The Outlook for Global Growth

We recently attended the well supported Capital Economics (CE) Conference on The Outlook for Global Growth. In total there were more than 90 slides and charts presented. At the risk of over-simplification, 6 key points stood out to us:

United States

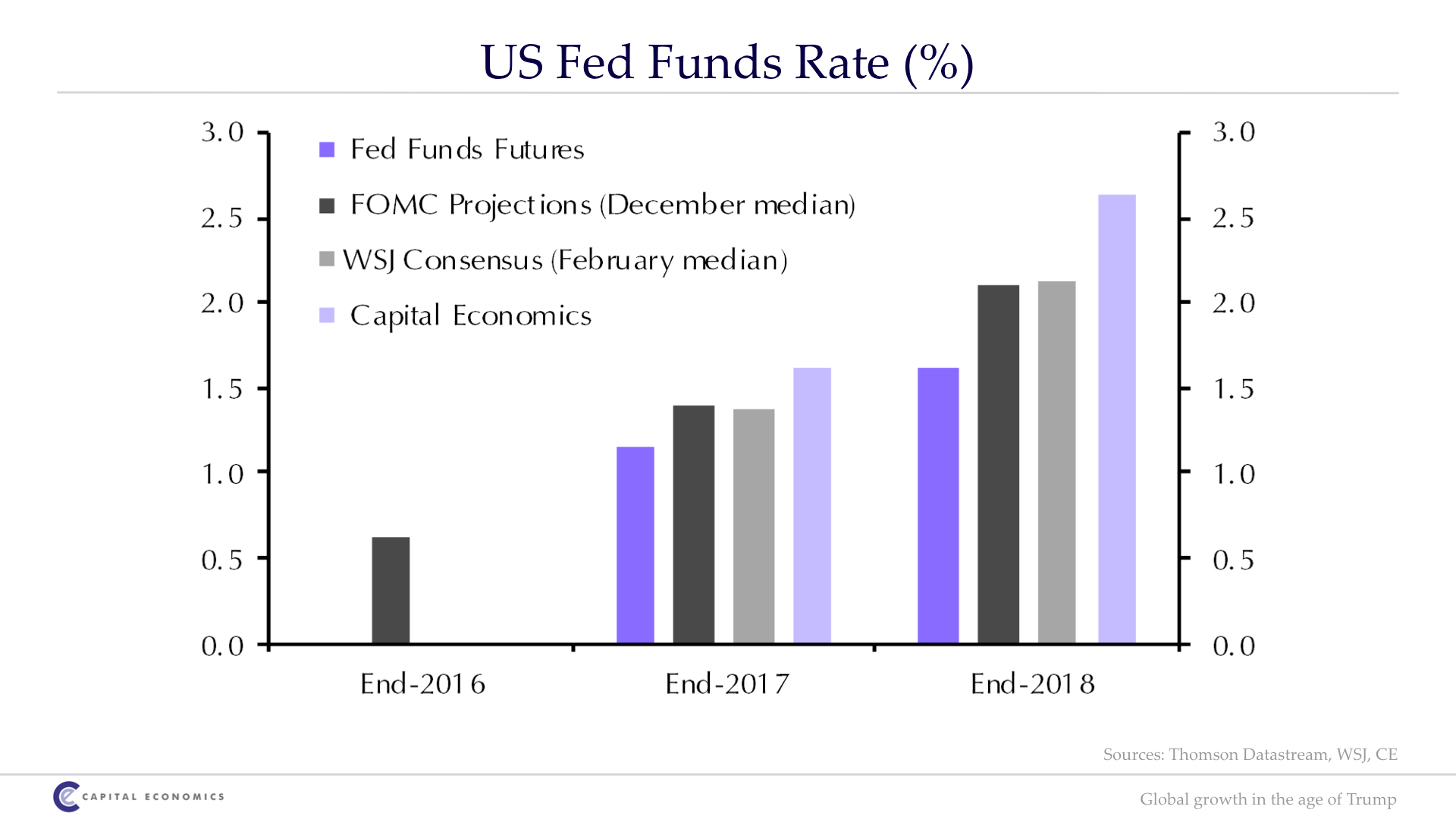

1. The United States’ economy is already operating at close to capacity. Trump’s planned FISCAL package is in reality politically inspired not economically required. As a result, the greater risk is that it leads to over-utilisation and hence inflation. CE are forecasting top of the street rate rises in the US of 100 basis points in both calendar years 2017 and 2018.

Source: Capital Economics

United Kingdom

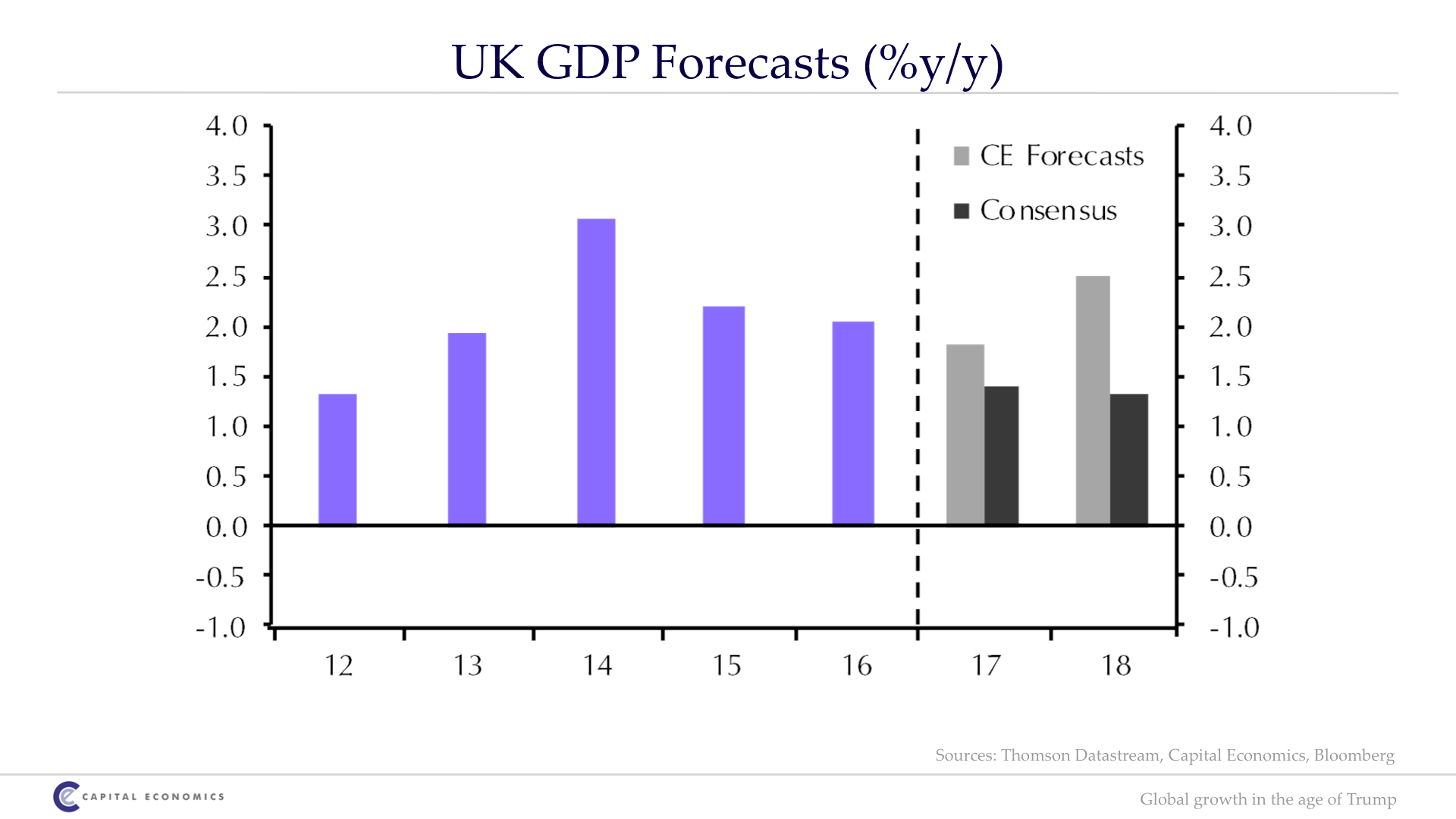

2. Rapid regulatory intervention, and the declining pound sterling, will largely insulate the UK from the effects of BREXIT. CE is forecasting UK growth to accelerate into 2018.

Source: Capital Economics

China:

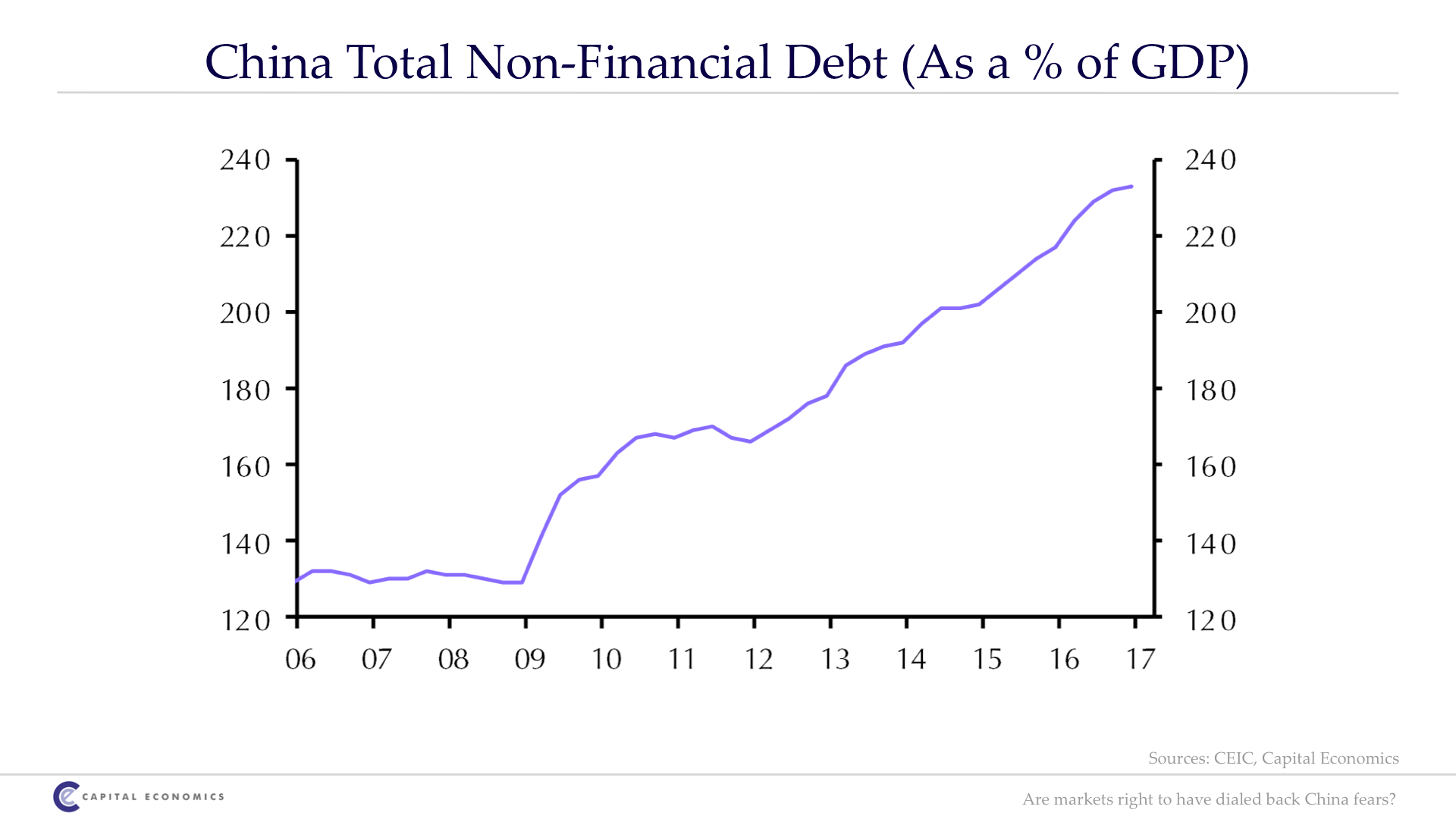

3. A debt crisis is brewing in China, but it is still some way off. The likelihood of a crisis in China near term is slim.

Source: Capital Economics

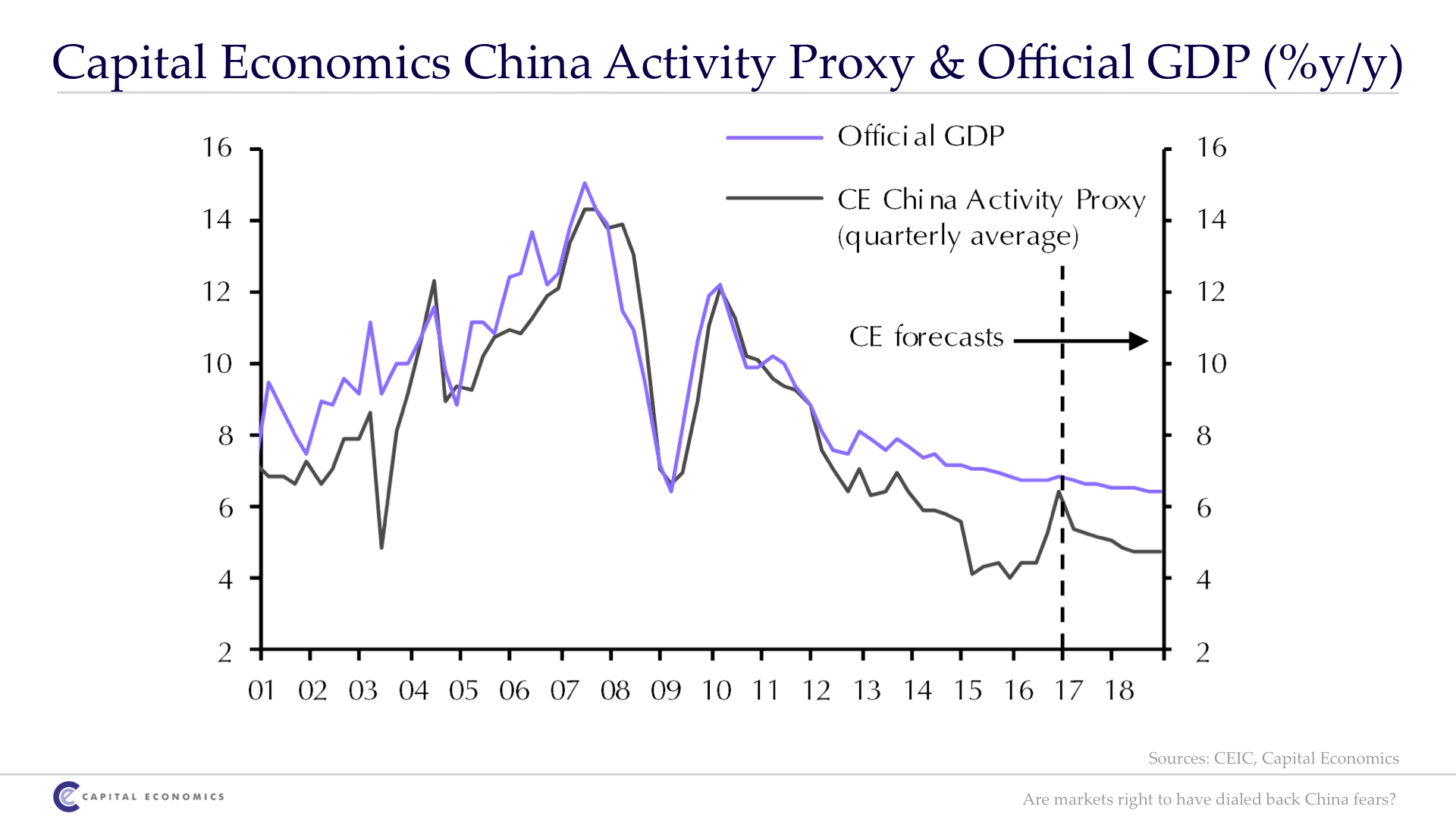

4. Over the next decade, GDP growth of 4-5% per annum would be a ‘good’ outcome but requires that the Government act (soon) on bad debts, which are accentuating the misallocation of capital. Without proper reform, GPD growth may drop to 2% per annum.

Source: Capital Economics

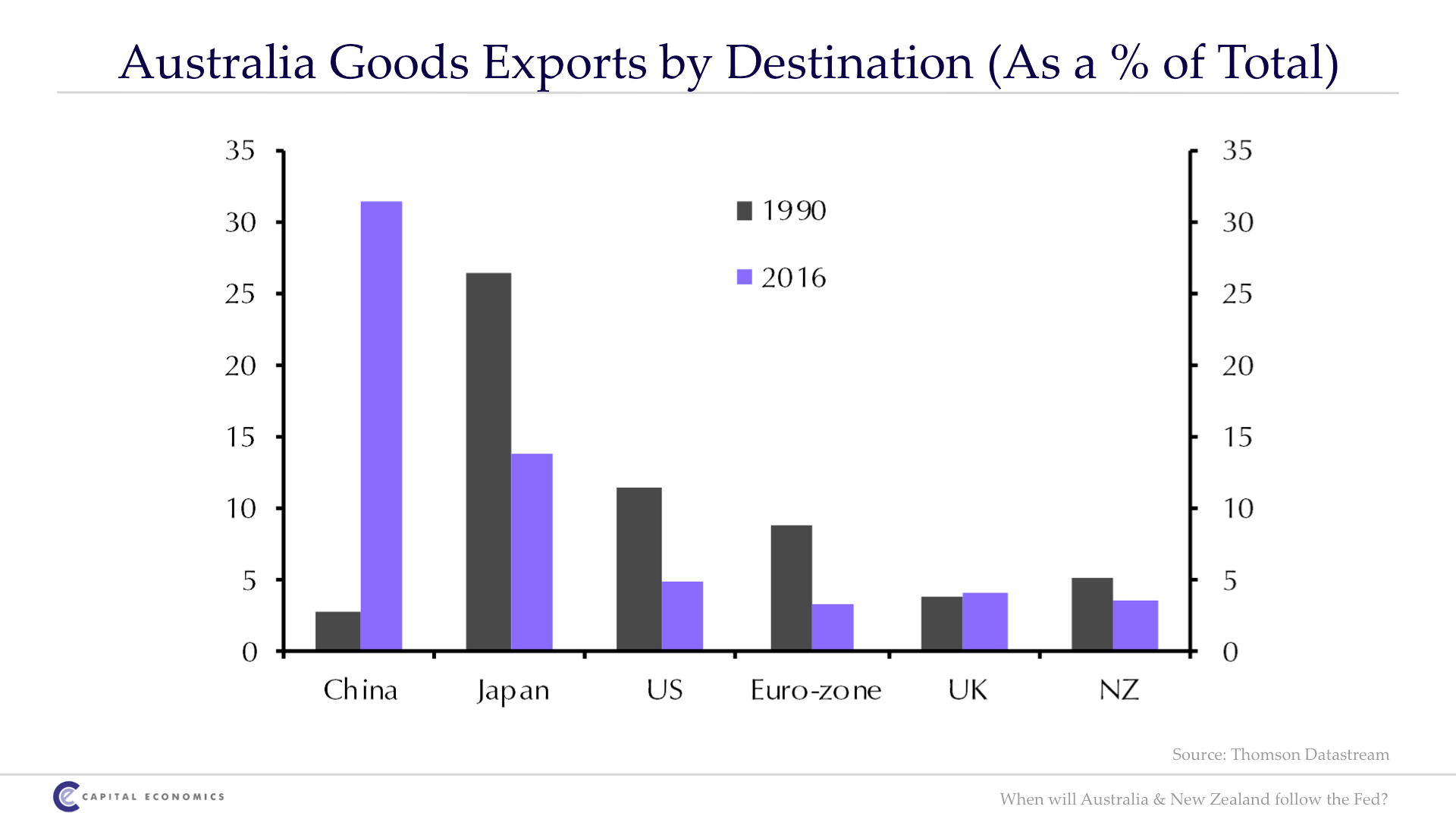

Australia:

5. More than 30% of all exports are now to China – greater than Japan, the US, Europe, the UK and NZ combined. If China sneezes, forget about a cold – Australia is going straight to the intensive care unit.

Source: Capital Economics

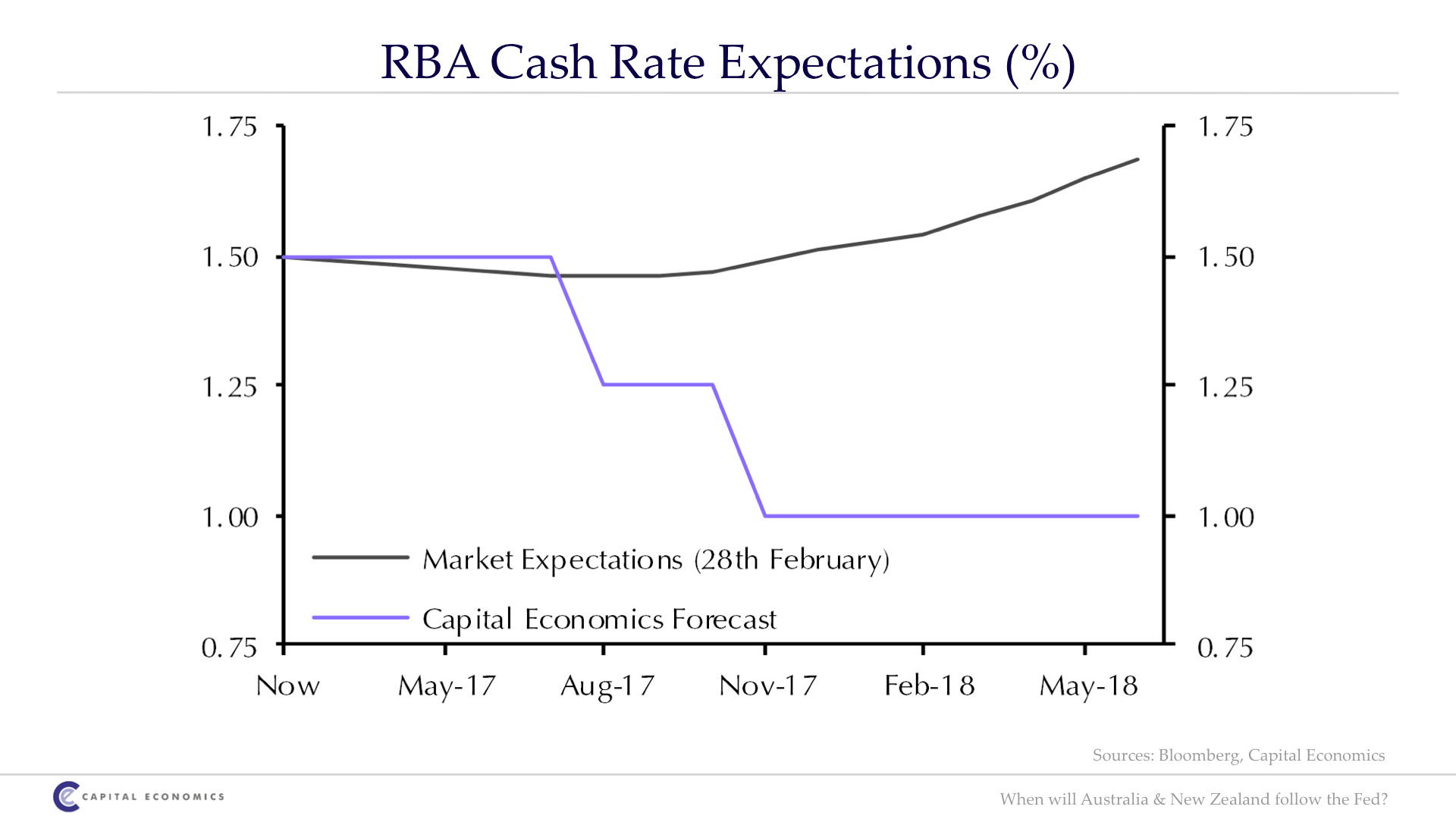

6. And CE is forecasting that China will sneeze this year and that the iron ore price will exit CY2017 at around $US50 per tonne. As a result, CE has made a highly non-consensus call that the RBA will drop rates twice in 2017 and end the year at 1.00% - below the official rate in the US. It’s a stretch, but the rationale is valid should China slow infrastructure spending.

Source: Capital Economics

A key thematic, from our interpretation at least, is that many of the underlying structural issues in the four major global engines (US, China, Europe and Japan) have not been resolved but rather delayed. The outlook for the foreseeable future is positive. However, at some point – perhaps around 2020 – debt levels, inflation and the structural misallocation of capital will create an even bigger obstacle to global growth than what has been experienced thus far.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

.jpg)

2 topics

.jpg)

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Comments

Comments

Sign In or Join Free to comment