The RBA has many more bullets to fire...

In the AFR today I write that markets are focused on what the Reserve Bank of Australia’s Governor Phil Lowe and Deputy Governor Guy Debelle decide regarding how they continue to support the economy at a time when there is large excess capacity in the labour market, double-dip recessions overseas, a full-blown trade war with our biggest export partner, and the prospect of fiscal policy detracting from growth (click on that link to read the full column). Except enclosed:

To put that labour market slack in context, wages growth in the September quarter was just 1.4 per cent over the year, the lowest since the index began in 1998 (and less than half the average 3.1 per cent pace since that inception date).

During this recession, Australia’s jobless rate jumped from 5.0 per cent to 7.5 per cent, noticeably much higher than the GFC peak of 5.9 per cent. Crucially, the lesson from the GFC was just how hard the RBA found it to get the economy back to full employment. In early 2008, the jobless rate was 4.0 per cent. After climbing to almost 6 per cent, the RBA has struggled for the last decade to get it below 5 per cent towards its “4 point something” estimate of the full employment rate at which wages growth increases more rapidly. In fact, Australia’s jobless rate has averaged 5.7 per cent since 2015.

Excess labour supply has driven correspondingly weak wage outcomes. Since 2015, workers have captured real pay increases of only 2.1 per cent annually compared to the 3.6 per cent average in the decade preceding the GFC. Weak wages growth is the key reason Martin Place has failed to hit its mandated 2 to 3 per cent inflation target since 2015. During this time core inflation has averaged 1.6 per cent, which explains why Lowe has reprioritised the RBA’s mission to focus on crushing the jobless rate back into that fully-employed zone.

While recent employment numbers are encouraging, Debelle’s view that the recovery will be “bumpy” has been vindicated. Care of deep lockdowns around the world, double-dip recessions are emerging in Europe and the UK while there has been a sharp deceleration in US activity. Locally we have had to contend with lockdowns in Sydney and Brisbane, and a full-blown trade war with China, which is hammering many sectors.

Finally, Martin Place knows that with the expiry of JobKeeper, the Morrison government’s massive fiscal stimulus program will start detracting from growth in the second half of 2021.

The challenge for monetary policy is that conventional tools are tapped out. The RBA’s main policy lever, the overnight cash rate, has hit its effective lower bound at 0.1 per cent. Two of its unconventional levers—the circa $200 billion Term Funding Facility (TFF) and the yield curve control policy that keeps the 3 year government bond yield at 0.1 per cent—have little runway left. The TFF is providing the banking system with more funding than it needs right now. And the RBA has effectively ruled-out negative rates.

The one policy the RBA has remaining that has enormous untapped capacity is its 5- to 10-year Commonwealth and State government bond purchase program, known as “quantitative easing” (QE). This seeks to reduce the yields, or interest rates, on Commonwealth and State government bonds to levels that are lower than they would otherwise be. In doing so, the RBA undermines the appeal of these assets to foreigners, prompting them to sell Aussie dollars, putting downward pressure on our exchange rate.

An exchange rate that is lower than it would otherwise be supports exporters and import-competing businesses, boosting incomes, household spending, labour demand, and economic growth. What this type of QE does not do is blow housing bubbles, because it is only influencing longer-term interest rates, which have little bearing on mortgage rates given most Australian borrowers have either variable-rate loans or short-term fixed-rate products.

One optical issue is that we cannot observe the “counter-factual”: that is, what yields and the dollar would look like in the absence of QE. Yet every investor on the planet agrees they would be higher, and hence growth lower, were it not for the RBA’s interventions. This is why when we survey economists at 11 banks, all are forecasting that the RBA will extend its $100 billion QE policy when it expires in April. Whereas six of these banks expect another $100 billion of bond purchases, five think it will be tapered somewhat. It's surprising none are projecting a larger program.

The problem is that the RBA is basically engaged in competitive QE vis-à-vis other central banks that are buying, relatively speaking, larger quantities of their own government bonds to reduce their public sector’s cost of capital and make their real exchange rates as cheap as possible.

The evidence to date is mixed on how the RBA has fared in this battle. One of the most important measures the RBA is using to assess its efficacy is Australia’s real effective exchange rate, which reflects our exchange rate weighted against key trading partners. This is almost 6 per cent higher than it was in December 2019 before the COVID crisis hit. It is about 2 per cent above its level in September 2020, prior to the RBA launching QE.

That does not mean the RBA has failed. Long-term interest rates and our exchange rate would be higher again were it not for its $100 billion of bond purchases. One illustration of this is the differential between the 10-year interest rates on our government bonds and those on US treasuries.

In mid September before the RBA signalled its interest in QE, our 10 year government bond yields were almost 19 basis points higher than their US equivalents. As a result of the RBA’s jaw-boning, that gap was crushed down to negative 2 basis points the day before the RBA announced the QE policy. (Today it is sitting at positive 2 basis points.)

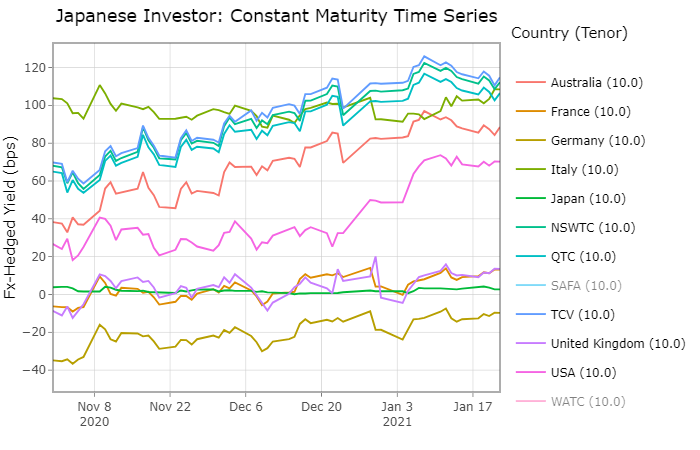

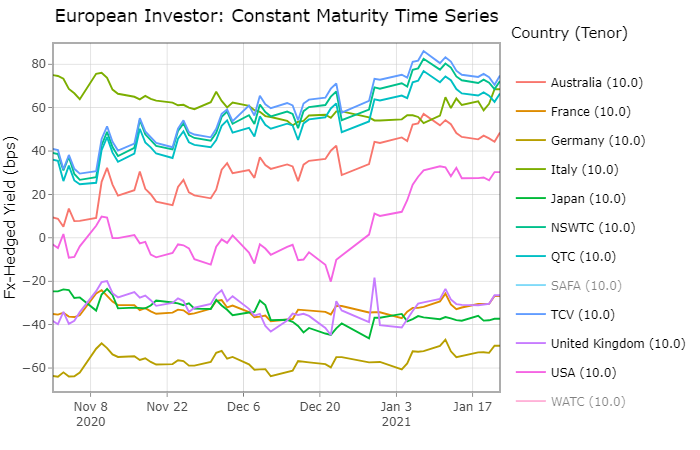

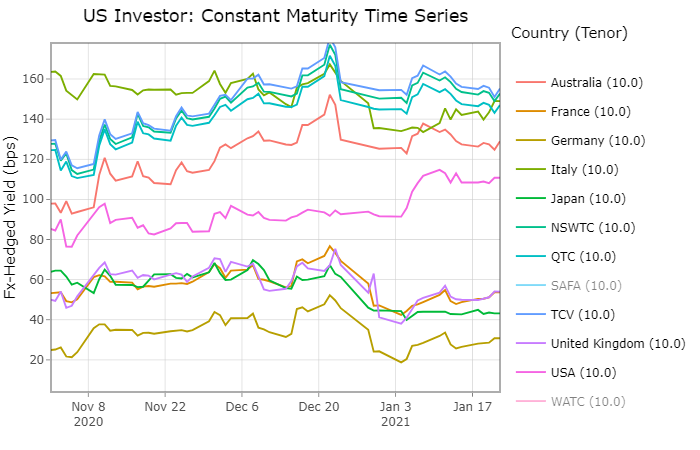

A third variable that, like the real exchange rate, hints the RBA has more heavy-lifting to do is the relative level of global bond yields hedged into different currencies. Because of our outstanding budget performance, Australia is one of the few AAA rated countries in the world. The State governments are typically rated AA to AAA, on par with or superior to nations like the US (AA+), UK (AA) and Japan (A+). And yet when hedged into US dollars, yen, euros, or Aussie dollars, Commonwealth and State government bond yields are above any other highly rated government bonds globally.

In fact, our AA and AAA rated State government bond yields are now better than those offered on BBB rated Italian government bonds, which are a popular higher-yielding sovereign asset for investors. This explains why Aussie bonds are sought after globally. During the week Victoria issued a 2025 bond that attracted a record $6.6 billion of demand, much of which came from foreigners.

The issue is that the balance between the supply of these bonds and demand for them is not sufficiently skewed towards the demand side to materially reduce yields, which is why it is hard to imagine Martin Place would want to crimp its QE program only six months after it has started.

(Enclosed are screen-shots from our internally-developed systems.)

Access our intellectual edge

Coolabah Capital Investments is a leading active fixed income manager, specialising in liquid, high grade credit. Our large investment team covering Sydney, Melbourne, and London is equipped with deep quantitative credit research capabilities. Click the ‘CONTACT’ button below to get in touch with us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment