Stocks catching our eye into weakness… (EHL, BIN, CBA)

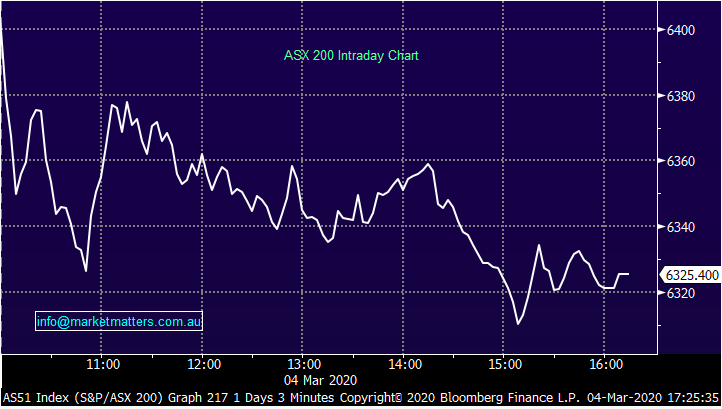

Down again today ending near the session lows despite the US futures trading higher throughout our time zone. Asian markets were also higher today benefitting from a weakening $US after Jerome Powell and co cut rates at an emergency meeting overnight. At the sector level today, financials again a drag while the gold stocks benefitted from safe have demand

From the peak of 7197 just 9 trading days ago, the mkt had a low of 6245 on Monday morning before closing todays session at 6325, the drop from high to low being a fairly stark 952pts / -13.2%. Not many places to hide in this market. When the dust does settle, there are some compelling buys – fear gripping mkts at the moment however that will change at some point.

Overall, the ASX 200 fell another -110pts / -1.71% today to close at 6325. Dow Futures are trading up +353pts/+1.34%

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE

A few stocks: While fear is front and centre here and now, some really compelling stocks starting to show their hand into weakness. While its hard to do, and taking losses on stocks is difficult for some, we need to try and put our blinkers on and think about the portfolio we want to have coming out of this turmoil. While there is a lot of rhetoric being written around whether or not to buy this weakness, the reality for a lot of us is that its now more about what we want hold as the dust settles – a good time to reposition portfolios into the chaos. Stocks that looks interesting here:

Ramsay Healthcare (RHC) hit from ~$81 down to ~$66

Webjet (WEB) whacked from ~$14.50 to ~$8.50

Altium (ALU) down from ~$42 to ~$30

BHP from ~$41 to $32

Macquarie (MQG) ~$152 down to $132

Z1P Co (ZIP) ~$6 to ~$2.80

Emeco (EHL) ~$2.55 to ~$1.80

Wisr (WZR) ~33c to ~15c…to name a few

Ramsay Healthcare (RHC) Chart

Banks: All the major banks have now announced that they will pass on the 25 bps rate cut in full to variable rate home loan customers. ANZ went a little further and reduced investor interest only rates by 35 bps, but that just brings them into line with their peers. ANZ and NAB said the interest rate changes are effective on 13th March. It’s the 24th for CBA and 17th for WBC. The standard variable owner/occupier P&I interest rates are: ANZ 4.54%, CBA 4.55%, NAB 4.52%, WBC 4.58%

In 1H20, CBA’s Australian loan to deposit spread increased by 4 bps from 2H19 to 1H20 and NIM increased by 1 bps. Whether or not they can repeat this performance in 2H20 relies on the action they take on deposits and how depositors react. In terms of earnings impact for CBA in real terms, this one cut is not a major issue - by passing on the full cut rather than 20bp which they would have liked, this hurts their net interest margin by 2bp or more widely, impacts their earnings by 1% - not a huge issue now but it becomes one if more cuts happen and the Government continues to put pressure on them to pass on in full. Interestingly, reports emerged today that the Government would have increased the bank levy had the cut not been passed on in full – seems extraordinary.

CBA Chart

Elsewhere today: While the market tumbles, small pockets of good news are popping up – and the market isn’t giving the stocks the credit they deserve – understandable. Emeco (EHL) -5.73%, took a hit with the market today despite having their credit rating upgraded to B+ by Fitch. The release from the ratings agency said “that Emeco’s business profile has improved following its acquisition of Pit N Portal.” A big reason why EHL is trading so cheap is because of its high debt levels, leveraged at 1.77x operating EBITDA as at the half year result last month, carrying $US409.1m in net debt. A ratings upgrade will make it easier to refinance when the time comes, and highlights the progress the company has made over the last 12 or so months.

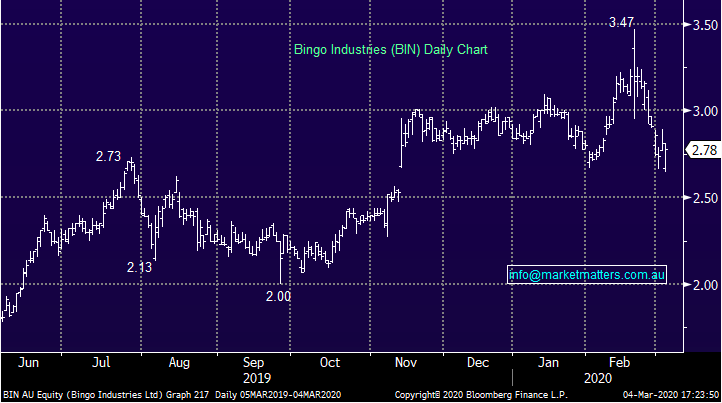

Another one of our holdings, Bingo (BIN) -1.07%, has also come off with the market, though there look to be some underlying trends in their favour despite the economic slowdown. This week Scott Morrison announced some changes to procurement rules which will make it move viable to source recycled products – more demand out of Bingo’s recycling facilities. While the Victorian government has also announced they will almost double the states land fill levy to bring it in line with NSW over the next few years. While landfill volumes will fall as a result, it will push more waste into the higher margin recycling facilities Bingo has. BIN traded dividend today for 2.2c FF

Bingo (BIN) Chart

BROKER MOVES

- BHP Raised to Overweight at JPMorgan

- BHP ADRs Cut to Hold at Argus

- Rio Tinto Raised to Buy at SocGen

- Telstra Raised to Buy at New Street Research; PT A$3.90

- Avita Medical ADRs Rated New Buy at BTIG; PT $10

- Regis Resources Raised to Neutral at JPMorgan; PT A$3.90

- Newcrest Raised to Neutral at JPMorgan; PT A$26

- Newcrest Raised to Buy at Shaw and Partners; PT A$30

- Goodman Group Cut to Sell at Goldman; PT A$12.91

- Fortescue Raised to Buy at Shaw and Partners; PT A$10

- Alumina Raised to Buy at Shaw and Partners; PT A$2.05

- Whitehaven Raised to Buy at Shaw and Partners; PT A$2.90

- IGO Raised to Buy at Shaw and Partners; PT A$5.90

- GrainCorp Raised to Buy at Bell Potter; PT A$9.10

- CBA Raised to Buy at Bell Potter; PT A$88.80

- Viva Energy REIT Raised to Buy at Goldman; PT A$2.92

Get regular market updates

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking the 'CONTACT' button bellow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

1 topic

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management