The 3 factors behind the LIC boom

Nathan Umapathy

Bell Potter

2017 was a big year for both Listed Investment Companies (LIC) and Listed Investment Trusts (LIT) with a record number of new and innovative entrants into the sector. LIC/LIT dominated capital raisings, collectively bringing $3.7bn via Initial Public Offerings (IPO). And this was further supported by a number of secondary market raisings that saw $1.2bn raised during the course of 2017.

In this piece, we recap the factors behind the LIC boom over the last couple of years. Plus, we elaborate on 2 major structural changes in the sector which we view as positive development for future LIC IPOs. You can access our full quarterly report by clicking here.

LICs flourishing for three reasons

The growth rate of LICs has been higher than that of managed funds. And we can associate this to 3 tangible reasons:-

- Future of Financial Advice (FoFA) reforms: As of July 2013, commissions paid to financials planners by providers of managed fund have been banned. This has removed the incentive for financial planners to use managed funds over LICs or Exchange Traded Funds (ETFs).

- A competitive dividend yield in comparison to the ASX200: In July 2010, there was a significant change in the Corporations Act that paved the way for LICs to offer greater consistency in dividends. Previously, LICs could only pay a dividend if they had an accounting profit, which saw a number of LICs being unable to pay dividends through the GFC. However, following the introduction of the solvency test, LICs now have greater flexibility to offer sustainable dividend policies even with the absence of accounting profit. Many LICs offer a grossed up yield higher than the Australian share market grossed up yield of 6.0%.

- Stronger demand from the growing Self Managed Super Fund (SMSF) market: An increasing number of investors are looking for greater control over their superannuation. The combination of rising property prices and prolonged low interest rate environment has resulted in a level playing field for alternative investment vehicles such as LICs and ETFs. SMSFs are a valuable investor base to cater for, as they now account for 28% of all superannuation assets in Australia and are growing.

Two structural changes

We also saw two structural changes which we view as positive developments for the sector in 2017. These changes were:-

- IPO Cost Absorption: Historically, the cost of a LIC IPO - generally a fee of 2-3%- was transferred to the shareholder at listing. As a result, for example, a $1.10 IPO will see an opening NTA of $1.06-$1.09. In late 2017. we saw a shift where LICs came to market with a proforma Net Tangible Assets (NTA) in line with its issue price. Managers of Magellan Global Trust (ASX:MGG), Spheria Emerging Companies (ASX:SEC) and VGI Partners Global Investments (ASX:VG1) absorbed the issue cost associated with its IPO, while MCP Master Income Trust (ASX:MXT) had its issue cost paid via a loan, which will be amortised by shareholders over the next 10 years. This enabled shareholders of MGG, MXT and VG1 to access these LICs at NTA on day one.

- No more bonus options: Bonus options issued at IPOs have generally been offered to investors to compensate for the issue cost reflected in the NTA. Investors who seek to purchase these securities in the secondary market, must be cautious of the potential dilutionary impact on the NTA of in-the-money options, as options expiry nears What is perhaps less understood is that the person who exercise these options is not diluted as they have received the benefit of a lower exercise price. As a result, bonus options can be sometimes view negatively by shareholders. With Managers choosing to absorb the vast majority of the IPO cost, LICs no longer have to offer options as an IPO sweetener. As a consequence, a number of LICs came to market without an option attached, removing the overhang that is cast around LICs close to option expiry.

We anticipate this will likely drive further interest and larger capital raisings that are likely to tip through $500m plus.

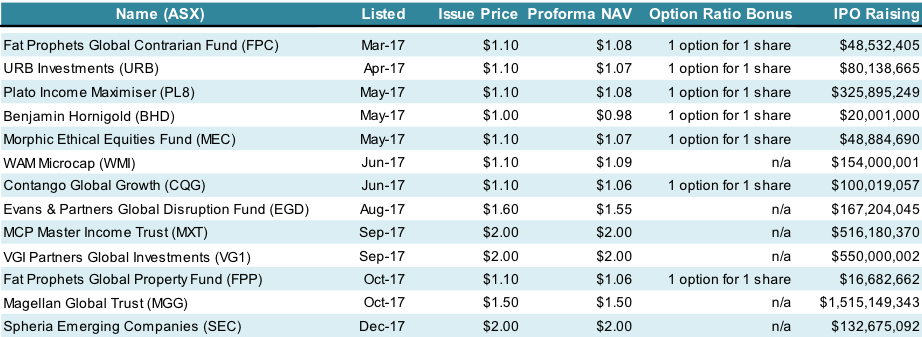

Table 2: LIC/LIT IPO’s - 2017

Initial Public Offerings

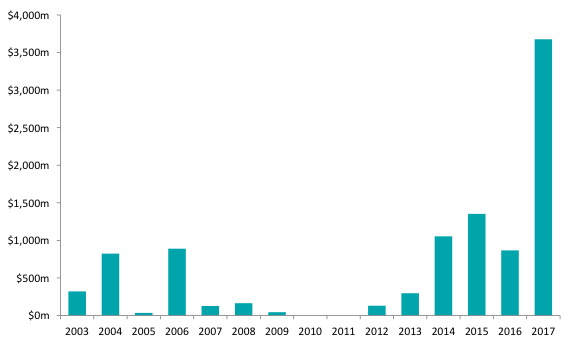

2017 was the best year for IPOs in the LIC sector since 2015, buoyant with positive market conditions. There were 13 new vehicles launched (including Listed Investment Trusts) raising over $3.0bn, the largest of which was the Magellan Global Trust (ASX:MGG), which raised $1.5bn in October.

Graph 1: Money raised from LIC/LIT IPOs - 2003 to 2017

Table 3: Of the top 10 IPOs for 2017, 6 are LIC/LIT

Of the new products, 6 were new International LICs — Fat Prophets Global Contrarian Fund (ASX: FPC), Fat Prophets Global Property Fund (ASX:FPP), Morphic Ethical Equities Fund (ASX:MEC), Contango Global Growth (ASX:CQG), VGI Partners Global Investments (ASX:VG1), Magellan Global Trust (ASX:MGG). We are still seeing huge demand for international products from Managers with a proven track record coupled with effective communication.

Investors search for yield has put LICs in the front and centre as Plato Income Maximiser (ASX:PL8), MCP Master Income Trust (ASX: MXP) and Magellan Global Trust (ASX:MGG) have promoted their products with the goal of providing investors with a strong yield. MXP was also the first and only LIT to offer corporate debt exposure on the ASX.

Capital Raising

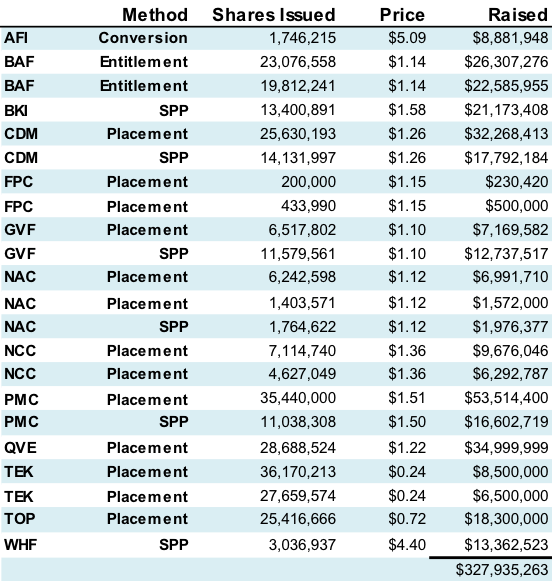

A total of $566m was raised in the secondary market through a range of Dividend Reinvestment Plans (DRP), Entitlement Offers, Placement Offers and Share Purchase Plans (SPP).

Table 4: CY17 Share Purchase Plans, Placements, Conversion & Entitlements

Full report here

You can access our full quarterly report by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nathan Umapathy is a research analyst who specialises in strategy and fundamental analysis of listed managed investments including Listed Investment Companies (LICs) and Exchange Traded Funds (ETFs). Joining Bell Potter in 2010, he gained a strong foundation in Australian and International Equities working under the head of research Peter Quinton before carving a niche for himself in listed managed investments. In his current role Nathan produces a range of LIC and ETF reports covering investment fundamentals, asset class structure and cost, and the role of managed investments in portfolios. He holds a Bachelor of Commerce (Finance & Econometrics) from the University of Melbourne.

4 stocks mentioned

Nathan Umapathy

Research Analyst - Listed Managed Investments

Bell Potter

Nathan Umapathy is a research analyst who specialises in strategy and fundamental analysis of listed managed investments including Listed Investment Companies (LICs) and Exchange Traded Funds (ETFs). Joining Bell Potter in 2010, he gained a strong...

Expertise

No areas of expertise

Nathan Umapathy

Research Analyst - Listed Managed Investments

Bell Potter

Nathan Umapathy is a research analyst who specialises in strategy and fundamental analysis of listed managed investments including Listed Investment Companies (LICs) and Exchange Traded Funds (ETFs). Joining Bell Potter in 2010, he gained a strong...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment