The Path to Whiskey Riches

Lark Distilling Co. (LRK), founded in 1992 and formerly known as Australian Whiskey Holdings (AWY), is the owner of the Lark Distillery in Tasmania. Lark was the first boutique Australian whiskey distillery to open after amendments to the 1901 Distillation Act, which previously made it difficult for boutique distilleries to open and operate.

Whilst Lark was the first, Bill was involved in helping to set up or manage numerous other distilleries including Sullivan’s Cove in the late 1990s and while Lark has not yet gained the global recognition that I think the brand is destined for, it was the genesis of the now flourishing Australian boutique spirits industry.

The recent rebranding to Lark Distilling Co. coincided with the complete refresh of the business in 2019 after a challenging period post the initial acquisition of Lark by AWY. AWY was a listed vehicle which was rolling up domestic whiskey and spirit brands, with a focus on Tasmania. It was poorly run, consumed huge amounts of capital for little success (raised $24m + script used for acquisitions over 2017/18), and arguably made poor capital allocation decisions.

The perennially underperforming capital incinerating dumpster fire that was AWY came to a head in April 2019 when a 249D was called by substantial shareholder Quality Life Pty Ltd.

The 249D sort to remove 4 of the 5 directors not named Bill Lark and replace them with two new directors in Geoff Bainbridge (Former MD of Sprits for Fosters, ex-Grill’d co-founder) and David Dearie (ex-CEO of Treasury Wines) who are the current the MD and Chairman respectively.

The 249D was successful with Geoff, David and also Warren Randall (MD of Seppeltsfield Winery) joining the board. I note Seppeltsfield became a material shareholder in AWY via the conversion of convertible notes in 2018. Bill went on to resign from the board but remained with the company as Brand Ambassador. Acting CEO and CFO Brendan Waights also resigned on the same day. This clean out marked the final low and turning point in the AWY saga.

Since then, Geoff moved into the MD role (October 2019) whilst the board was further strengthened with the appointments of Laurent Ly (via sub holder Ace Cosmo Developments) and Laura McBain (ex-CEO of Bellamy’s). It is also worth noting that insiders have been actively purchasing stock with Geoff and Laura buying >$2.5m on-market over 2020, and at current levels.

What is the New Strategy?

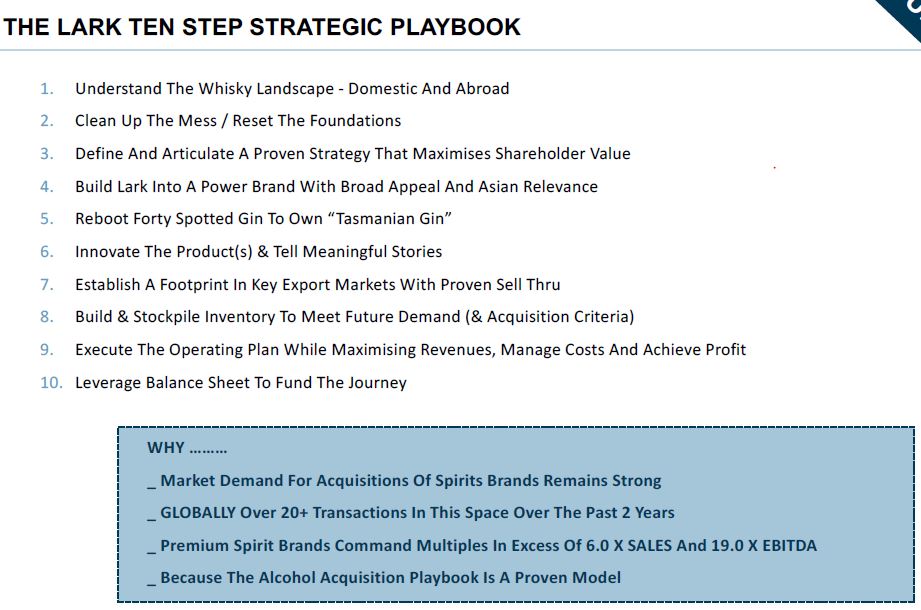

Great question reader! The strategy was initially detailed in the 2019 AGM presentation (slide 9) and covers a 5 year plan to support a 10 year vision. This was later distilled into a 10 step playbook (image below) to turn LRK it into a globally recognised and leading Tassie whiskey brand. The key is putting the business in a position to scale production to meet the huge demand profile that comes with achieving this vision.

Source: LRK investor presentation May 2020

The first step was to review what they had, what can be done with it and tie up the loose ends from the Nant investor barrel scheme. This saw the divesture of all brands down to Lark, Nant and Forty Spotted. Whilst the Nant brand is retained, it is not the focus whilst it also has value in use for blended whiskey product lines (i.e. Symphony No 1).

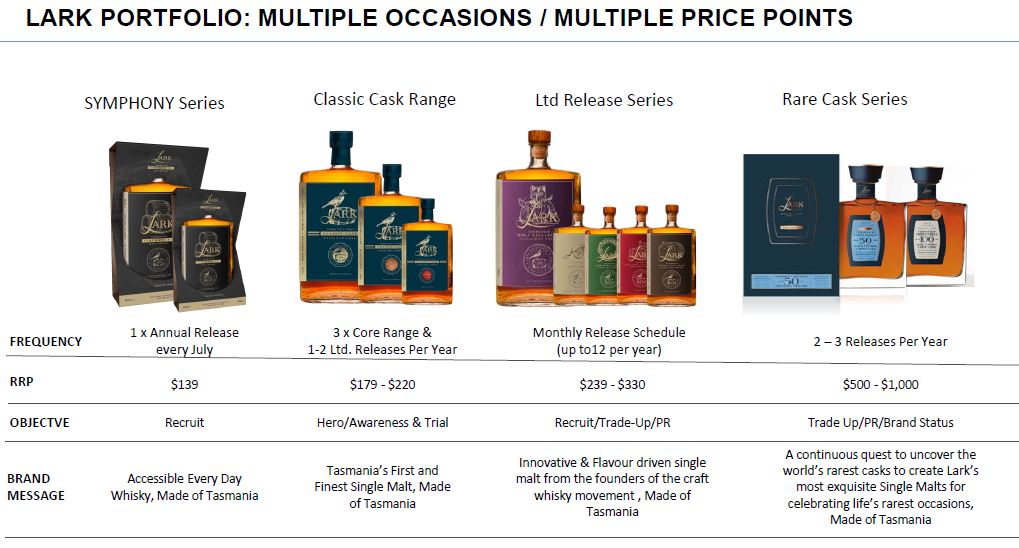

With the Lark brand, a complete overhaul of the product range and tiering was put in place. This included producing more premium and limited batch variants in addition to developing blended variants for mass market. The expansion of limited and rare range series comes hand in hand with the expansion of distilling rates as these limited ranges are taken from the tails (i.e. barrels that don’t meet the spec of the core range) but can be enhanced to become their own spec. Thus, as distilling rates go up, the volume of variants in the limited range also increases thus adding further potential incremental value from the average unit economics of a barrel.

This tiering is illustrated below:

Source: LRK capital raise presentation Sept 2020

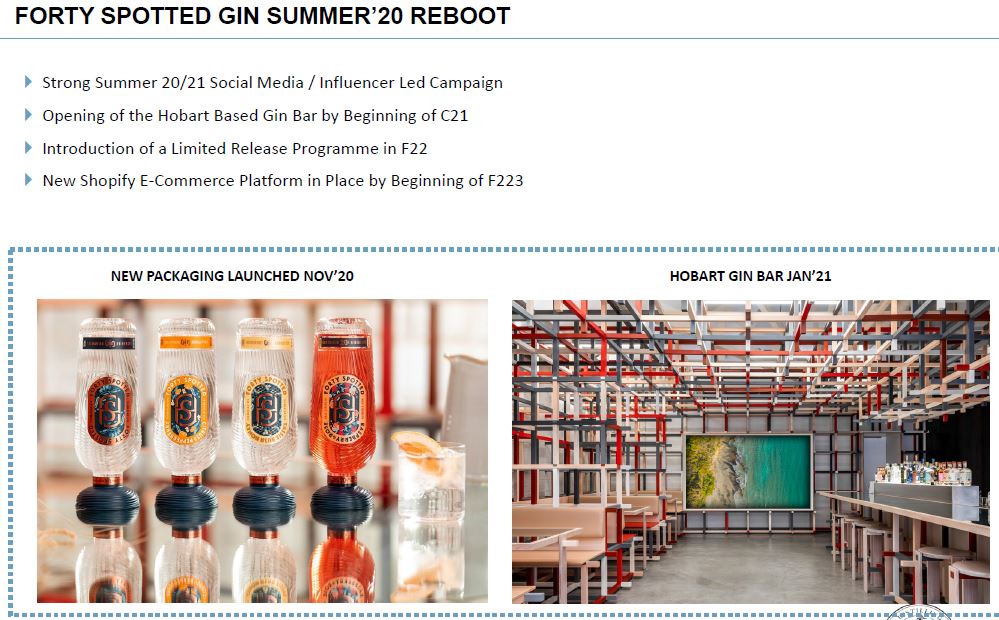

In addition to the expansion of the Lark product range, Forty Spotted is undergoing a major brand refresh which required a reformulation and revamp of product ranges, including tapping into the lower alcohol segment within the category. Whilst gin may not come with the story telling lustre of whiskey, there remains a good opportunity to create a leading Tassie brand for the domestic market in which domestic brands have a small market share.

Source: LRK AGM presentation Nov 2020

The next step was to refresh distribution channels which initially meant terminating most agreements, particularly those providing export market exposure and focusing on expanding the brand within Australia via retail and online channels. As a result of COVID19, online channels became further prioritised as hospitality took a major hit, which helped sales rebound faster than the recovery in hospitality over the second half of 2020.

To support all this, LRK has invested in the business through marketing and into capex to expand production capacity and fill more barrels. They raised $5m in debt (March 2020, from Quality Life, at great rates) and $8.9m in equity (September 2020) which brought pub baron Bruce Mathieson onto the register. If management get the execution right, this is likely the last equity raise needed to support working capital for planned organic growth.

Capacity expansion is achieved through expansion of existing facilities and third party distillers. The latter is used for the mass market product which goes by the code name AX8. LRK has aggressively utilised this expanded capacity with production rates now at 5,600L/week up from 4,100L/week at the end of FY20 with the aim of ramping up further to meet a target of having 1.5m litres of whiskey under maturation by the end of FY22.

As at 30 October 2020, LRK has ~788k litres under maturation for an inventory value of ~$110m (net sales value at maturation), which was up ~63% YoY. The aggressive expansion of inventory is required to support materially higher sales levels expected over the coming 3yrs+ if the company succeeds in achieving its vision.

Speaking of new successes, Lark was recently nominated as one of the 4 finalists for the IWSC’s whiskey distillery of the year after a strong showing in the whiskey competition with multiple gold and silver awards as detailed below. This can only help with the marketability of the Lark brand and improve its global recognition.

Source: LRK September 2020 Quarterly Report

After a successful turnaround through 2019/20, I believe LRK is now a compelling long term growth opportunity as it aims to become a scalable Tassie whiskey brand that can be taken to the world. The initial green shoots of longer term growth potential came through in the September 2020 quarter as net sales grew +78% YoY (larkdistilling.com sales up 400%) despite the impacts from Victorian lockdowns and broader hospitality sector recovery (sales still down 73% YoY in the period).

From this position of strength they’ve given guidance for FY21 of ~100%+ growth in revenues. Of note is that the September result was also EBIT positive and after excluding deferred tax and excise payments from COVID19, cash burn was modest at -$686k and driven by production/inventory growth. As a result of the rapid inventory growth, it is likely that near-term LRK will still burn cash despite producing accounting profits. Today’s modest cash burn is tomorrow’s bigger cash flows.

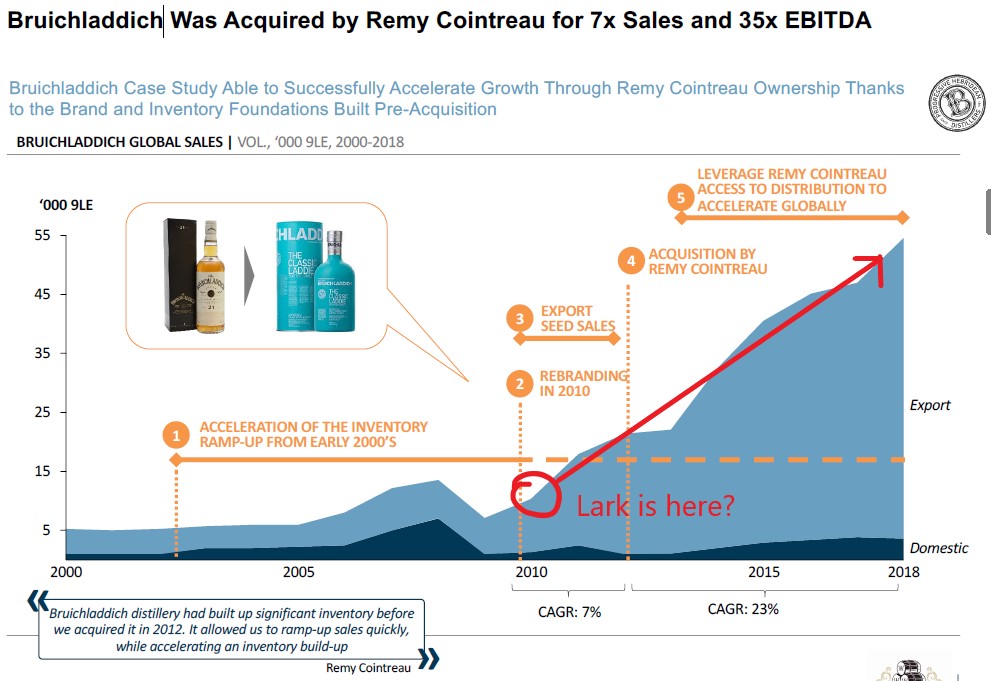

An analogy of the potential outcome of the new strategic vision offered by LRK in their 2019 AGM presentation is Bruichladdich Distillery, which went through a similar inventory barrel build up, rebrand, etc… before hitting a sales inflection in export markets and ultimately being acquired by Remy Cointreau ahead of the major, longer-term acceleration in sales growth.

Source: LRK AGM presentation Nov 2019

Although LRK can grow materially over the long term and be a highly lucrative investment in its own right, I believe it will eventually become a suitable target for a major spirits company. Whilst one would think that a distillery such as Sullivan’s Cove would be a better target given brand recognition, Sullivan’s Cove has had little interest in scaling production which is a turn off as acquisitions over the last decade show the majors tend to come in after inventory has been significantly built up and is shown to translate into strong sales growth. If LRK can successfully execute, it would receive extra attention as it would be the only scalable Tassie brand on offer and provide a new competitive advantage in a major’s portfolio.

Summary

I believe LRK has put itself in a successful position to go from whiskey pariah to whiskey champion as it builds a globally recognised and scalable whiskey brand, which I expect to be rewarding for investors with both tasty whiskey and share price gains.

Whilst still early in the growth leg after completing the turnaround of the business and navigating COVID19 through the acceleration of online sales channels, execution risk remains key to LRK. We think execution risk is mitigated by the highly experienced board and management team and their alignment with shareholders. Put simply, when the MD of a company buys >$2m of stock on-market like Geoff did recently, that should tell you something.

Whilst Dan Andrews’ best quote is “get on the beers”, at the Federal level it appears the mantra from ScoMo is to get on the Larks.

Cheers!

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Disclaimer: Any information contained in this article is limited to general information only, whilst the opinions and views detailed are those of the author only, and as such does not constitute advice or a recommendation in any capacity. The information contained in this article has not taken into consideration your specific financial needs, goals or objectives, so please consider consulting a licenced adviser before considering acting on this information.

The author owns shares in LRK at the time of publishing.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

2 topics

1 stock mentioned

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Comments

Comments

Sign In or Join Free to comment