Sunset Strip > Trading Day Wrap From Blue Ocean 20170907

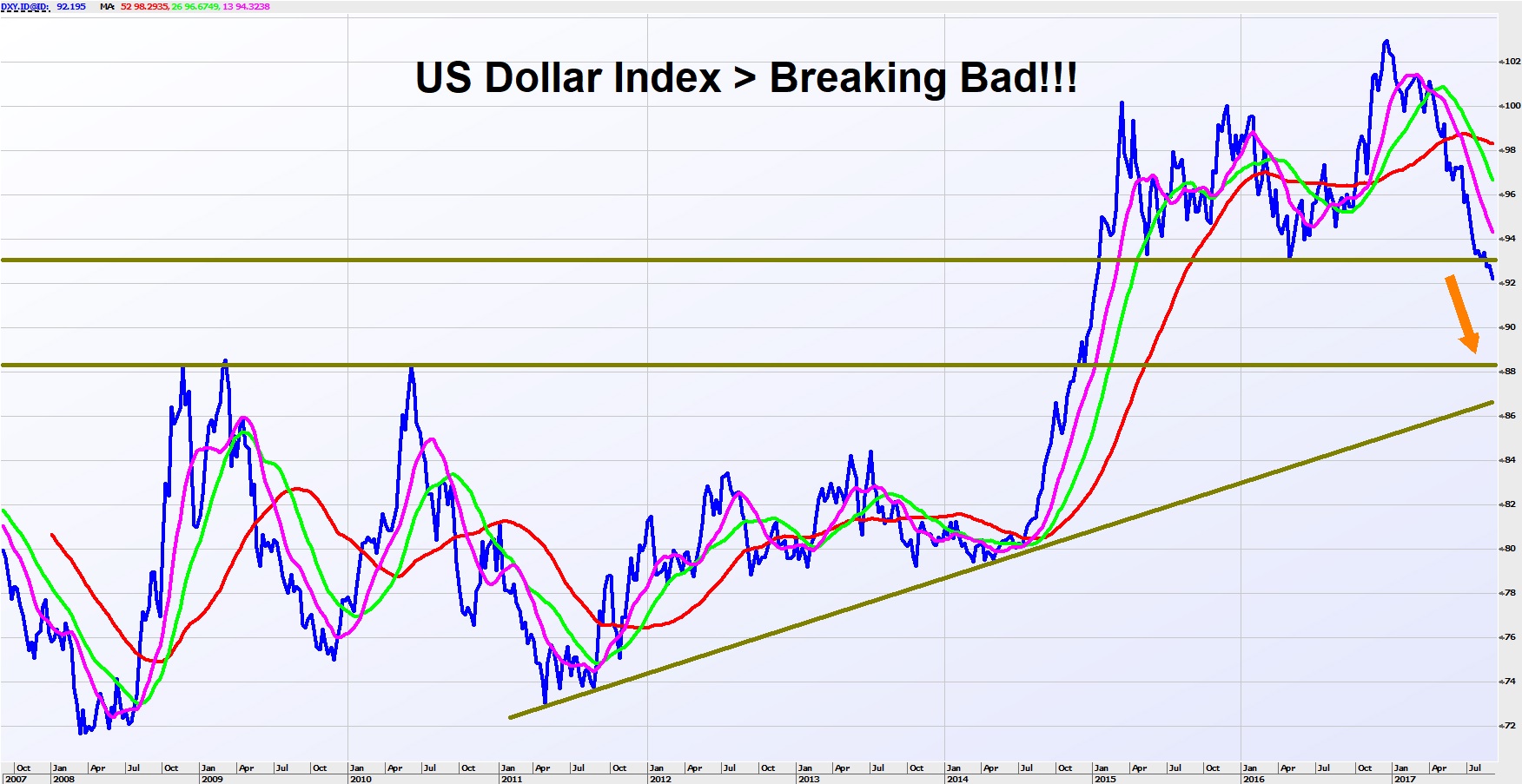

Local market jumped on the open with global bounce and then slid down to flat as overall negative sentiment took hold. Trump administration has kicked the can down the road by a short term debt ceiling deal for 3 months while the US Fed meeting in 2 weeks will be key to market sentiment as it deals with geopolitics, membership changes (i.e. Vice Chairman Stanley Fischer to resign next month) and patchy economic data. Canada has now raised rates in the past two BOC meetings and expected to raise again in the next month. Australia is very comparable with Canadian economy and their moves to curb property bubble and drive growth shows than Australia so far has missed the global recovery boat. RBA seem to be digging their heals in to stay put till something goes wrong or inflation shoots. The economy is facing tough outlook for consumers and that raises the risk that RBA has priced themselves out of the economic cycle while the high spending governments and over geared households are going to run out of puff. There are a few big caps going ex dividend today (i.e. BHP and WOW) and tomorrow and that will weigh on sentiment. We continue to be fans of the base metals and precious metals in the short term…we like RRL and DCN in Gold, MLX and MOD in Copper, WSA and IGO in Nickel, AWC on aluminium and S32 as the diversified outside BHP and RIO. AUDUSD back near 80 cents and looking to go higher as commodities hold up on positive China outlook. Weak retail and current account did not push down the AUD much…RBA caught between a bubble and slow growth. We continue to favour miners over financials and industrials for September. Stay nimble as September outlook remains weak for markets before the next leg higher. BOEQ Footy Finals picks…just for fun!!!

Click here for the full report.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and CEO at Deep Data Analytics (www.deepdataanalytics.com.au) which is an integrated data analytics driven investment strategy service provider.

6 topics

3 stocks mentioned

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Comments

Comments

Sign In or Join Free to comment