The Quality Advantage in Small Cap Investing

Ian Carmichael

Fairlight Asset Management

A quality investing framework executed sensibly can earn returns in excess of the market. The benefits derived from a quality approach are magnified even further when investing in small caps. In defiance of conventional finance theory, earning this additional return doesn’t require taking on additional risk.

In the simplest sense quality companies are those that are highly profitable, growing and relatively safe. Over time a wealth of academic research has shown that excess returns have been historically available to investors in quality companies. The research has been robust to various definitions of quality and it hasn’t mattered whether you defined quality companies as those with high-profitability (Novy-Marx, 2012), low-beta/volatility (Black, 1972), low-leverage (Penman, 2007) or conservative accounting (Sloan 1996).

This is a somewhat surprising conclusion because it is not necessarily intuitive as to why investors should be rewarded for owning better businesses. Traditional finance models assume return is compensation for risk, but in the case of quality, investors are being rewarded for eschewing risk. Instead it appears that quality investors are rewarded for avoiding lottery tickets – those businesses with high-potential but low likelihood of success. While lottery tickets can occasionally produce spectacular short-term returns, as a group they represent a drag on returns.

This observation may not, at face value, appear to be overly helpful to investors who deal exclusively in large cap companies as the largest components of the S&P500 (Microsoft, Apple, Amazon, Alphabet, and Facebook) are all comfortably high-quality businesses. As you might expect it is very difficult to become a large cap company without exhibiting several quality characteristics. Regardless, despite the large proportion of high-quality businesses in the large cap universe, there has still been an excess return available to investors who focused exclusively on quality.

Small caps have a quality problem

Where quality investing does however get particularly interesting is at the smaller end of the market. Unlike the large cap universe where quality is the norm, small cap businesses are on average considerably lower quality. The small cap market is rife with broken business models, fallen angels, fads, and frauds. In this respect the historic outperformance of small caps over large caps is even more impressive when the difference in quality composition Is accounted for.

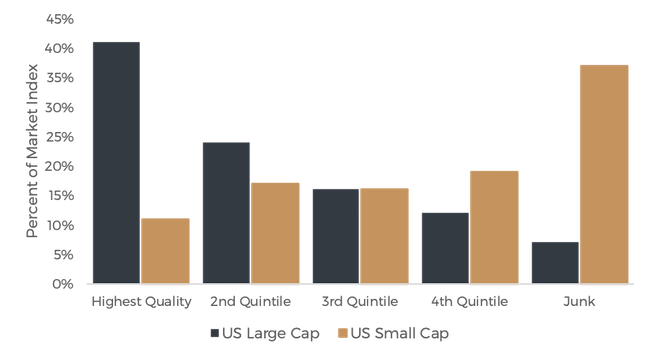

Figure 1 highlights the difference in the distribution of quality between the large cap and small cap universes. Over 40% of large cap companies can be considered high quality whilst only 10% of small cap companies can make a similar claim. Conversely less than 10% of the large cap universe is junk (unprofitable, high risk and speculative), whilst nearly 40% of small cap companies can be classified this way.

Source: Asness, et al., Size matters, if you control your junk, Journal of Finance Economics, 129 (2018).

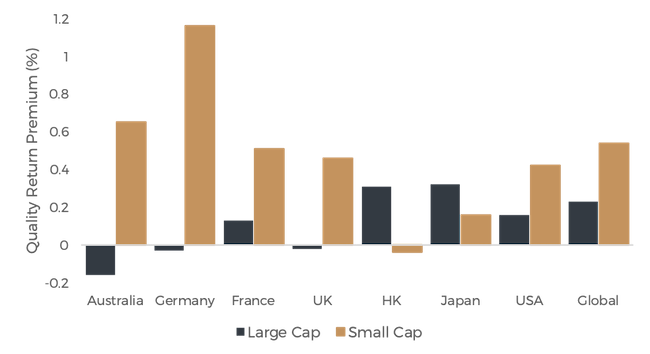

A direct consequence of the compositional difference between the large and small cap markets is that the benefits of investing with a quality approach are magnified when investing in small companies. Figure 2 shows that for most markets (Asia the exception), small cap investors have earnt a more significant premium from investing in quality than large-cap investors. Over the past three decades, the excess returns available in the global small cap market have been twice what has been available in global large cap.

Source: Asness, et al., Quality minus junk, Review of Accounting Studies, 24 (2019).

Quality investing reduces risk

Additional to the return-based argument, there is also a risk-based argument for taking a quality approach to small cap investing. The small cap market is more volatile than large cap as the businesses are typically less diversified by geography and industry, and the shares are less liquid which can amplify the share price reaction to any one piece of news. Quality companies are less sensitive to macroeconomic shocks, produce reliable cashflows, and have conservative balance sheets. As a result, they tend to outperform in difficult markets. Thus, a small cap portfolio assembled with a quality investing philosophy represents a defensive approach to a riskier market.

The Fairlight view

The historic data is clear that a quality investing framework executed sensibly can earn returns in excess of the market. The benefits derived from a quality approach are magnified even further when investing in small caps given the adverse composition of the market. In defiance of conventional finance theory, earning this additional return doesn’t require taking on additional risk.

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ian is partner and portfolio manager of the Fairlight Asset Management Global Small and Mid Cap Fund.

1 topic

Ian Carmichael

Portfolio Manager

Fairlight Asset Management

Ian is partner and portfolio manager of the Fairlight Asset Management Global Small and Mid Cap Fund.

Expertise

Ian Carmichael

Portfolio Manager

Fairlight Asset Management

Ian is partner and portfolio manager of the Fairlight Asset Management Global Small and Mid Cap Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment