The art and science of Late Cycle Investing

Investing late in the cycle of a bull market poses particular challenges for investors and requires a disciplined approach to risk and liquidity to be successful.

Timing a peak is very difficult, even for professionals. However, we know that global economic growth is slowing. The US economy is decelerating and China is softening due to monetary tightening and the trade dispute. The US Fed has turned less hawkish, perhaps signaling rate rises are near the end or even finished.

In Australia, the February NAB Business conditions survey was very weak. The housing market is falling and credit growth is drying up due to the Banking Royal Commission’s focus on responsible lending and a drop in consumer confidence. Like the Fed, the RBA is now less likely to raise rates, reflecting the deterioration in the domestic economy. After a significant correction in global stock markets in Q4 last year, markets have rebounded and valuations are stretched.

A framework for managing risk

No one can predict the future, thus the backbone of any individual’s portfolio should be a well-diversified long-term strategic asset allocation (SAA). The SAA is the average allocation to the different asset classes an investor should have through a cycle that reflects the risk the investor is willing to take. Choosing the correct SAA minimises the risk an investor will panic in down markets and sell just at the wrong time. That is because the volatility is within expectations. The SAA will be a mix of bonds, equities, hedge funds and commodities. The bonds and to some extent hedge funds and certain commodities act to preserve capital in weak markets.

Tactical strategies to reduce risk

As we approach what seems to be a risky period for growth assets, it makes sense to make some shorter term tactical investments to reduce the impact of a downturn. In doing so, investors must remain true to the broad thrust of their SAA.

Reducing the allocation to shares and holding cash is a valid strategy, but cash won’t hedge against falls in stock markets. In contrast, increasing the allocation to Australian government and high grade bonds is a simple way to reduce risk and build exposure to an asset class that typically appreciates in value when stock markets are falling. With the Fed and RBA putting rates on hold, the risk of higher yields appears low.

Emerging market bonds offer a more attractive yield, but tend to have a higher correlation with share markets as they are perceived to be riskier. However, fund vehicles are available that provide downside protection against this scenario in exchange for a slightly reduced yield.

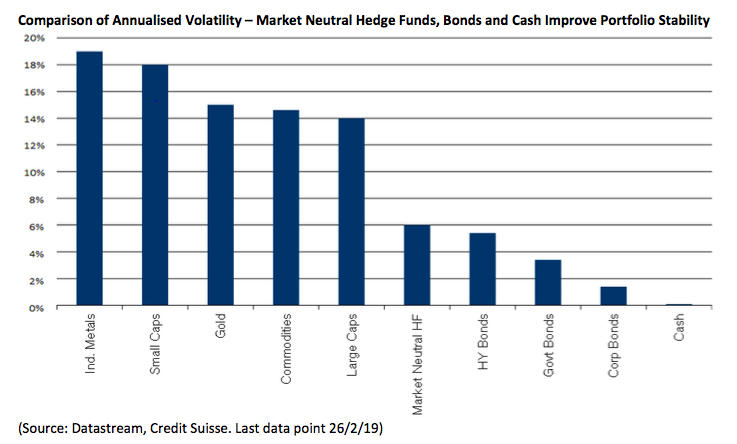

Increasing hedge fund allocations at the expense of equities is also a useful strategy late in the cycle. It is important to find the right hedge fund - one that has an absolute return objective and an investment approach that is uncorrelated with the direction of share markets. For example, a special situation strategy, which takes advantage of takeovers or distressed debt situations doesn’t rely on the direction of share prices. Likewise, a market neutral fund, where the return is determined by its longs outperforming its shorts, as opposed to markets appreciating in general, improves the stability of the overall portfolio.

Defensive sectors

Changes can also be implemented within asset classes to counter the risk of a downturn. For example, within Australian equities our portfolios are underweight domestically exposed stocks such as those in consumer retail, banking and building/residential property. We have skewed our portfolio towards foreign currency earners such as the miners, healthcare and specific situations where the prospects are brighter or earnings more defensible. The big miners also have the ability to declare special dividends due to their strong cash flow and large franking credit balances.

Consideration can also be given to infrastructure, low regulation utilities and industrial and office real estate trusts that provide a lower risk dividend stream. Consumer staples stock earnings are also resilient regardless of economic growth. Exposure to small capitalisation stocks can be reduced, as they often underperform in slowdowns. At the sector level, they have an outsized exposure to the domestic economy less ability to weather a storm and it is more difficult for them to access capital.

Safe havens and option strategies

The experience of the Global Financial Crisis (GFC) has taught us that when systemic risk is at an extreme, almost all asset classes are sold off. Even so, there are some investments that are given “safe haven” status such as US Government Treasuries. For Australian investors, buying unhedged US Treasuries is a useful strategy, given the AUD tends to depreciate in risk off periods. During 2008, long duration US Treasuries returned over 50% in AUD.

Gold also does well in times of extreme stress. Although it doesn’t pay a dividend, and has limited industrial use, its rarity and acceptance as a store of wealth gives it a value unrelated to stock market movements. Finally, the Yen can be a good hedge against risk depending on where it is trading. Japan is the largest net creditor to the world. When growth fears rise, the Japanese habitually repatriate their capital, which strengthens the JPY. But we would note predicting currency moves is very difficult.

Finally, options can be used to hedge risk or lock in returns. The simplest strategy, but also usually the most expensive, is to buy puts on an index such as the S&P500. Having the ability to sell a market at a lower price is insurance, but is quite a bearish stance given the premium that has to be paid for the insurance.

Conclusion

Investing late in the cycle is about reducing portfolio risks as the expansionary cycle slows and we near the market’s peak. Risk can be reduced in a number of ways, but whatever method is chosen, the integrity of the overall long run strategic asset allocation must be kept intact.

I discuss more on how to set up portfolios to survive the late-cycle in this video

Never miss an update

Stay up to date with the latest news from Credit Suisse Private Banking by hitting the 'follow' button below and you'll be notified every time I post a wire. Want to learn more about Credit Suisse Private Banking? Hit the 'contact' button to get in touch with us.

Credit Suisse Private Banking specialises in asset diversification, holistic wealth planning, next generation training, succession planning, trust and estate advisory, philanthropy. Find out more here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

1 topic

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment