The Riddle of The Reject Shop

Jeffrey Tse

Do you remember the first time you visited a dollar store? For me it was an exciting stop after school. My weekly pocket money felt like a fortune. I converted it into a Swiss army knife, a cap gun and an assortment of snacks. There are fewer genuine dollar stores today but the discount variety store concept is still around, mostly in the form of The Reject Shop (TRS).

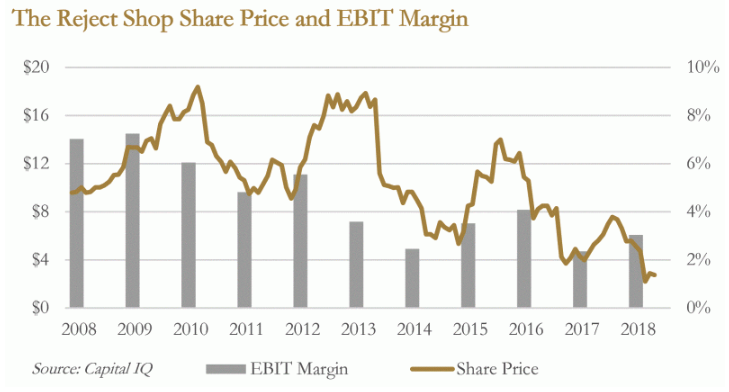

Its shareholders are now considering a cash takeover offer at $2.70 per share, valuing the business at not much more than its franking credits balance. Ten years ago shares changed hands for $10 each. Same store sales were growing at an average of 7.4% a year. Returns on equity were 50%. Where has The Reject Shop gone wrong?

American and Canadian Success Stories

Some international discount variety retailers have performed extremely well over that same period. Dollarama (TSE:DOL) operates a network of 1,192 stores throughout Canada. Same store sales grew at an average of 6% a year over the last decade and the business is valued at $12.6bn. To put that into perspective, the market values a Dollarama store at sixty times as much as a Reject Shop store.

Dollar Tree (NASDAQ:DLTR) and Dollar General (NYSE:DG) in the US have large and growing store networks of fifteen thousand each. Both grew same store sales at an average of 4-5% a year over the last decade. Together, these two businesses are worth a combined $81bn.

These examples demonstrate that the concept can thrive under the right conditions. But a closer look at their business models highlights the importance of clear price leadership and a unique customer proposition.

Dollarama has a much lower lease and wage cost base compared to The Reject Shop. It sources its products directly, cutting out the cost of the agent and providing control over product design. Its value merchandise seems to resonate with the customer base. Just look up “Dollarama haul” on Youtube and see if you can scroll through all the videos of people proudly showing off their newly purchased wares. The business spends nothing on advertising.

The US success stories also carved out positions as price leaders with a unique customer proposition. Dollar General focused on providing discount consumables to rural towns with populations too small to attract investment and competition from Walmart. Dollar Tree sells everything at a fixed $1 price point which has proven to be a compelling offering, even for middle to higher income consumers in urban and suburban areas.

The Riddle of The Reject Shop

The North American success stories provide market leading prices and a distinct shopping experience. The Reject Shop has been unable to execute as successfully despite numerous adjustments in strategy and leadership changes. Different store layouts, price points and merchandising mixes have been tested and failed.

But the number one problem is that its products simply aren’t that cheap. Most items are available at similar prices at Aldi, K-Mart, Target and even Coles and Woolworths. The treasure hunting experience is less satisfying without the payoff of a striking bargain.

Parallel importing of branded fast moving consumer goods could be the last vestiges of The Reject Shop’s competitive advantage. Rather than purchasing directly from the manufacturers, it procures indirectly from an agent based in another country. This avoids the discriminatory pricing applied to Australian retailers such as Coles and Woolworths.

Will The Reject Shop still be around in 10 years’ time?

Still, $800m of revenues is nothing to sneeze at. It’s still the first place I go whenever I need a last minute Halloween or Christmas accessory and $2 is a great price point for a tub of Pringles.

At its core, The Reject Shop has a unique proposition to work with and experiences internationally demonstrate that the discount variety retail concept can thrive under the right conditions. But plenty of discount variety retailers have gone bust.

For The Reject Shop to survive if competition continues to whittle away at its value proposition, it may need to shrink or relocate stores away from large discount grocers and discount department stores. This will be difficult with $296m of operating lease commitments. A small decline in sales can easily wipe out profits given the large fixed cost base.

For The Reject Shop to thrive, a more significant transformation would have to take place. There may be an optimal merchandising, pricing and layout strategy that management have yet to figure out.

Shareholders, though, don’t have the luxury of time. They have to choose between a certain but lowly $2.70 now, or a turnaround strategy that might never come. I’ll keep dreaming about the good ole’ days.

Forager Funds does not own shares in The Reject Shop.

Further insight

If you are interested in receiving the Forager monthly and quarterly reports, please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Jeffrey Tse,