The opportunity of the century?

Gree Electric, Zhejiang Supor Cookware, Fuyao Glass. If you know much about any of these three companies, I take my hat off to you. Gree is the market leader in air conditioning in China. Zhejiang is the country’s largest manufacturer of pressure cookers, blenders and other small kitchen appliances. Fuyao is the world’s only pure automotive glass company. I must confess, I’d never heard of any of them.

All three are listed on China’s domestic A-share markets in Shanghai and Shenzhen, and all three are pretty much unknown in the outside world. Why am I telling you this? Because I suspect that quite quickly the black box that is China’s onshore stock market could become a whole lot more transparent. It may be a while before these companies roll off the tongue like Apple, Siemens and Samsung, but the days when China’s best-known stocks elicit blank stares are numbered.

Last week MSCI, a New York-based company that creates the indices that investors use to measure the performance of stock markets, lifted the lid just a fraction on the hidden world of China’s A-shares. Three years after first toying with the idea of adding Shanghai and Shenzhen-listed shares to its widely-followed emerging market index, it finally took the plunge. Foreign investors who track the performance of this benchmark will find it difficult to continue pretending that the world’s second biggest stock market does not exist.

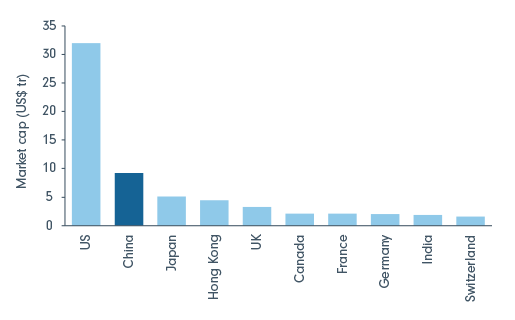

The A-Share market in China is valued at around $7trn and lists more than 3,000 companies, yet big Western investment houses have been more than happy to ignore it, accessing the world’s second biggest economy via the far smaller number of mainland Chinese companies which have taken the trouble to get their shares listed in either Hong Kong or New York.

It’s not hard to see why. Many overseas investors who have ventured into the Wild West of the Chinese market have discovered to their cost that different levels of due diligence apply. Corporate governance in China is, shall we say, less developed than they are used to at home. The regulation of stock markets is less rigorous. The ease with which Chinese companies suspended trading in their shares at the first whiff of a market meltdown during the 2015 correction confirmed the old emerging market adage: they’re hard to emerge from in an emergency.

What changed this year? A key change in the Chinese stock market over the past couple of years has been the creation of the so-called Stock Connect link between the two big mainland Chinese markets and the foreigner-friendly bourse in Hong Kong. With up to $2bn of trades allowed to pass in either direction every day, investors are more reassured today that not only can they put their clients’ money into Chinese stocks but they can also take it out again. The support of big institutional investors (the principal users of MSCI’s indices) has been crucial.

Don’t think, however, that a new investment El Dorado has suddenly been opened up to overseas investors. The door has been opened just a crack by MSCI. These are baby steps. First, only 222 A-shares have been deemed large and liquid enough to be included in the Emerging Market index. Furthermore, because only 5pc of their actual market value is used in MSCI’s calculations, they will have just a 0.7pc weighting in the benchmark. MSCI is coy about the conditions under which that might move closer to a more representative exposure.

MSCI is right to be cautious. More than two thirds of the 222 companies are effectively run by the Chinese state. Government control of the banking system means the supply of credit to companies is driven by bureaucratic fiat. China remains a uniquely policy-driven economy, hard for outside investors to navigate, with a regulatory framework that evolves at a rapid pace.

The A-share market is also dominated by retail investors, who are influenced by short-term swings in sentiment and have a tendency to overpay for apparent growth levels that are not sustainable over an economic cycle.

That’s the bad news. The flip side of all this is a market full of opportunity, with sketchy research coverage of stocks giving investors on the ground a genuine information advantage that is much harder to achieve in more developed markets. Including A-shares in MSCI’s indices will bring new capital into the market, reduce volatility and help create a better-regulated, smoother investment environment.

The enthusiasm of Chinese retail investors for get-rich-quick growth stories makes the A-share market a happy hunting ground for value-focused investors with a longer time-frame. There are many domestically-focused stocks only listed on the A-share markets that are well-placed to benefit from the ongoing shift towards a more consumption-driven Chinese economy. There are plenty of companies with steady growth prospects, undemanding valuations compared with global peers and even attractive dividend yields. Many of the home appliance manufacturers like Zhejiang Supor can only be accessed through the mainland markets.

One final lesson that investors might take from MSCI’s adjustment to its Emerging Market index is the fact that passive investing is a lot less mechanical and systematic than they might have thought. The fact that a small index provider in New York can effectively decide how much global investment giants should be directing towards the Chinese stock market suggests that index tracking is more arbitrary than its proponents might claim.

In the meantime, what can you tell me about China Vanke, Baidu or Nexteer Automotive?

To find out more about the Fidelity China Fund, please click here

Investments in small and emerging markets can be more volatile than investments in developed markets. Investments in overseas markets can be affected by currency exchange and this may affect the value of your investment.

Reference to specific securities should not be taken as recommendations and may not represent actual holdings in the portfolio at the time of this viewing.

This document is issued by FIL Responsible Entity (Australia) Limited ABN 33 148 059 009, AFSL No. 409340 (“Fidelity Australia”). Fidelity Australia is a member of the FIL Limited group of companies commonly known as Fidelity International.

This document is intended for use by advisers and wholesale investors. Retail investors should not rely on any information in this document without first seeking advice from their financial adviser. You should consider these matters before acting on the information. You should also consider the relevant Product Disclosure Statements (“PDS”) for any Fidelity Australia product mentioned in this document before making any decision about whether to acquire the product. The PDS can be obtained by contacting Fidelity Australia on 1800 119 270 or by downloading it from our website. While the information contained in this document has been prepared with reasonable care, no responsibility or liability is accepted for any errors or omissions or misstatements however caused. This document is intended as general information only. The document may not be reproduced or transmitted without prior written permission of Fidelity Australia. The issuer of Fidelity’s managed investment schemes is FIL Responsible Entity (Australia) Limited ABN 33 148 059 009. Reference to ($) are in Australian dollars unless stated otherwise.

© 2017 FIL Responsible Entity (Australia) Limited. Fidelity, Fidelity International and the Fidelity International logo and F symbol are trademarks of FIL Limited.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Fidelity International

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Fidelity International

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Comments

Comments

Sign In or Join Free to comment