7 biases to tame for better returns

Joe Wiggins

Aberdeen Standard Investments

Behavioural economics moved into the mainstream when psychologist Daniel Kahneman was awarded the Nobel Prize for economics. Ironically, his work was critical of classical economics. He focused on how human behaviour differs from what economists would expect, from their theoretical viewpoint. (vii)

Kahneman is best known for identifying a range of cognitive biases in his work with the late Amos Tversky. These are our consistent deviations from rational behaviour.

For example, the ‘endowment effect’ is our tendency to value things more highly when we own them. A research study found that participants willing to buy a lottery ticket for $1.28 would only sell a ticket they already owned for $5.18.(viii) This is clearly not rational, economically consistent behaviour. The odds of winning are the same for both tickets. And why would we have an emotional attachment to a piece of paper?

But it also feels intuitively correct. Imagine you won tickets to the Wimbledon final. There is a good chance that your selling price for the tickets would be far higher than the price you would have been willing to pay. This example may seem trivial. Yet we find this behaviour across a range of different scenarios.

“We are all susceptible to a formidable array of decision biases. There are more of them than we realize and they come to visit us more often than we like to admit." (ix) Ariely & Jones, 2013

The number of cognitive biases identified has exploded. Wikipedia lists hundreds, from the ‘ambiguity effect’ to the ‘Zeigarnik effect’.(x) The growing awareness of our behavioural foibles is undoubtedly positive. However, the vast list of biases – real or perceived – can be unhelpful. We want to better understand our behaviour, but there is a danger that we become lost in a sea of biases.

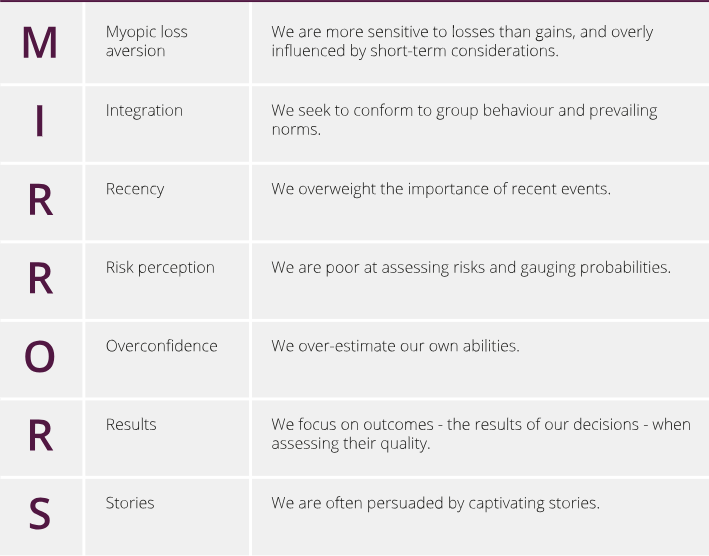

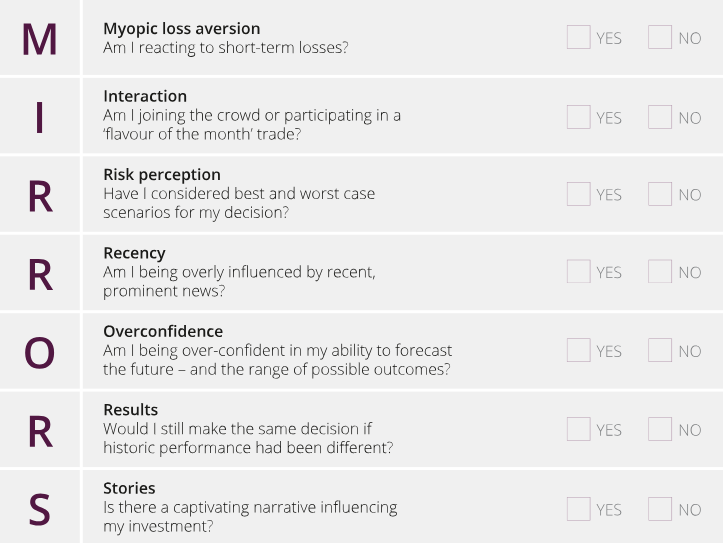

Investors should focus on those biases that are most likely to impact their investment decisions – and those supported by robust evidence. We have developed a checklist to reduce errors from the key behaviours that affect our investment decisions - ‘MIRRORS’. It provides key questions to ask yourself before making an investment decision.

MIRRORS: a checklist of our main behavioural biases

Atul Gawande is a US surgeon who developed a simple safe surgery checklist for the World Health Organisation. They applied it around the world with staggering success. In The Checklist Manifesto (xi), he explains how checklists encourage consistent behaviour in order to limit mistakes.

A checklist for investors cannot be as specific as in surgery, where questions such as: ‘Have you washed your hands?’ or ‘Are you operating on the correct leg?’ can be definitively answered. In investment, very few issues are as clear cut. However, we can ensure that we integrate the consideration of behavioural issues into our decision making.

The ‘MIRRORS’ checklist addresses the major impediments to effective investment decision-making; the behaviours that create the ‘behaviour gap’. These are the behaviours.

Myopic Loss Aversion – We are more sensitive to losses than gains and overly influenced by short-term considerations.

Myopic loss aversion is stimulated by focusing on short-term performance. We check our portfolios frequently, even if we have a long-term investment horizon. Investors who received the most frequent feedback took the least risk according to one study.(xii) And made the least money. Making frequent investment decisions worsens the decisions made.(xiii)

Technological developments have improved our ability to monitor our investments. But this increases the difficulty of sticking with the appropriate long-term investment strategy.

We often struggle to cope with short-term losses. This happens even if the losses are irrelevant in the context of our long-term goals. This can lead investors to take insufficient risk in their portfolios.

Loss aversion is the best-known finding from behavioural economics. Yet investors understate the importance role of reference points. We experience losses relative to a particular reference point – a starting level, value or benchmark. The choice of reference point changes how we think about investment performance – and the decisions we subsequently make.(xiv)

Reference points can vary between individuals, even with the same investment. How we compare our investments and set expectations can alter our decision making. We need to make comparisons when we assess performance. But it is crucial that these comparisons are sensible, relevant and applied consistently.

Integration – We seek to conform to group behaviour and prevailing norms.

Social proof is our propensity to base our decisions on the behaviour of others. This is one of the six principles of persuasion outlined by psychologist Robert Cialdini in his landmark work, Influence.(xv) There is no better setting to help us understand herd mentality than financial markets. Our desire to follow what others are doing is a strong driver of behaviour. The more we see other people doing something, the more we believe that it is the right thing to do.

Charles Mackay documented the damaging impact of crowd psychology in Extraordinary Popular Delusions and the Madness of Crowds, published in 1841. The lessons learned in studying events such as Tulipomania (1636 – 1637) and The South-Sea Bubble (1720) remain relevant today.(xvi) Our desire to conform plays a key role in fuelling financials bubbles and crashes. It is also a crucial element of successful financial frauds.

“Our desire to follow what others are doing is a strong driver of behaviour. It plays a key role in fuelling financials bubbles and crashes.”

Recency – We overweight the importance of recent events.

Recency bias is our inclination to focus on events that have occurred in the recent past – and overstate their importance in determining future outcomes.

As investors, we tend to assume that future performance will be a continuation of the recent trend. We feel positive about stock prices close to the market peak and reticent to invest at the bottom. Our decisions are swayed by the most recent news headline, even when making long-term decisions.

When asked what would be learnt from the Global Financial Crisis, veteran fund manager Jeremy Grantham observed: “We will learn an enormous amount in a very short time, quite a bit in the medium term and absolutely nothing in the long term”.(xvii)

Risk Perception – We are poor at assessing risks and gauging probabilities

We are poor at judging the risk of low-probability events. We overestimate the odds of winning the lottery(xviii). When betting on horse racing, the longshot is ‘overbet’ and the favourite is ‘underbet’ (xix). Yet we also disregard certain low-probability risks, such as failing to insure ourselves against catastrophes like floods and earthquakes.(xx)

We exhibit ‘probability neglect’. Our decisions are affected by how readily an example comes to mind. We let emotions override analysis when we assess the likelihood of an event (xxi).

This behaviour is evident after severe market declines. Investors become more risk averse, despite cheaper valuations improving expected long-term returns. The emotional toll of losses – and the recent experience of severe losses – overwhelms rational, long-term thinking. Similarly, strong markets lead investors to underestimate or ignore the probability of significant market losses.

Overconfidence – We overestimate our own abilities

Overconfidence is readily observed. The vast majority of individuals believe that they are an above average driver. Digging deeper, it has been argued that there are three distinct types of overconfidence.

- We overestimate our own performance level.

- We believe we are better than others.

- We believe we know the right answer.

Overconfidence can create costly problems for investors, such as insufficient portfolio diversification and overtrading. We make decisions based on forecasts of economic data, politics and markets despite the difficulty of predicting the future. Our confidence can tempt us into short-term trading, despite the challenges of anticipating the moves in volatile and often random markets. It is important to be humble in our investment decision making.

Results – We focus on final results and outcomes when assessing the quality of a decision.

Outcome bias is our propensity to judge a decision by its eventual result instead of the quality of the decision (xxii).

If I bet my life savings on a game of poker, you would think this was a poor decision, irrespective of the outcome. Yet the result alters our view. If I am financially ruined, it was a foolhardy decision. If I make my fortune, I may be lauded for my skills at the poker table.

This focus on results is problematic for investors because financial markets are inherently random (at least over short time periods). Astute decisions can lead to bad outcomes. Increasing allocations to equities after a period of weakness is likely to be a sensible decision. Valuations will be lower and therefore long-term expected returns higher, all other things being equal. Yet the most recent outcome means we tend to focus on the fact that they may continue to fall. This can make a sensible decision to increase equities appear unjustly imprudent.

Stories – We are persuaded by compelling stories:

Stories are fundamental to how we understand the world. This is true across cultures and generations. Compelling narratives are particularly important in areas of high complexity such as financial markets.

We use stories to try to explain and simplify the randomness of markets. They are also the hallmark of manias and panics. No investment bubble has occurred without the tailwind of a captivating story. Even professional investors rely on stories to make investment decisions (xxiii).

Even investors using computer-driven decision making to manage their portfolios are susceptible to the power of stories. Their models incorporate underlying assumptions about how markets work. They assume that the future will closely resemble the past. Investors need to realise that their models are a model, not the model.

Our susceptibility to narratives leaves us vulnerable to poor investment decisions. We are drawn to simple stories that allow us to make sense of highly complex issues. But this can draw us away from evidence-based decision making. Today’s headline reads “Stocks Rally in Europe and Asia Ahead of Trade Talks” (xxiv) but a more accurate description might be “Stocks Fluctuate due to Normal Random Movements”. These changing narratives lead investors to trade too frequently.

How to Use the Checklist

Using a checklist is no panacea. We cannot overcome our ingrained biases simply by ticking boxes. However, by asking ourselves some key questions before we make a decision, we can aim to reduce errors of judgement and deliver better investment outcomes.

Turning Down the Noise

Noise refers to the random variables that affect our decisions. Our judgements are guided by informal experience and general principles rather than by rigid rules. Where there is judgement, there is noise. Our choices are influenced by irrelevant factors. This leads to inconsistent judgements. Investors can reduce the effects of noise through the consistent application of simple rules.

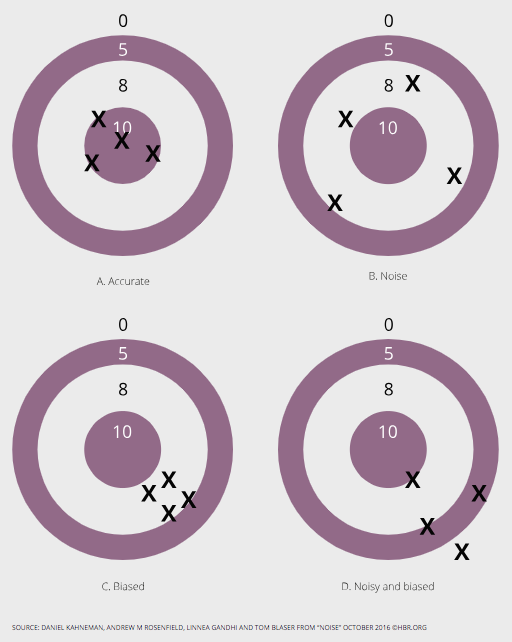

Daniel Kahneman is mostly associated with behavioural biases, but he has recently focused on a different phenomenon – ‘noise’. Our biases are our behaviours that are consistently sub-optimal - at least in direction, if not magnitude. By contrast, noise is defined by the absence of consistency. A watch that loses time each day is biased. A watch that can either gain or lose time during any given day is noisy. The image below illustrates the distinction.

How noise and bias affect accuracy

Our judgements are guided by informal experience and general principles rather than by rigid rules. This leads to inconsistent judgements. Kahneman cites the example of software developers asked to estimate the completion time for a given task. On two separate days, the hours they projected differed by 71%.

Individual choice is “strongly influenced by irrelevant factors”.xxv However, it is hard to identify, isolate and anticipate these irrelevant factors. (By contrast, our MIRRORS framework helps to define, understand and cope with some of our biases.)

Noise can stem from entirely spurious factors. We are influenced by variables that we perceive to be meaningful but are in fact meaningless. Notably, our decisions change with how we feel at the time of a decision.xxvi

In investment, we are often uncertain about the issues that are genuinely relevant to a decision. When making investment decisions, we can define two separate forms of noise:

- Unconscious noise. Irrelevant factors will influence our judgement. Given the same information, we are unlikely to make the same decision at a different time.

- Conscious noise. Information that we believe is relevant, but actually should have no bearing on our judgements, influences our decision making.

With unconscious noise, there are many factors that impact our decision making over which we have no awareness. Indeed, if asked, we might well be reticent to acknowledge that many had any influence over us (such as the fact that we were hungry at the time).

With conscious noise, the issue is uncertainty about what constitutes relevant information and what is noise. We are bombarded on a daily basis by information on companies and economies. Yet a tiny fraction of this information is relevant to our long-term investment strategy.

Noise is an inescapable feature of human judgement. In investment markets, where daily price moves are random and the future uncertain, its influence is profound. It is impossible to eradicate it. Instead, investors should acknowledge its presence.

Kahneman sums it up. “Where there is judgement, there is noise – and usually more of it than you think.”

What steps can investors take to counteract noise? A more systematic approach to decision making can reduce its influence. And this does not have to mean handing over the decision making to a computer algorithm. Human judgement can be a useful input. The key is to adopt procedures that promote consistent decision making. Algorithms do a better the role of final decision maker in many situations. “Unlike humans, a formula will always return the same output for any given input.”

Nor does a process have to be complicated. “You can reap most of the benefits by using common sense to select variables and the simplest possible rules to combine them.”

The consistent application of simple rules is an effective way of mitigating the negative impact of noise.

This is part two of a three-part series. Read part one here.

Never miss an update

Stay up to date with the latest content from Aberdeen Standard Investments, including the final installment of our deep dive on behavioural finance, by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Aberdeen Standard? Hit the 'contact' button to get in touch with us or visit our website for more information.

_________________________________________________________________

(xii) Thaler, R. H., Tversky, A., Kahneman, D., & Schwartz, A. (1997). The effect of myopia and loss aversion on risk taking: An experimental test. The Quarterly Journal of Economics, 112(2), 647-661.

(xiii) Hardin, A. M., & Looney, C. A. (2012). Myopic loss aversion: Demystifying the key factors influencing decision problem framing. Organizational Behavior and Human Decision Processes, 117(2), 311-331.

(xiv) Tversky, A., & Kahneman, D. (1991). Loss aversion in riskless choice: A reference-dependent model. The quarterly journal of economics, 106(4), 1039-1061.

(xv) Cialdini, R. B. (1987). Influence (Vol. 3). Port Harcourt: A. Michel.

(xvi) Mackay, C. (1869). Memoirs of extraordinary popular delusions and the madness of crowds. George Routledge and Sons.

(xvii) Jeremy Grantham (2008), Interview, Barron’s magazine.

(xviii) Clotfelter, C. T., & Cook, P. J. (1990). On the economics of state lotteries. Journal of Economic Perspectives, 4(4), 105-119.

(xix) Snowberg, E., & Wolfers, J. (2010). Explaining the favorite–long shot bias: Is it risk-love or misperceptions? Journal of Political Economy, 118(4), 723-746.

(xx) Camerer, C. F., & Kunreuther, H. (1989). Decision processes for low probability events: Policy implications. Journal of Policy Analysis and Management, 8(4), 565-592.

(xxi) Sunstein, C. R. (2002). Probability neglect: Emotions, worst cases, and law. The Yale Law Journal, 112(1), 61-107. “When strong emotions are triggered by a risk, people show a remarkable tendency to neglect a small probability that the risk will actually come to fruition. Experimental evidence, involving electric shocks and arsenic, supports this claim, as does real-world evidence, involving responses to abandoned hazardous waste dumps, the pesticide Alar, and anthrax.”

(xxvii) Baron, J., & Hershey, J. C. (1988). Outcome bias in decision evaluation. Journal of personality and social psychology, 54(4), 569.

(xxviii) Tuckett, D. (2011). Minding the markets: An emotional finance view of financial instability. Springer.

(xxiv) Bloomberg headline, 4/1/2019.

(xxv) Kahneman, D., Rosenfield, A. M., Gandhi, L., & Blaser, T. (2016). NOISE: How to overcome the high, hidden cost of inconsistent decision making. Harvard business review, 94(10), 38-46.

(xxvi) Loewenstein, G., & Lerner, J. S. (2003). The role of affect in decision making. Handbook of affective science, 619(642), 3.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

2 topics

1 contributor mentioned

Joe Wiggins

Senior Investment Manager

Aberdeen Standard Investments

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

Expertise

Joe Wiggins

Senior Investment Manager

Aberdeen Standard Investments

Joe is responsible for fund research and the management of multi-asset portfolios. He joined Standard Life in 2011 from Stamford Associates where he was an Investment Analyst, and prior to this he worked for Principal Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment