The characteristics of a long term winner

When we think about growth versus value, and this is very topical now because growth stocks are doing well, I think it's important to recognise that this has actually been happening for quite some time. And a lot of the trends we're seeing here have been happening for a long time, they're just accelerating in a post-COVID world. The standard accusation as to why growth investing is doing well is that interest rates have fallen from say 20% to 1%. And in a post-COVID world, interest rates have gone lower, so growth stocks are going higher.

I think that is definitely part of what's going on, but I think it also misses the point because from our point of view, Jeff Bezos set up a bookstore in his garage 20 years ago, and it's now worth $1.6 trillion. That only happened because interest rates went from 20% to 1%. Reed Hastings set up a DVD delivery service in California and turned it into Netflix. That only happened because interest rates went from 20% to 1%. Even here in Australia, Mike Cannon-Brookes and Scott Farquhar put software online at the University of New South Wales and turned into Atlassian, which is now worth roughly $50 billion.

So it's clear that there's actually something else going on here apart from interest rates falling, and that is clearly the acceleration in compute power. Like every generation before us, we are living through a revolution. Others have been through the transport revolution, the oil and gas revolution, the rail revolution, the retail revolution. We are living through the digital revolution.

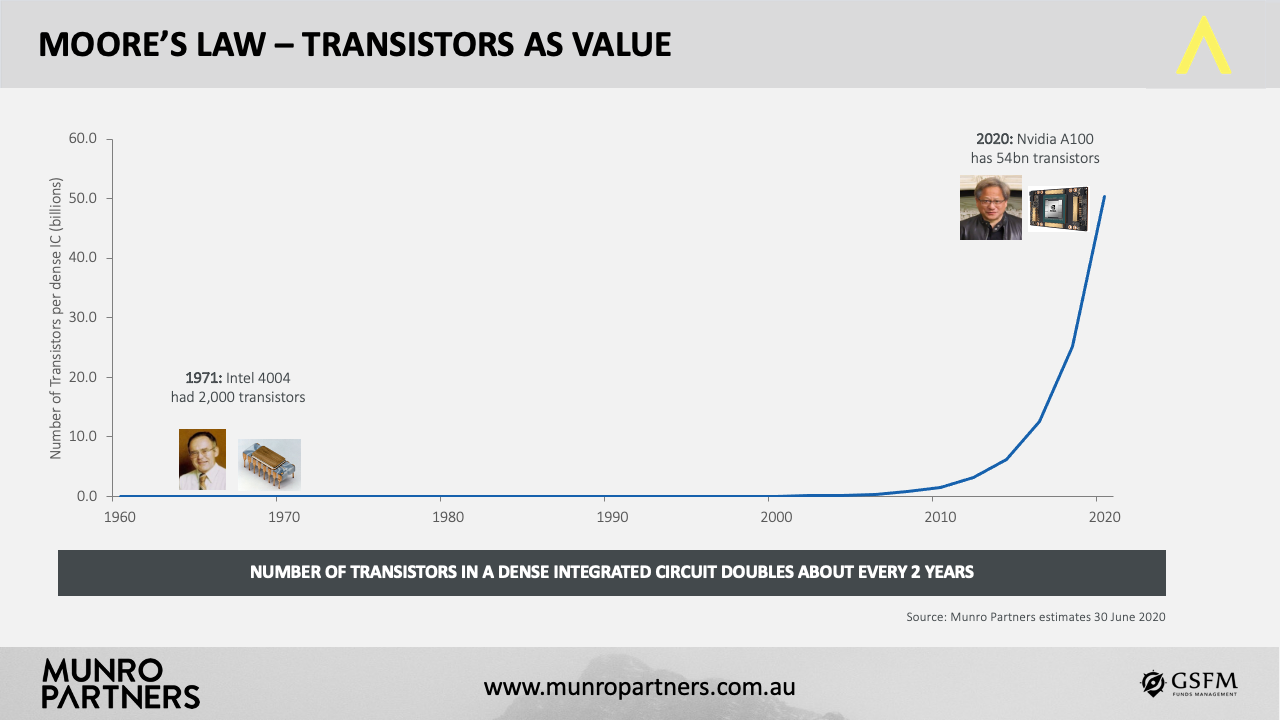

This digital revolution is being driven by Moore's law, and when we talk about Moore's law, we talk about computers becoming more powerful, and as they become more powerful, they grow their compute power exponentially.

Put simply, in 1971, Intel's first semiconductor chip had 2,000 transistors on it, but every two years, it doubled the transistors and halved the price, and now here in 2020, Jensen Huang's new transistor at Nvidia has 54 billion transistors on it. Computers are getting faster.

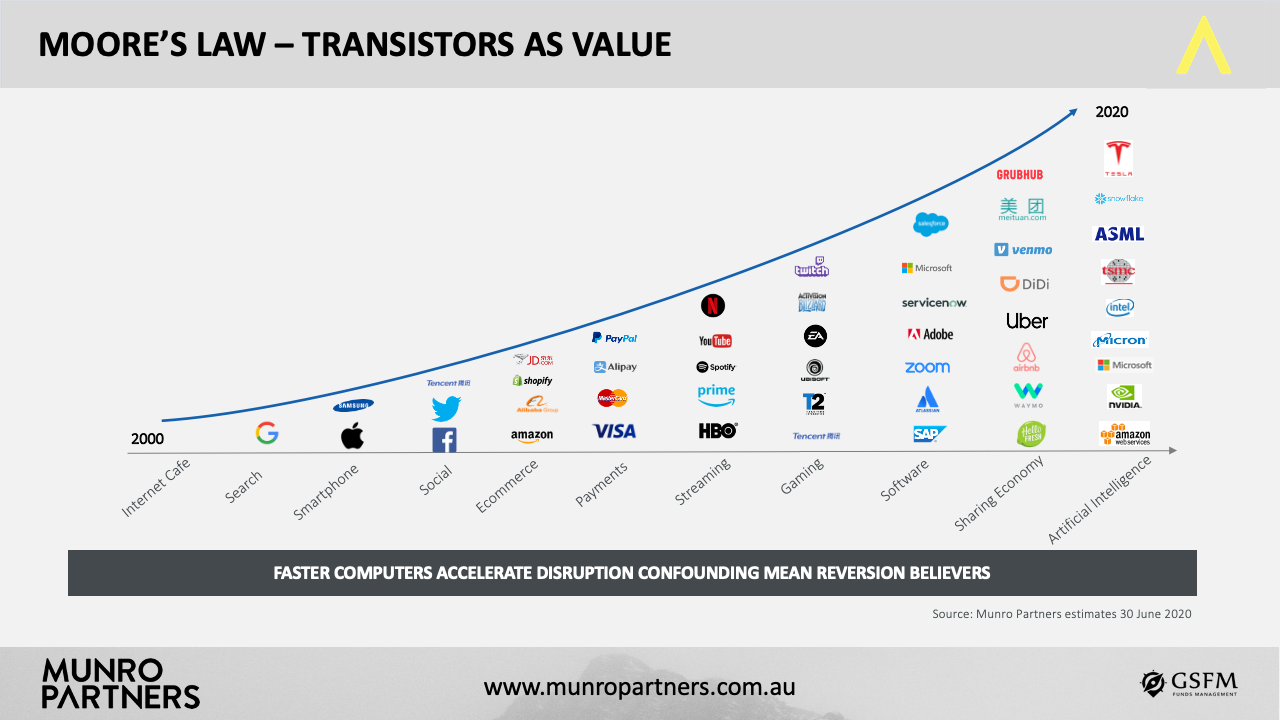

Now most people will see this all around them, just purely by looking at the speed of the Internet or what the Internet's done in the last 20 years.

You've gone from a point where we used to be able to send an email, to then being able to do search, be on your telephone, stream movies, and then now even in this crisis, we're seeing how software is so important in our lives and internet enables software, be it video conferencing from Zoom etc. And so ultimately, as computers get faster, disruption accelerates, creating more and more of these wonderful winners. And these companies disruption accelerates and so for the people who are looking for mean reversion, this continues to confound them.

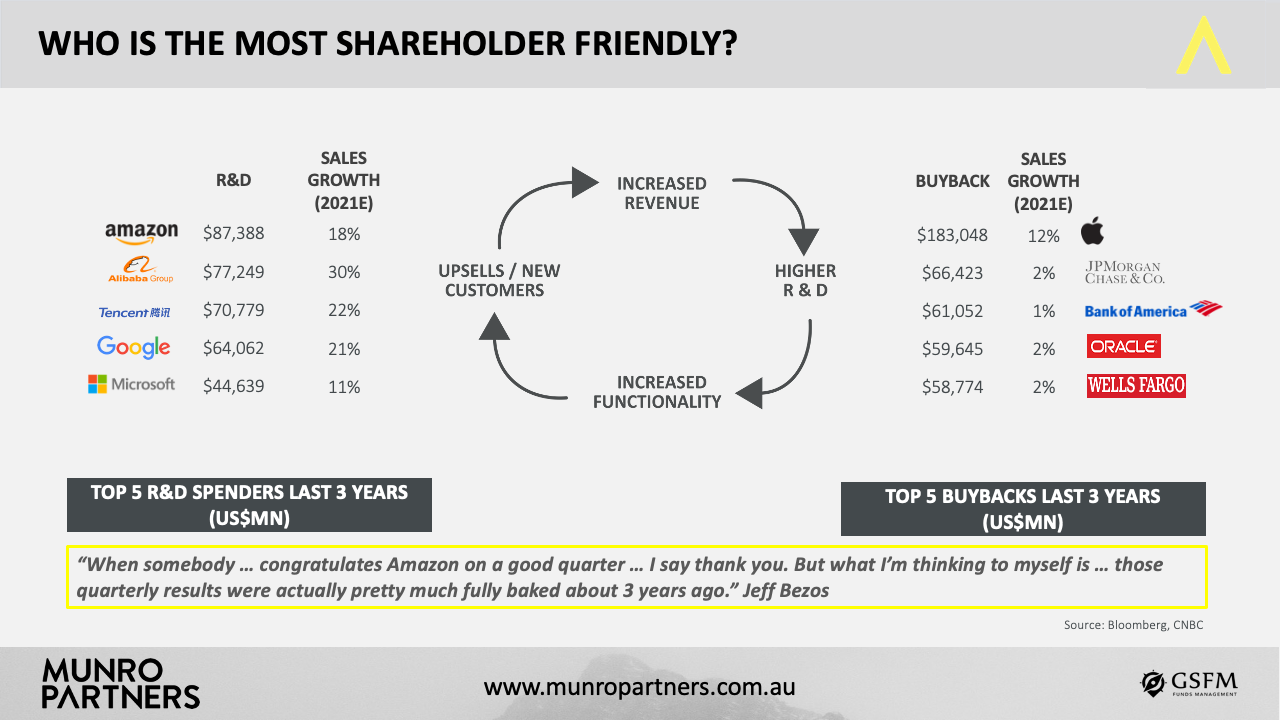

If we extend this conversation on, and we look at just what's happened in the last 10 years at the big platform companies that have won, it's reasonably obvious to us that they are exploiting this relationship. They are spending heavily on R&D to effectively grow what their business can do digitally in order to grow their sales. And they're being rewarded for it from their shareholders.

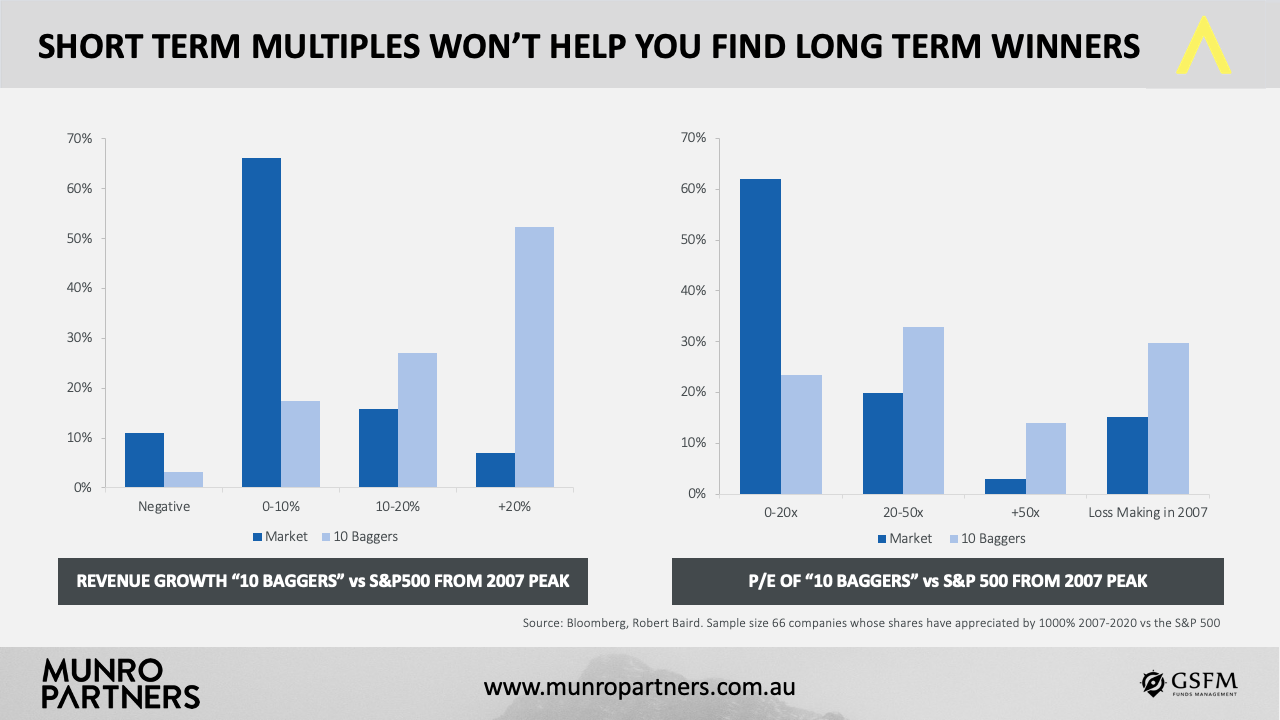

What's interesting against this is the so-called value companies that aren't spending on their business and doing so-called shareholder friendly actions are actually not being rewarded by shareholders because ultimately they don't have sales growth. If you follow this equation through, what's becoming very, very clear to us, is over the last 10 years if we look at the companies that actually went up 10 times in value from 2007 to 2020, all of them have the sales growth characteristics. All of them have this ability to grow sales at more than 10%.

So I think the market is quite correctly rewarding companies for investing in their business and being able to grow because they are going to be one of the few winners. This is a game of very few winners and lots of losers, and it gets worse in a digital world. As we look ahead, we think it's inconceivable that you should be able to look at short-term multiples to drive long-term performance. It doesn't actually make sense.

From our point of view, it's not really a growth versus value argument. It's quite simply, you have looked at next year's multiple and decided a company is expensive. And we don't see it that way. We think it's cheap because we're looking at what happens over the next 10 years. That's what's worked well for us for a period of time. We know why it's working well for us. And we think in a post-COVID world, it's going to become more important. So from that point of view, whether you choose us as a growth investor or somebody else, we don't really mind, but you're going to need a growth investor if you're going to deal with the next 10 years ahead.

Want to learn more?

Munro focuses on identifying and investing in companies that have the potential to grow at a faster rate and on a more sustainable basis than the peer group. Stay up to date with all my latest insights by clicking the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has over 20 years of financial services experience and over 14 years managing absolute return mandates focused on global growth equities.

........

The material contained in this publication is being furnished for general information purposes only as is not investment advice of any nature. The information contained in this document reflects, as of the date of publication, the views of Munro Partners and sources believed by Munro Partners to be reliable. There can be no guarantee that any projection, forecast or opinion in these materials will be realised. The views expressed in this document may change at any time subsequent to the date of issue.

This information has been prepared without taking account of the objectives, financial situation or needs of individuals. Before making an investment decision, investors should consider the appropriateness of this information, having regard to their own objectives, financial situation and needs.

Past performance information given in this document is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance. No representation or warranty is made concerning the accuracy of any data contained in this document.

3 topics

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Comments

Comments

Sign In or Join Free to comment