The end finally appears near for NABHA holders

After 21 years, long suffering NABHA holders can finally see the end of their bumpy journey. Whilst NABHA holders have received what was required from their contractual position, getting quarterly payments through market ups and downs, they have long felt the sting of giving away a call option too cheaply. NABHA holders have constantly had to deal with the dilemma of selling at a capital loss to reinvest in better alternatives, or sticking with their hybrids not knowing when, if ever, they would be repaid. The announcement by NAB this week that they will ask shareholders for approval to redeem NABHA securities during 2021 looks to be the beginning of the end.

The history of NABHA highlights two common misunderstandings amongst hybrid buyers. NABHA and recent missed calls on European hybrids are a reminder that when you give a borrower an option on when to repay, it’s not unusual for the borrower to repay when it best suits them. NAB could have paid back their hybrids sixteen years ago, but the dividend rate was so low they were incentivised not to. It’s not only a borrower decision, in some cases the prudential regulator might strongly encourage or force a financial institution to leave their hybrids outstanding or switch off their dividends. Hybrid holders need to remember they are not in control of their repayment, in the case of NABHA it has taken a change of regulatory treatment to incentivise NAB to redeem these notes.

Another misunderstanding is that the liquidity provided by buying ASX listed hybrids means holders always have an easy exit option. It is correct that transacting listed hybrids is easy, but the capital loss incurred could be very painful. During the peak of the Financial Crisis, NABHA notes traded below $60. During 2016 they spent most of the year trading below $70. All this time NABHA holders were receiving a measly bank bills + 1.25%, typically less than term deposits. Similar risk securities were often paying 3-5% higher yields than NABHA. Small NABHA holders could have sold out quickly, but always at a substantial loss since 2009.

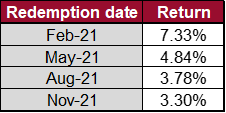

This brings us to where NABHA sits today at just above $98. Holders have the option to sell out and lock in a known price and timing for capital return or stay in the security to squeeze the last $2 of capital appreciation out. If you stay there’s a high probability you do get that last $2 in 2021 but a low probability market conditions change and NAB decides to keep NABHA as is, retaining it as long term funding until market conditions improve. There is a higher cost to NAB for this from 2022, but it could become a feasible option in a difficult economic environment. Based on the current price and various quarterly payment dates during 2021, here’s the potential returns.

It is obvious that when the repayment occurs makes a substantial difference in determining whether to hold or sell. If you are confident the repayment occurs in February 2021, most will hold as they don’t see alternatives offering a similar return. From the alternative credit universe I work across, I do see options that will deliver a similar return and with lower risk so I would be selling now and reinvesting elsewhere.

However, if you think the call could occur in May or later, then selling now starts to become a clearer call. I’ve seen some research arguing that NAB is motivated to call in February, without a decisive reason why. NAB still receives some capital attribution for these securities through 2021, so I’m not convinced that they need to move early in the year. They might think the pricing for a replacement security is fantastic in February and make it happen straight away, but equally they could wait until August hoping for a lower margin then. Holding out until November seems less likely as NAB would run the risk that pricing moves against them and they are stuck issuing at a higher margin, but it’s still a possibility. I’ve left off the table the low probability event that NABHA extends beyond 2021, but if that did occur the return would be poor relative to alternatives and those who held would be disappointed once again.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors. Enjoy this wire? Hit the 'like' button to let us know.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

........

This article has been prepared for educational purposes and is in no way meant to be a substitute for professional and tailored financial advice. It contains information derived and sourced from a broad list of third parties and has been prepared on the basis that this third party information is accurate. This article expresses the views of the author at a point in time, and such views may change in the future with no obligation on Narrow Road Capital or the author to publicly update these views. Narrow Road Capital advises on and invests in a wide range of securities, including securities linked to the performance of various companies and financial institutions.

3 topics

1 stock mentioned

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management