The price of doing more fiscal policy

I was recently asked whether it is really true that the AA and AAA rated state governments are having to pay materially more to raise capital to fund their budget deficits than Australia's banks, which all have lower credit ratings---and in many cases substantially lower ratings in the higher risk BBB band (eg, Bank of Queensland, Bendigo, and ME Bank).

There is of course also the argument that the states are part of the federation and explicitly backed by it through revenue streams like the GST, whereas banks are less explicitly government guaranteed (they have a limited government guarantee of their deposits and various implicit guarantees).

This disconnect has been canvassed repeatedly in recent weeks by analysts, economists, and economics commentators, such as the AFR's highly regarded Canberra-based economics and politics correspondent John Kehoe in this story.

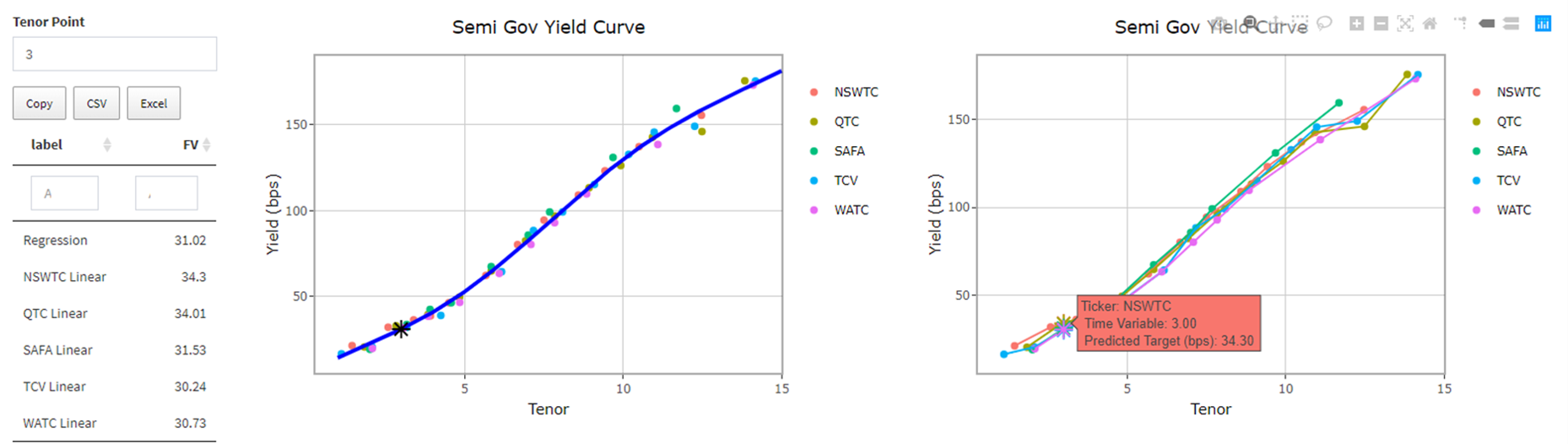

So let's examine the data. The three screenshots below highlight the price the various state governments pay to raise money at different maturities ranging from one year to more than 10 years. For three year money, states like NSW are indeed paying as much as 0.34% pa (see the table on the left-hand-side of the first image immediately below), which is materially above the price of three year money for banks, which is just 0.25% pa. The banks are currently accessing up to circa $200 billion of this funding via the RBA's novel Term Funding Facility (TFF). (Click on the image to see the data more clearly.)

In practice, state governments prefer longer-term funding of between 3 years and 15 years to match the capital investments required to build and fund long-dated infrastructure projects, amongst other things. And the longer the tenor, the more they have to pay for it.

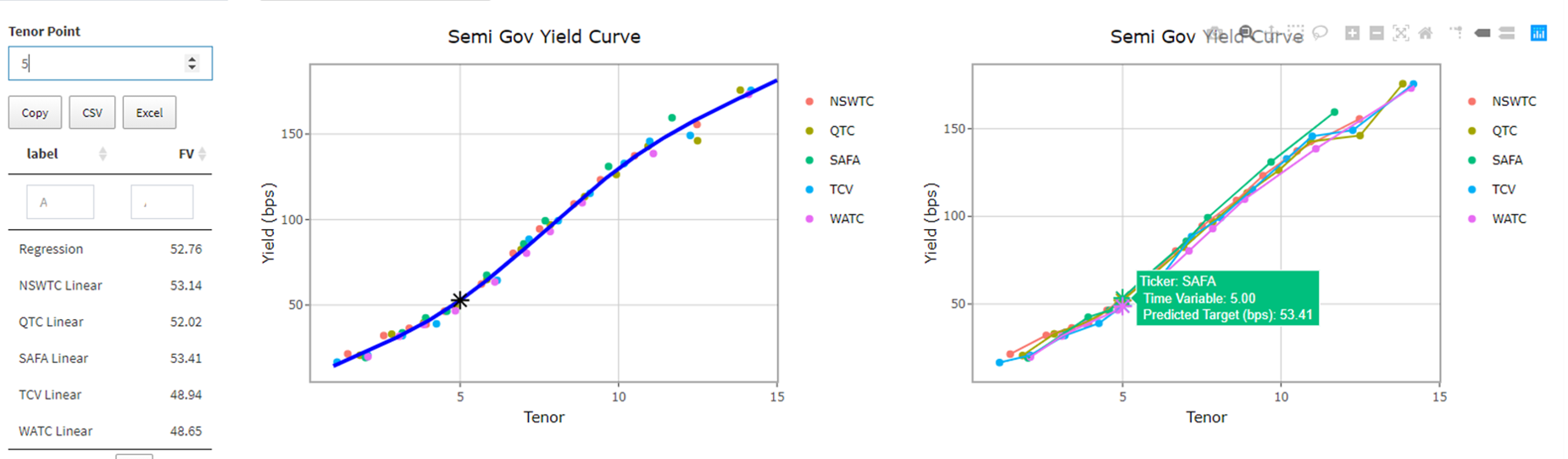

So when we look at the price of five year money (next image), it jumps to more than 0.53% pa for NSW (again see the table on the left hand side), which incidentally is especially odd because NSW right now has the most expensive cost of capital of all the major state governments out to about 10 years (ie, it pays more to raise money than QLD, Victoria, and WA). This is historically very unusual---as the biggest state with the strongest AAA credit rating, NSW has historically paid amongst the lowest prices to access capital---and particularly bizarre given S&P has put Victoria on watch for a 50% probability of a downgrade from AAA to AA+. (Click on the image to see a better version.)

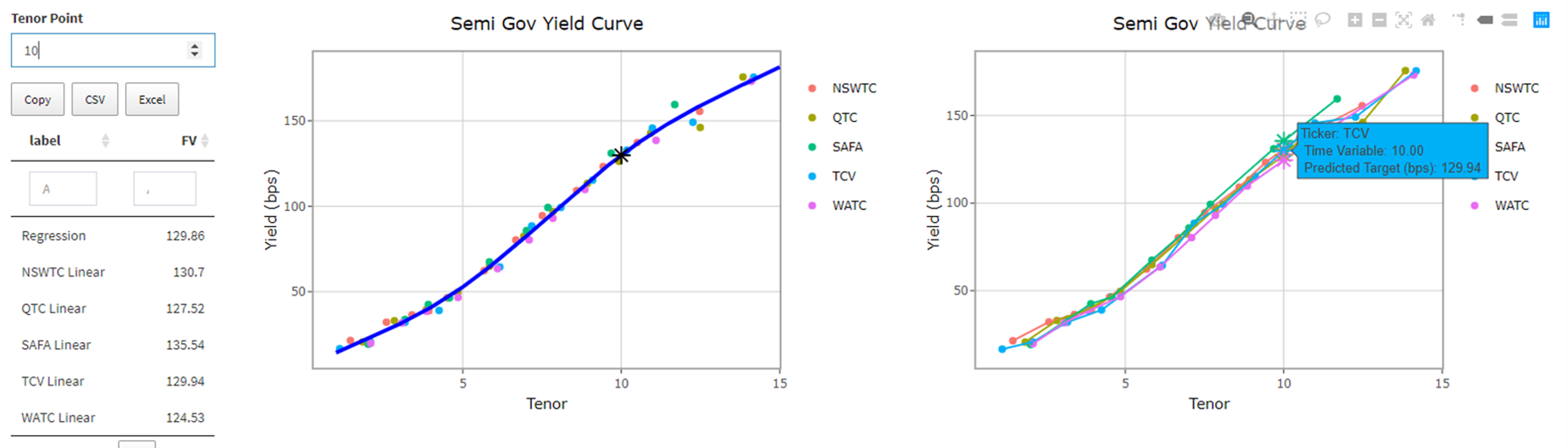

Since the states have been focussing on long-dated infrastructure investments in recent times, they have been often targeting funding of 10 to 20 years in term. In the third image you can see the cost of 10 year money in the table on the left.

After South Australia (1.35% pa), NSW once again takes the cake for the highest cost of capital at a chunky 1.31% pa. Another question I've fielded is how much more do the states have to pay for funding than the federal government, which I guess is pretty topical given both are being asked to do a lot of heavy lifting on fiscal policy.

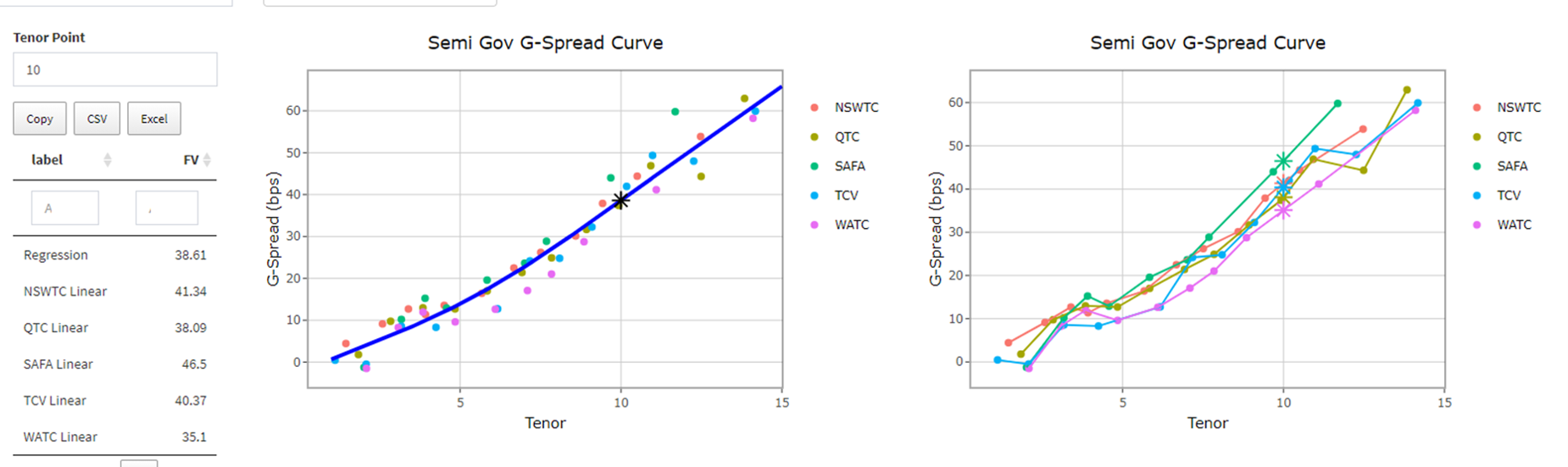

The fourth screenshot below answers this quantitatively by displaying the spread above government bond yields that the states have to service. While the table summarises the data, one can see the spread is fairly chunky: NSW, which again has the dearest cost of capital among the largest states, pays a spread of 0.41% pa above what the federal government has to pay.

The Reserve Bank of Australia's Governor Phil Lowe has put this issue on the table with his suggestion at National Cabinet that the states consider spending another $40 billion over the next two years to support the federal government's expansionary fiscal policy program. Governor Lowe delivered the same message in his parliamentary testimony, specifically citing the ability of the RBA to keep the states' cost of capital low:

To date, I think many of the state governments have been concerned about having extra measures because they want to preserve the low levels of debt and their credit ratings. I understand why they do that, but I think preserving the credit ratings is not particularly important; what's important is that we use the public balance sheet in a time of crisis to create jobs for people. From my perspective, creating jobs for people is much more important than preserving the credit ratings. I have no concerns at all about the state governments being able to borrow more money at low interest rates. The Reserve Bank is making sure that's the case. The priority for us is to create jobs, and the state governments have an important role there, and I think, over time, they can do more. But the federal government may be able to do more as well. We may need all shoulders to the wheel.

Westpac's Chief Economist, Bill Evans, highlights that in the latest RBA board minutes there were several revealing remarks about the states' spending programs, including the often overlooked point that the fiscal policy settings of the states are more important in demand terms than the federal government's policy posture on this front:

Another important change in the Board’s rhetoric is around the commitment to further purchases of government securities. For the first time in the “Considerations” section of the Minutes the Board note – “Members noted that public sector balance sheets in Australia were strong which allowed for the provision of continued support.” In the discussion on the domestic economy further support to the causes of the State and Territory governments was outlined, “Members noted that state and territory governments had played an important role in complementing income transfers …by increasing direct spending on goods and services and job creation….accounted for a larger share of public demand than the Australian government… debt levels relative to the size of the economy were low for Australian and state governments.” This indication of support for the state governments is clear even though the official policy target is restricted to the three year AGS...However it seems reasonably clear that the RBA is committed to supporting the semi government sector’s borrowing requirements as it encourages states to lift their spending. That will happen indirectly through the TFF and the wind down of the CLF, although I expect there will be a significant lift in direct purchases of semi’s by the RBA as we move into the next stages of the budget deficit funding processes.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

General Disclaimer:

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer:

This information may contain some forward-looking statements. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to rely on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment