The Case for Owning Quality Stocks Now

It is no secret that investing in high quality stocks for the long term is a good investment strategy. Russell Investments believes that a premium for high quality stocks exists, in that they will outperform low quality stocks over the long term. We believe that this anomaly exists as investors tend be focussed on more volatile stocks in the short term with higher upside potential, leading to high quality stocks being mispriced. Furthermore, high quality companies tend to outperform in periods of market stress and downturns, which can have a material impact on long term performance.

Quality stocks tend to exhibit a combination of characteristics, but key features are generally high profitability (typically measured by Return on Equity, “ROE”), low leverage, low earnings variability, high interest and dividend coverage, as well as robust business models. ROE is frequently used as a general proxy for exposure to quality. The Australian Health Care sector has been and remains a source of high quality companies, Cochlear and CSL being two notable examples. Outside of this sector, finding high quality stocks tends to be more idiosyncratic and there can be a degree of cyclicality around which companies are high quality at different points in time. For example, Fortescue Metals currently scores well on quality metrics, but this has not always been the case. Over the past two years the company has increased its ROE from below 5% to over 20%, whilst reducing leverage from approximately 130% debt/equity to 46% as of June 2017 (Source: FactSet). Caltex is another example of a company that is currently attractive from a quality lens due its strong relative ROE and low debt profile.

Source: Russell Investments, UBS

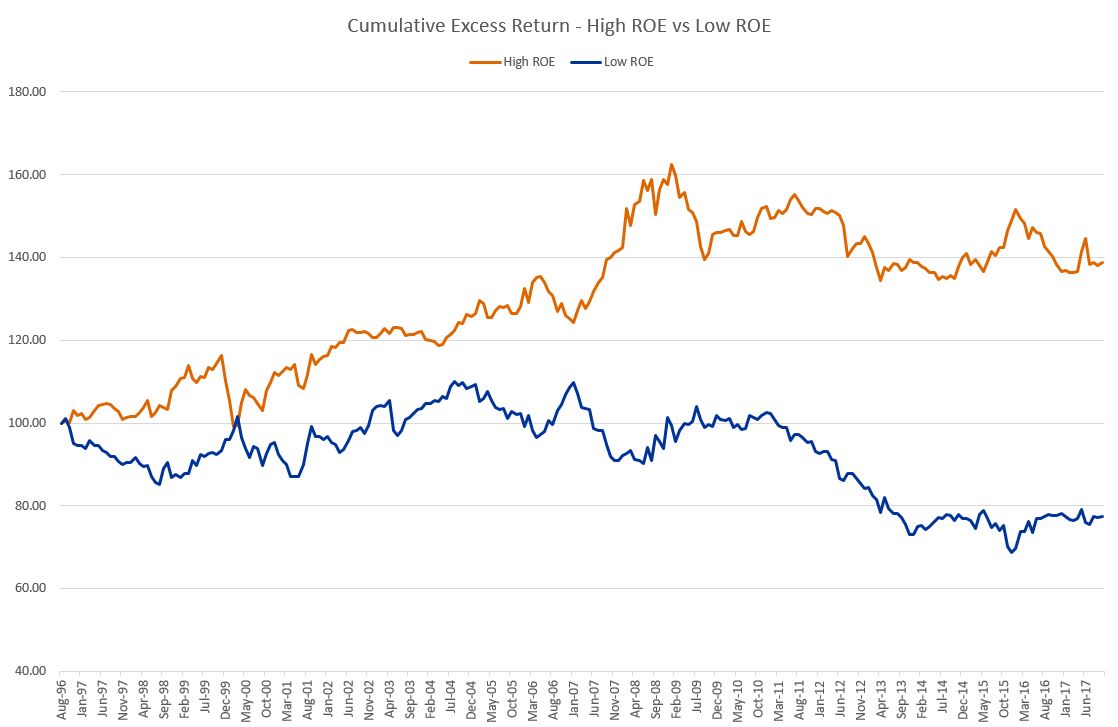

Due to our belief in the quality premium, our equity funds generally favour exposures to high quality stocks over the long term in order to benefit from the associated excess return potential. As with all market segments, performance is cyclical and there are times when quality stocks will be out of favour. It is therefore important to dynamically manage exposures to different factors through time, and we do this by looking at metrics across three categories - cycle, valuation, and sentiment. As seen in the following chart, quality (using ROE as a proxy) has been through a period of relative weakness since the beginning of 2016, when high beta cyclicals began to rally.

Source: Russell Investments, UBS

Cycle

We gauge where we are in the business cycle by looking at earnings, economic, and policy signals. These signals are currently modestly positive on quality. This view is driven by a relatively benign outlook on earnings over the next twelve months, alongside an expectation of rising interest rates in Australia through 2018.

Valuation

High quality stocks are currently attractive on a valuation basis, on both earnings and asset based measures relative to history. Comparing valuation measures relative to history is important when it comes to high quality stocks, as many of the stocks tend to trade at a premium to the market multiple through time; comparing valuations to history allows us to take this premium into account.

Sentiment

Sentiment signals are more technical in nature, and look at how the market’s behaviour can help us make informed timing decisions of when to enter and exit (or increase and decrease) positions. We currently see sentiment on high quality stocks as strongly positive. After what has been a relatively weak period for quality stocks in aggregate, recent performance has begun to turn around and exhibit positive momentum. Supporting the positive sentiment on high quality stocks is the breadth of recent performance across multiple quality stocks.

The underperformance of high quality stocks over the past two years has presented an attractive buying opportunity and this is supported by our cycle, valuation, and sentiment signals. We believe that now is the right time to be buying quality stocks, and we have been increasing our exposure across our Australian equity funds.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew Zenonos is a Portfolio Manager at Russell Investments focussing on Australasian equities and responsible for all aspects of portfolio management. He is also a member of the Global Equity SME team, and is a CFA charterholder.

4 stocks mentioned

Andrew Zenonos is a Portfolio Manager at Russell Investments focussing on Australasian equities and responsible for all aspects of portfolio management. He is also a member of the Global Equity SME team, and is a CFA charterholder.

Expertise

Andrew Zenonos is a Portfolio Manager at Russell Investments focussing on Australasian equities and responsible for all aspects of portfolio management. He is also a member of the Global Equity SME team, and is a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment