

But it is in the face of severe uncertainty that we think opportunity knocks loudest. Yes, Sigma’s relationship with its largest customer is somewhat fractured. Round one with CWG has been resolved amicably, but round two looms large in the minds of investors. And yes, there are risks associated with drug manufacturers bypassing Sigma’s distribution network.

In investing, the price one pays should be paramount. Sigma’s uncertain future is now well appreciated by the sharemarket and, at least in part, reflected in the share price one pays today. At its recent 75-cents-per-share lows, the company traded at less than 10 times its forecast pre-tax operating profit and about 13 times its forecast after-tax earnings. This was a substantial discount to the broader sharemarket and, in our view, well in excess of what was warranted considering the range of possible outcomes. We increased our holding substantially.

Table 1: Sigma’s enterprise value to operating profit

Note: A company’s enterprise value is its market capitalisation plus its net debt. Source: Allan Gray; Factset, 31 December 2017

Sigma has since increased in price, but remains priced at a modest discount to the sharemarket.

It is hard to know whether Sigma’s future prospects are adequately reflected in the price one pays today, but we believe there is still relative value in owning the company.

Investors remain concerned about CWG moving its business to a competitor, but the downside in Sigma’s earnings are no more severe than the company’s discount to the broader sharemarket. And this is not a certain outcome. Even if it did happen, offsetting the impact on the company’s earnings would be a near $300m release in working capital that could be invested in other profitable endeavours.

The future may be brighter than people think

Amongst all the uncertainty, there are also silver linings. For example, there is a real possibility that the Australian Government stops manufacturers from exclusively distributing their drugs directly to pharmacies, as it makes it more difficult for CSO wholesalers to meet their commitments. This is arguably in the public interest, as the scheme’s purpose is to ensure ready access to essential medicines listed on Australia’s PBS. If the Australian Government did change the rules for manufacturers, the 1% revenue lost from AstraZeneca’s decision may ultimately end up being an 8% revenue tailwind as Pfizer’s drugs may also need to be channelled back through the CSO wholesalers (like Sigma). Anecdotally, this would also be supported by pharmacies, which would require less investment in working capital as CSO wholesalers are required to deliver within 24 hours. Pharmacies would also benefit from reduced operating complexity (and most likely cost) as they would deal with fewer suppliers.

It is easy (and important) to obsess about the downside when it comes to investing, but it is helpful to turn the coin over from time to time to get a balanced view of a company’s future prospects. Sigma’s future is far from risk-free, but we feel its future prospects are better than the sharemarket believes, despite the uncertainty around its biggest customer.

This extract is from Allan Gray Australia’s December 2017 Quarterly Commentary. For further insights from Allan Gray, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

1 topic

1 stock mentioned

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management