Six simple steps to improve decision-making

Joe Wiggins

Aberdeen Standard Investments

The study of behavioural economics allows us to better understand the decisions we make. We show how behavioural finance can lead to better investment decision making. We explore the inherent biases we must overcome to achieve our long-term investment goals. And we provide six tips to improve investment decision making.

Over the next fortnight, we will be digging deeper into the main themes that affect behavioural finance, as well as looking at ‘noise’, the random and irrelevant variables that affect our decisions, and some lessons from four books that changed the way we think about thinking.

The significant cost of the 'behavioural gap'

Behavioural finance aims to influence – and hopefully improve – our financial decisions. It helps us understand the gap between how we should invest and what we actually do. This ‘behavioural gap’ can come with a significant cost - sub-optimal investment performance.

“An understanding of our own behaviour should be at the forefront of every decision we make”

We exhibit a number of biases in our decision making. While we cannot remove these biases, we can seek to better understand them. We can build more systematic processes that prevent these biases adversely influencing the decisions we make.

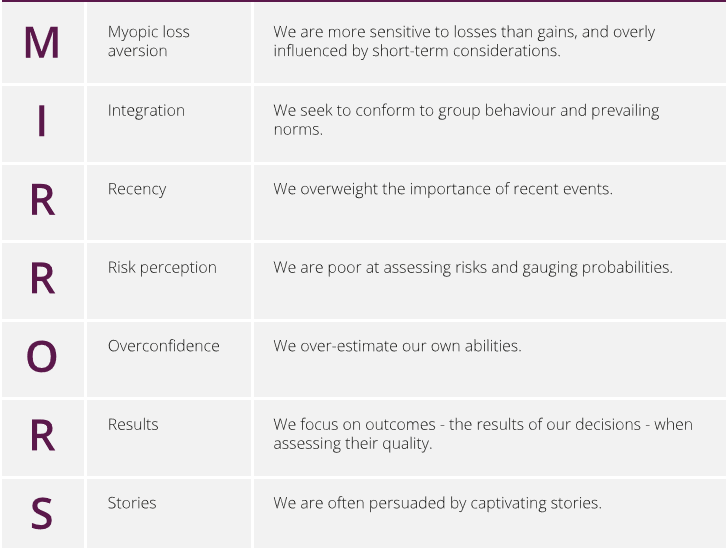

Investors should focus on those biases that are most likely to impact their investment decisions – and those supported by robust evidence. We have developed a checklist to reduce errors from the key behaviours that affect our investment decisions - ‘MIRRORS’.

Our decisions are affected by noise; random fluctuations in irrelevant factors. This leads to inconsistent judgement. Investors can reduce the effects of noise and bias through the consistent application of simple rules.

We offer six simple steps to improve decision making; three dos and three don’ts.

These six steps seem simple but are not easy. We cannot remove our biases, or ignore the noise. Instead, we must build an investment process that helps us overcome them.

What is behavioural finance?

Behavioural finance is the branch of behavioural economics that focuses on finance and investment. Behavioural economics is a common feature of our lives today. It has changed the wording of our tax request letters and the food options in our canteens, usually without us even noticing. There is a growing drive to better understand how we behave - and how this affects the decisions we make.

Behavioural economics is still in its infancy. It encompasses elements of psychology, economics, sociology, anthropology and other fields.

This combination is both a blessing and a curse. The attempt to marry lessons from different areas is refreshing, but can make the subject appear complex and difficult to apply in everyday situations. Yet the essence of behavioural economics is simple. It can be narrowed down to five questions.

- What is the problem or issue?

- What is our rational or optimal decision?

- How do we actually behave?

- What is causing this difference between what we should do and what we actually do?

- How can we alter behaviour to deliver better outcomes?

Case study: “Save More Tomorrow”

One successful application of behavioural finance is the “Save More Tomorrow” scheme for US defined contribution pension plans.

1. What is the problem or issue?

The movement from Defined Benefit to Defined Contribution pensions puts a greater onus on individuals to save for their retirement. However, people tend to either make minimal or no contributions to their pensions. This causes financial problems in retirement.

2. What would be considered rational behaviour?

Individuals should build a pension pot that can provide an acceptable standard of living in retirement. To achieve this aim, they should start saving early. This allows the power of compounding of long-term returns.1 And they should increase their saving rates as rising wages increase their disposable income.

3. How do we actually behave?

Shlomo Benartzi and Richard Thaler, the architects of the scheme, talk of a global “Retirement Savings Crisis”. Inadequate saving means many workers will have an inadequate pension income.

4. What is causing this difference?

There is a range of behavioural biases contributing to the problem, including:

- our tendency to think that the present is more important than the future

- limits to our self-control and

- our dislike of reducing our disposable income (or loss aversion).

5. How can we alter behaviour to deliver better outcomes?

Individuals who enrol in the “Save More Tomorrow” scheme agree to increase pension contributions every time their wages rise (up to a pre-defined maximum). This removes a number of the hurdles to achieving higher savings. By pre-approving future increases, individuals no longer sacrifice current spending. And by linking growth in contributions to rising pay, they never experience a loss in take-home pay through pension contributions.

A lengthy time period will be required to assess the long-term effectiveness of the scheme. However, early signs are encouraging. Initial participants saw their saving rate increase from 3.5% to 13.6% across four pay rises. It has proved particularity effective when used alongside auto-enrolment. This boosts participation because of our inclination to stick with the default option.

Simple steps can have a profound impact on long term outcomes.

Closing the behaviour gap

An understanding of our own behaviour should be at the forefront of every decision we make. As Charlie Munger, Warren Buffett’s business partner, put it:

“How could economics not be behavioural? If it isn't behavioural, what the hell is it?”

Failure to consider our behaviour can come with a significant cost – or ‘behaviour gap’. This gap is the difference between the returns on an underlying investment and the returns actually received by the investor. It can occur if investors succumb to behavioural biases and make poor decisions.

Closing this gap is difficult. Logic points in one direction and the human mind in another. We often struggle to believe the biases that lead to sub-optimal behaviour apply to us. Possible solutions are often counter to received wisdom. The unpredictable nature of financial markets seems designed to lure us into errors of judgement.

“The human mind is fundamentally not a logic engine, but an analogy engine, a learning engine, a guessing engine, and aesthetics-driven engine, a self-correcting engine". - Douglas Hofstadter

Schemes such as “Save More Tomorrow” show us the potential benefits of better managing our own behaviour.

Never miss an update

Stay up to date with the latest content from Aberdeen Standard Investments, including part II and III of our deep dive on behavioural finance, by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Aberdeen Standard? Hit the 'contact' button to get in touch with us or visit our website for more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

1 topic

1 contributor mentioned

Joe Wiggins

Senior Investment Manager

Aberdeen Standard Investments

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

Expertise

Joe Wiggins

Senior Investment Manager

Aberdeen Standard Investments

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management