Some low risk investments to beef up your defences

Elizabeth Moran

Elizabeth Moran Consulting

Lately, we’ve been on edge with domestic and global corrections happening. Here are four defensive assets to further guard your portfolio against impact.

You could be forgiven for thinking markets just keep going up given the long bull market we’ve experienced since the global financial crisis, but last month’s rocky sharemarket should set us straight.

Escalating trade tensions between the US and China, along with the US Fed increasing interest rates saw markets contract last month.

Some share markets were into official correction territory, down 10 percent plus, Sydney and Melbourne residential property continued to slide and prices of other risk assets were also down.

How did that make you feel? Were you glued to your screen watching, wondering where the rot would stop? Perhaps recalculating your capital balance and revising your expectations?

Maybe you were one of the lucky few to have ‘enough’ that a correction doesn’t worry you?

If you were jittery I think it’s a sure sign your portfolio allocation isn’t quite right. Depending on your age and capacity to generate an income, there comes a point where you need more defensive assets.. Here are four suggestions if you are looking to beef up the defensive part of your portfolio.

1. Government bonds

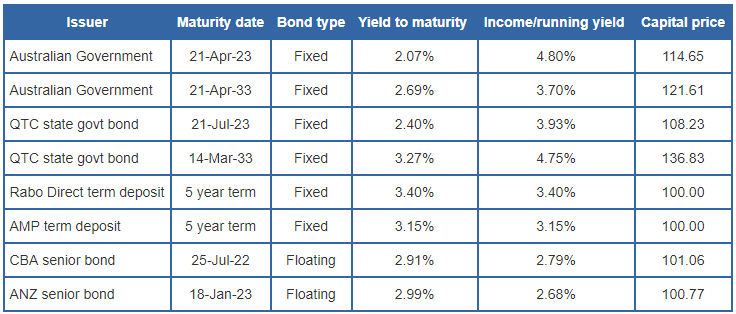

These could be US or Australian Commonwealth Government (ACG) or state government bonds.These are very defensive, liquid assets that are traded in huge volumes on a daily basis. Returns are typically low but investors know issuers will repay at maturity, preserving capital.

Most government bonds are fixed rate, so you lock in a known income. However, those issued some years ago locked in high rates of return and investors wanting known high income have paid more for these bonds, such as the ACG 2023 bond, which pays fixed 5.5 per cent per annum per $100 face value of the bond.

This bond was issued some years ago when interest rates were higher. The price has increased to about $114 and the overall yield if held to maturity is lower at 2.07 per cent per annum.

The downside with fixed rate bond prices is that if interest rates rise, the bond prices will fall. This particular bond pays a high income of 4.8 per cent per annum, effectively repaying the additional $14 capital value through higher income until maturity when its $100 face value is repaid to investors.

Government bonds have a ‘safe haven’ label and many of the world’s largest global institutions hold allocations to AAA rated government bonds. Australian government bonds are one of a handful of countries that still meet that hurdle.

Some of the funds pouring out of US stocks last month found new homes in US government bonds. The US 10 year Treasury rate is about 3.15 per cent per annum and high enough for investors to switch out of shares and into the bonds.

2. Australian deposits

Australian deposits are still guaranteed by the federal government up to $250,000 per entity per authorised deposit taking institution, giving them similar risk status to federal government bonds. A good rate of return for a year is about 2.85 per cent.

Deposits, however, have a few disadvantages: they can’t be traded like bonds, and if you want to access the funds early, you will be charged penalty interest.

Be wary about other accounts. Those that offer bonus interest are great but forget to make a deposit and interest could be as little as 0.5 per cent. I understand some cash accounts pay 1.9 per cent, about the same as inflation, and if you’re paying tax on that income you are actually going backwards.

Institutions and middle market clients can’t access ‘sticky’ retail deposit rates and, as they are paid less and usually have much larger sums to invest, they will often invest in senior bank bonds.

3. Senior bank bonds

Senior bank bonds are also considered ‘safe haven’ given they qualify as high quality liquid assets and are eligible for repurchase by the Reserve Bank.

This status applies to other securities as well – see RBA.gov.au for more details.

Senior bank bonds, which are low risk and very liquid, also pay low interest. Like government bonds, they’re tradeable and can earn higher than expected returns. They can also be fixed rate or pay floating rate interest, almost removing interest rate risk. Income on the floating rate bond changes with interest rate expectations.

These are great assets as they provide liquidity with very limited potential capital loss. For example, an ANZ senior floating rate bond with a four year term pays a yield to maturity of 2.99 per cent per annum.

4. Gold

Gold can be considered another safe haven investment as it is an alternative store of value. Unless you hold physical gold, the structure of the investment may limit protection in a severe downturn. Of course physical gold doesn’t pay any income but it has proven itself in past downturns.

Source: FIIG Securities

Note: Prices are accurate as of 2 November 2018

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

8 topics

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment