The danger in expensive defensives

Charlie Aitken

Aitken Investment Management

After a short period of relative calm, it appears rising global bond yields, led by US Treasuries, are going to again prove a headwind to certain “defensive” parts of equity markets.

While some bond fund managers get annoyed about equity fund managers writing on bonds, the simple fact is the direction of the “risk-free rate”, and the rate of change of the risk-free rate is crucial to overall equity market pricing and stock and sector selection. The very first thing I look at when I wake up is the “risk free rate”, also known as a US 10yr Bond. This is particularly so right now.

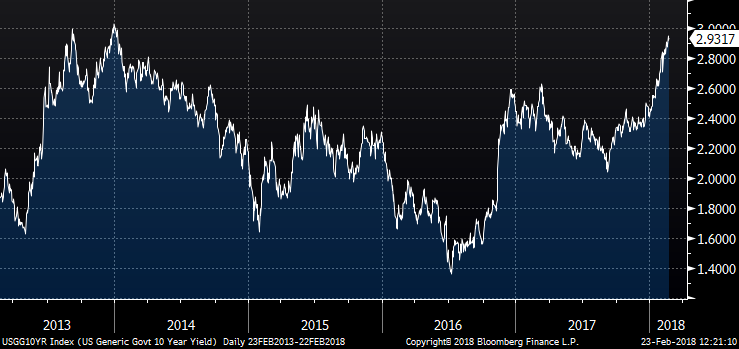

US 10YR BOND YIELD

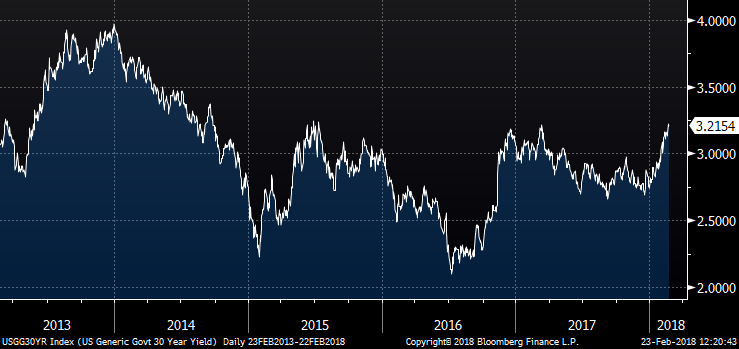

US 30YR BOND YIELD

The rise in bond yields and associated rise in volatility was what triggered the early February correction in equity markets. We need to be aware that US bond yields have made new highs and have taken out technical resistance. The new highs in bond yields are an important development with clear ramifications for equities, particularly in sectors where there has been a “search for yield” from those who had been squeezed out of low returning fixed interest assets by central banks. That reverses now as bond yields head higher.

I have been warning on long bonds and bond-like equities for 12 months. We believe long bonds and bond-like equities are real return free capital risk. The cost of shorting is very low at the annual yield of the bond or bond-like equity. My AIM Global High Conviction Fund is physically short long bonds and bond-like equities. I believe we are going from Central Bank quantitative easing (QE) to Central Bank quantitative tightening (QT). At the same time, the US has lost all fiscal discipline under Trump and will now run huge budget deficits that require record issuance of US Treasuries. The world, led by so-called bond vigilantes, is going to charge the US a higher interest rate to fund its deficits.

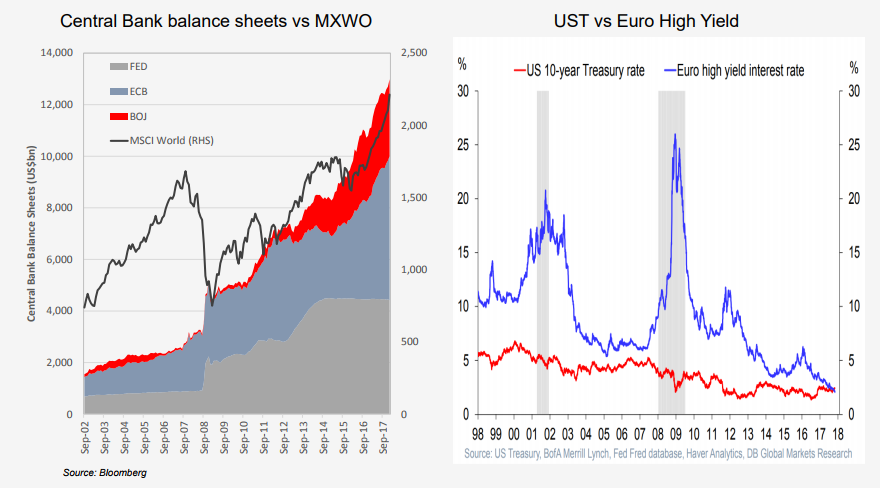

After a decade of QE, Central Bank action will turn negative in 2018:

- Fed balance sheet redemptions will increase, and ECB purchases will cease

- At the same time, increased fiscal deficits will see “issuance” increase

- The combined impact is a ~$500bn step up in supply of USTs

Similarly the size of cumulative central bank balance sheets has been highly correlated to asset prices.

If AIM is right and central bank balance sheets have peaked, and the risk-free rate is rising, then we are almost certainly past the end of the ultra-low volatility period in risk assets.

You must now condition yourself for a rise in volatility. You are going to see equity index moves driven by bond market pricing. You are also going to see a rotation away from perceived defensive equities, or equities with bond-like characteristics and durations.

I say again, just because a company operates in a defensive sector doesn’t mean its share price will prove defensive. I am of the view some of the largest potential capital losses over the next few years lie in perceived defensive sectors. As bond yields rise the price paid for defensive equities will fall, led by infrastructure, healthcare, utility, telco, supermarket and REIT sectors.

Yes, many of the current distribution yields in these sectors are attractive. But that won’t stop a P/E de-rating as bond yields rise. That P/E de-rating will equate to capital losses.

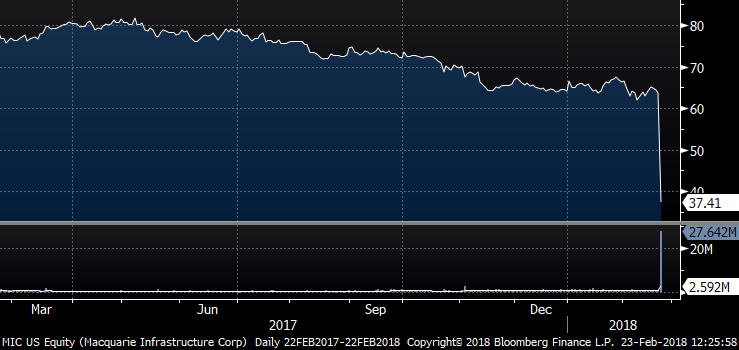

A classic example occurred last night when the $4b market cap Macquarie Infrastructure Corp (MIC.US) cut its dividend and fell a cool -41%, yes -41% in day. That’s not “defensive”.

Macquarie Infrastructure Corp: hits a speedbump

In Australia, the three large-cap defensive stocks I am most cautious on are Transurban (TCL), Sydney Airport (SYD), and Ramsay Healthcare (RHC). I realise these 3 market darling stocks have plenty of cheerleaders who think every dip is a buying opportunity, but this time I believe they will be proven wrong. This time rising bond yields will over-ride any stock specific story, and I think all three are at risk of -15% to -20% capital losses while still paying their dividends.

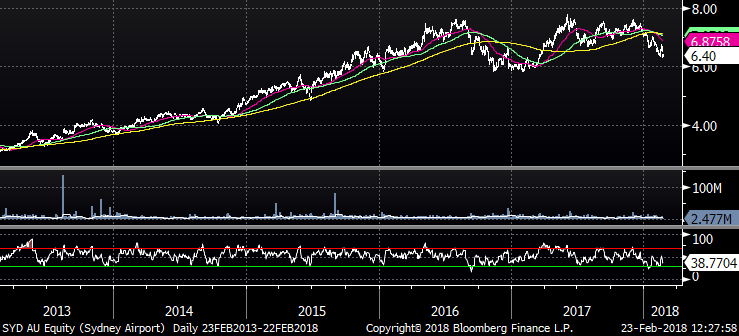

Sydney Airport (SYD) reported earnings yesterday and didn’t meet analyst expectations. SYD has a great narrative about rising international tourism numbers, but in my view is overvalued and likely to be de-rated in the months ahead.

Coming into the result yesterday there were 9 buys, 3 holds and 0 sells on SYD. The median 12-month price target was $7.33. However, SYD has broken down through the 200-day moving average, and I would argue that the 5-year uptrend is over.

SYD 5-year uptrend broken

As also happens regularly in corporate Australia, a long-serving very well regarded CEO recently stood down at SYD, just as things start to get a little tougher.

I would argue that SYD has squeezed every revenue dollar out of the Sydney Airport asset and incremental revenue growth from here will require larger capital expenditure.

Interestingly, for the third year in a row, the SYD capex budget appears to have increased. According to Macquarie Research last year SYD extended the 5 year spend and this year it has kept the spend rate constant, but now over four years (2018-21). Restating, SYD will spend $1.8b over FY16-FY20, $.5b more than the agreed envelope, and committed to another $.4b in FY21. There is always a risk that not all of the spend will be recovered.

The second issue is the capex spend rate is not falling. Much of the spending is for the growth in peak periods, i.e., 40% of traffic. As traffic growth stays strong, the airport gets increasingly complex and constrained, and MQG sees capex spend shifting to $.3b to $.35b up from $.25b historical average.

Don’t get me wrong, SYD is a true monopoly business, Australia’s gateway airport but the asset has been squeezed very hard, and capex is increasing to increase revenue. It will have a competitor of sorts in 2026 in the Western Sydney Airport, but right now that doesn’t concern me.

On a 2018 P/E of 36x offering +7.8% EPS growth and a 5.8% distribution yield (100% payout), it’s just too expensive for me. EV/EBITA of 18.3x as interest rates turn up. Net debt of $8.7b is also increasing over the forecast period.

SYD is a classic example of a defensive asset that isn’t proving defensive in share price terms. Yes, the distribution yield of 5.8% will be paid in 2018, but the stock just lost that in capital falls in two days since reporting . This is the risk in ALL BOND LIKE EQUITIES: your capital loss could be multiples of your annual dividend yield as the interest rate cycle turns up.

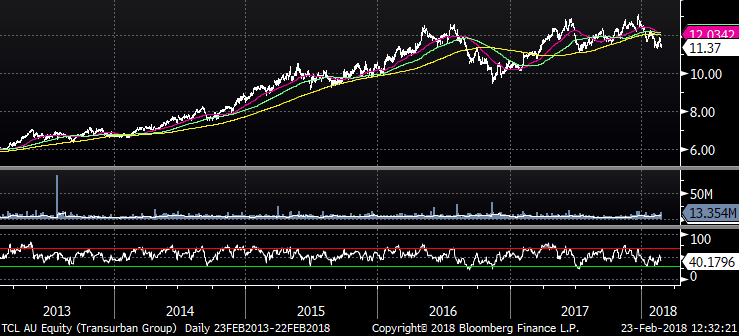

I think SYD will head below $6.00. Those of you who took up the recent TCL $2.5b rights issue at $11.40 should consider selling them while they’re still fractionally in the money. Trading on 52x earnings the scope for de-rating is real in TCL. For the next three years TCL’s distribution is not covered by free cashflow. Currently, there are 9 buys, 3 holds and 0 sells on TCL with a consensus price target of $12.72. I see TCL heading below $10.00 in the years ahead.

TCL 5-year uptrend broken

AIM’s cautious views on SYD, TCL, and RHC are not consensus, but they will be once investors and analysts realise the 30-year bull market in bonds is over. Defensive sector doesn’t mean defensive share price at the turning point of the interest rate cycle. This is particularly so after a decade of interest rate compression by central banks.

MIC.US’s -41% share price fall overnight is a warning signal for all listed infrastructure stock investors of the capital risk you are taking for picking up distributions paid from even partly from debt.

For more information on Aitken Investment Management please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire