The Global Economic Backdrop

The global environment remained constructive for most of Q3, however several important risks intensified. The Federal Reserve’s rate hikes contributed to an appreciating US dollar putting pressure on several emerging markets currencies, most notably the Turkish lira. A breadth of populist pressures in the eurozone, as well as signs of slowing growth in China have complicated efforts to deleverage and rebalance the economy. Increasingly aggressive US protectionism has exacerbated all of these challenges.

Looking ahead to the fourth quarter, we continue to weigh our relatively optimistic view of global economic fundamentals against our rising concerns. We see potential upside in equity markets, but we believe returns will be moderate and driven by earnings growth more than multiple expansion.

Higher risks will likely weigh on sentiment and contribute to volatility, making security selection and market differentiation important. Finally, we see developed markets sovereign bonds as relatively unattractive and believe there are benefits to alternative diversifiers.

Our View

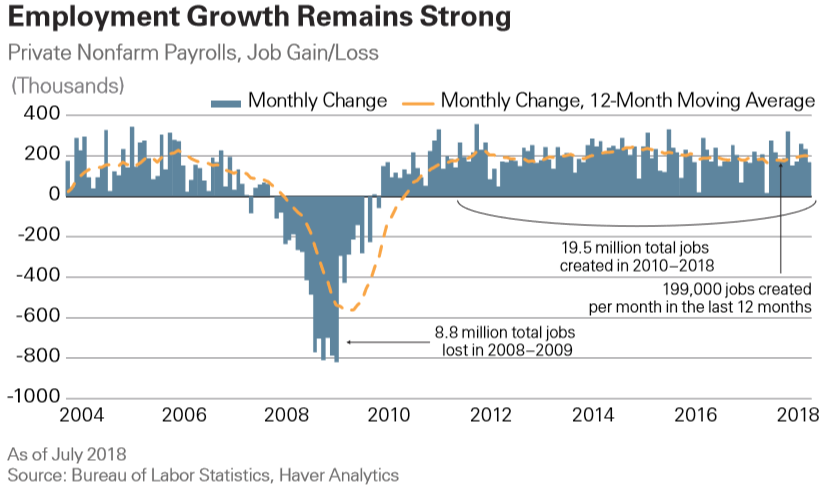

United States - Middle Class Recovery Continues

- US domestic demand growth rebounded from a relatively weak first quarter to above-trend levels, expanding by an annualized rate of 3.2% in real terms in the first half of 2018. We expect this pace to continue through the end of the year, as the US middle class continues to benefit from the ongoing expansion and as stimulus from the tax plan passed in December 2017 and the federal budget passed in February 2018 add to growth.

- After stagnating for 15 years, real US median household income is growing at its fastest pace since the 1960s, due to rising employment and broadening wage growth. Encouragingly, even as the unemployment rate has fallen to its lowest level since 2000 and, before that, 1969, employment growth has remained strong. As a result, many Americans have rejoined the labor force after giving up on their job searches following the global financial crisis.

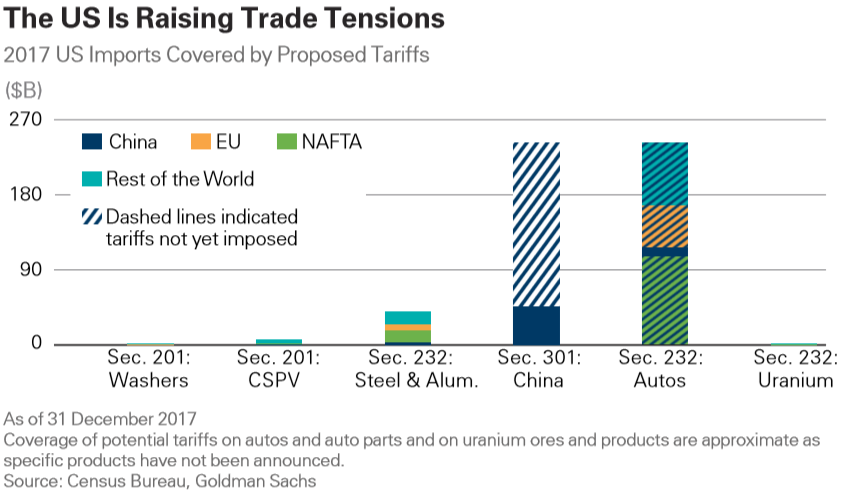

- However, increasingly aggressive US trade policy risks slowing this momentum. New tariffs currently cover about $95 billion in 2017 US imports and have drawn proportionate retaliation from many US trade partners. President Donald Trump’s administration has threatened more tariffs, which would represent a significant escalation—affecting at least another $200 billion in imports from China and potentially $240 billion in auto and auto parts imports. These numbers are small in the context of a $20 trillion economy. However, it is much harder to quantify the potential impact of protectionism on confidence and investment decisions, as well as the disruption to global supply chains, profit margins, and ultimately demand for goods and services.

Eurozone - Populism a threat amid a slow recovery

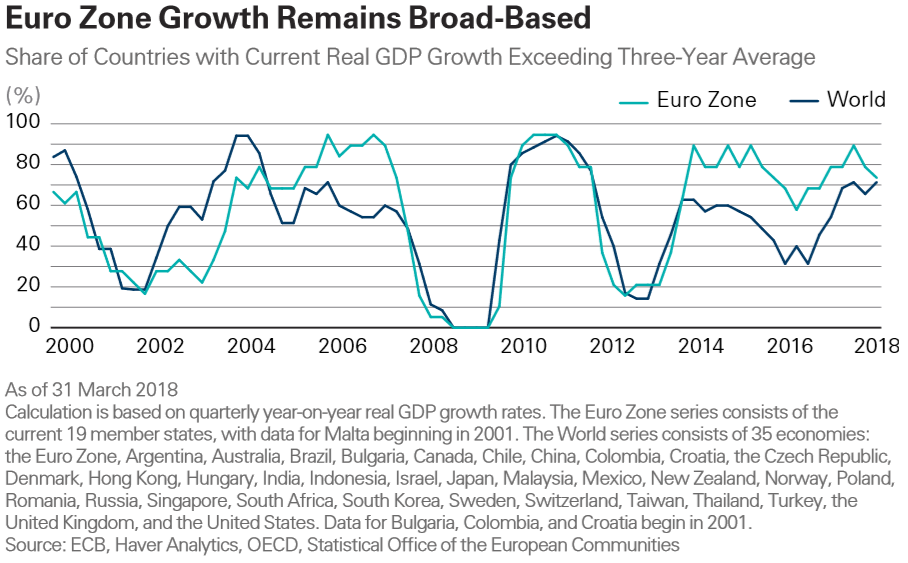

The euro zone economy slowed from relatively fast real growth of 2.8% in 2017 to 1.5% annualized in the first half of 2018. However, despite this deceleration, its expansion remains solid and broad-based, with nearly three-quarters of euro zone countries growing more rapidly than their three-year average.

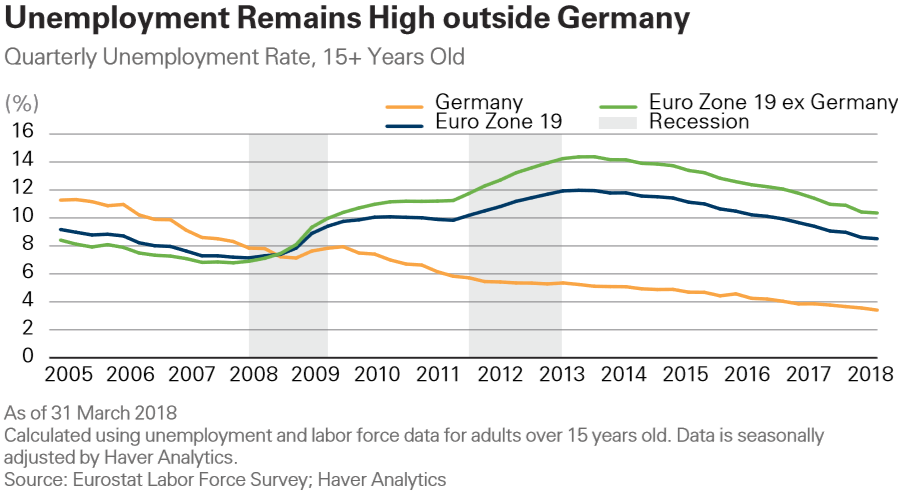

Furthermore, slow progress in the early years of the recovery means that there is significant runway for further expansion, as is reflected in labor markets. While the German unemployment rate has fallen to a historic low of 3.4%, the unemployment rate in the rest of the euro zone is still 3.5 percentage points above its precrisis level, a gap that would take almost 2.5 years to close at current rates of employment growth.

This slow recovery continues to pose a political risk. In Italy a new populist government has come to power on a platform that would raise public debt, with the potential for confrontation over fiscal rules when it submits its first budget to European Union authorities in October. Elsewhere, many other governments have been weakened by challenges from outsider parties—including in Germany, where in June, a rift appeared in the governing coalition over immigration. Populist risks to confidence, euro zone cohesion, and growth are complicated by a number of other pressures: negotiations on Brexit, US protectionism, and any geopolitical consequence of potentially severe economic difficulty in Turkey.

China - Walking a policy tightrope

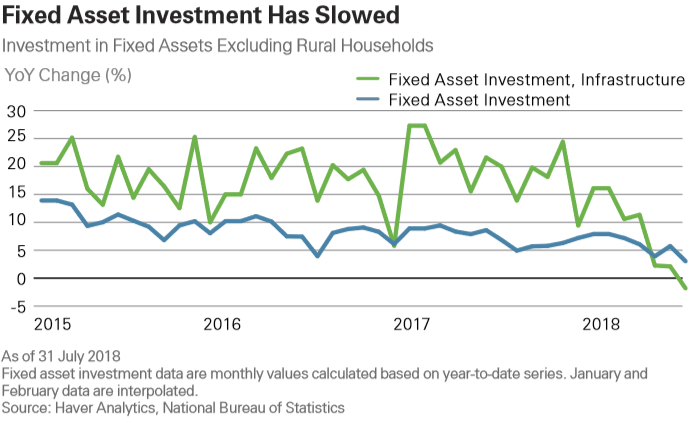

China has maintained rapid growth since the global financial crisis in part through rising leverage, particularly in the corporate sector, where debt is now 160% of GDP. Reducing debt and financial system risk has become a priority in Xi Jinping’s second term, and corporate leverage as a share of GDP has leveled off while household debt has continued to rise from a lower base. However, in recent months several economic indicators have suggested that slowing credit growth is resulting in reduced economic activity. In particular, fixed asset investment growth fell to its slowest pace in two decades, due to declining infrastructure investment.

Chinese authorities have begun to provide additional liquidity to the banking system, through cuts to required reserve ratios (Exhibit 6) and other targeted measures.

We expect further monetary easing, as well as fiscal stimulus to revive infrastructure investment. However, recent challenges illustrate the difficulties of calibrating policy to both rebalance the economy and maintain rapid growth. Furthermore, trade conflict with the United States could add to the need for stimulus, complicating efforts to contain debt and asset price bubbles. One related dilemma is the roughly 9% depreciation of the renminbi against the US dollar since June. While a weaker renminbi bolsters exports and helps counter tariffs, we doubt authorities will tolerate substantial further depreciation, given the risk of repeating the capital outflows experienced in 2015 and 2016.

Investment Implications

While we are growing increasingly concerned about populism and protectionism, we maintain our optimistic outlook for the global economy and expect continued earnings growth in the fourth quarter of 2018. We anticipate especially strong earnings growth in the United States, where corporate tax cuts have led to a step change in earnings. Moreover, we believe current equity market valuations appear to be sustainable, given low interest rates. Valuations in the United States are highest relative to their history, reflecting the United States' relatively strong economic outlook. Going forward, we expect equity returns to be driven by earnings growth and to be lower than in 2017.

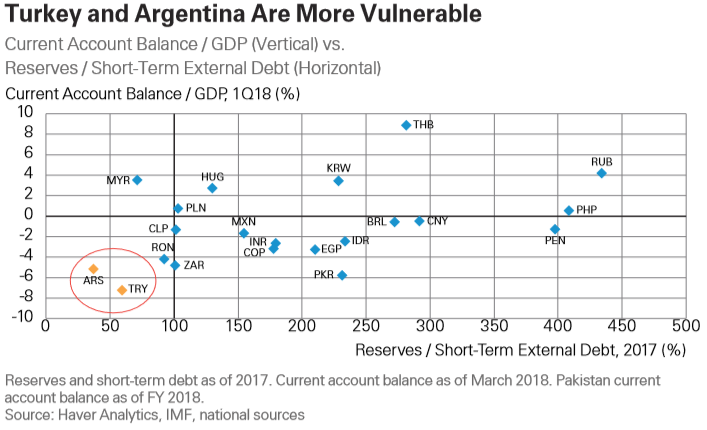

We expect that heightened political and geopolitical risks will continue to weigh on sentiment and lead to higher volatility. This type of equity market environment—characterized by more modest returns and higher volatility—should be more favorable to active managers as security selection and market differentiation become especially important. For example, the risks of direct economic contagion from Turkey and Argentina are relatively low, in our view, and we believe recent stress in both economies reflect specific vulnerabilities rather than systematic problems for emerging markets.

Given continued growth, we also expect both inflation and interest rates to grind higher, though both are likely to remain well below “normal” levels of prior cycles. Consequently, we view developed markets fixed income as unattractive. While rates remain exceptionally low in Japan and the euro zone, we would reevaluate this view in the United States to the extent the 10-year Treasury reaches a yield meaningfully above 3%.

You can read our full report on "The Global Economic Backdrop" here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with Lazard’s Geopolitical Advisory group to assess economic and market implications of key geopolitical issues globally. Ron also advises clients of Lazard’s Asset Management businesses regarding macroeconomic and market considerations that are important to achieving their objectives. Previously, Ron was the Head of US Equity and Co-Head of Multi-Asset Investing for Lazard Asset Management. In this role, Ron was responsible for overseeing the firm's US equity strategies, Multi-Asset investing, as well as several global equity strategies. He was also a Portfolio Manager/Analyst on various US and global equity teams.

.png)

.png)

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with...

Expertise

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with...

Expertise

Comments

Comments

Sign In or Join Free to comment