The Great State Bailout

It’s an issue that has passed under the radar here in Australia but it is of great political, economic, legal and credit risk interest. It’s the argument over whether the US Federal Government should be bailing out profligate state governments. It has strong parallels to Europe where there are ongoing calls (and recently some action) for thrifty northern Europeans countries to bailout their spendthrift southern counterparts. In the US it’s been classified as a red state (Republican) versus blue state (Democrat) battle, but it isn’t as clear cut as that when you get into the detail.

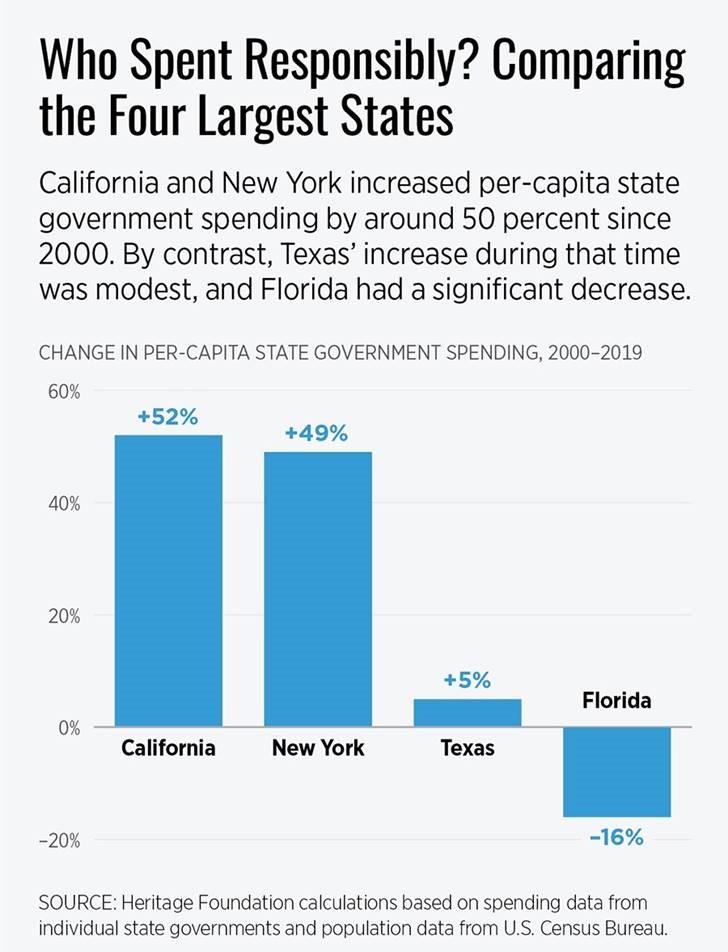

At the heart of the issue is whether the US Government should use its quantitative easing power to either gift or lend money to states and local governments that are struggling to raise debt at low interest rates. If bailouts occur, it is essentially all taxpayers giving money to the taxpayers in the states that have consistently failed to take action to balance their budgets. The chart below from Dan Mitchell’s International Liberty blog gives an illustration of one way to view the problem. Obviously, Texas and Florida resent the idea of New York and California getting bailouts.

It's interesting at a legal level as there is debate over whether states can go bankrupt. The default and debt restructuring in Puerto Rico (technically a territory not a state) shows that if politicians want to change the rules they’ll find a way to do it. I expect the public will generally support them in this endeavour, would voters/taxpayers support paying more to lenders when they are receiving cutbacks in the government payments and services they receive?

At the economic level, it’s an interesting test case and outworking of MMT. MMT proponents typically acknowledge that state governments can’t spend endlessly as they don’t print their own currency, whereas some federal governments can (theoretically) print their own currency endlessly. In theory this means that governments can all spend endlessly if they work together, but in practice it’s not that simple. Some states believe in old school economics where the amount and quality of spending and taxation matters whereas other states believe in funny money. History shows that old school economics brings old school economic growth, whilst funny money (QE, deficits, low interest rates) delivers lower productivity and asset price/debt bubbles.

At the credit risk level it brings a new angle to the default risk of both states and local governments. Bailouts might delay bankruptcy for years or decades at the state level. If there’s no bailouts, Illinois could be a test case on the political and legal questions of state bankruptcy in the next few years. Other states a bit further behind are Connecticut, Kentucky and New Jersey with a whole bunch of local governments now in financial trouble.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

........

This article has been prepared for educational purposes and is in no way meant to be a substitute for professional and tailored financial advice. It contains information derived and sourced from a broad list of third parties and has been prepared on the basis that this third party information is accurate. This article expresses the views of the author at a point in time, and such views may change in the future with no obligation on Narrow Road Capital or the author to publicly update these views. Narrow Road Capital advises on and invests in a wide range of securities, including securities linked to the performance of various companies and financial institutions.

3 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management