The risks are elevated this reporting season

Reporting season is upon us and as always, it presents another level of risk - but also opportunity. We think risk is more elevated this reporting season given the high valuation of the market and some of the sectors / stocks within it. If you’re a company with a very high multiple that misses expectations this reporting season, you’ll be savaged. Below are the reporting dates for stocks in our portfolio and consensus estimates for most holdings. We think the stocks within our portfolio will be okay, and some may even surprise to the upside. Suncorp (SUN) and CSR (CSR) would be candidates here. If we do see companies we hold miss expectations, we’ll be swift to make a call. As always, SMS & email alerts will provide timely information here.

Nicholas Forsyth

Market Matters

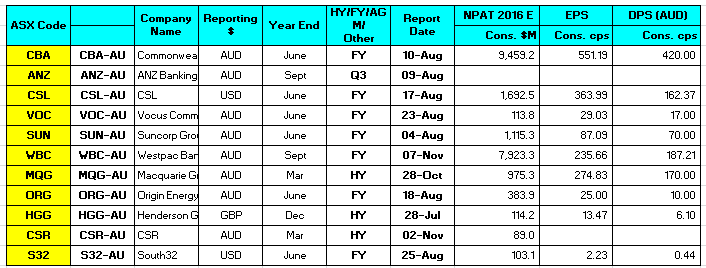

Table of current portfolio holdings – reporting dates + earnings estimates. (Please note, we purchased Independence Group (IGO) yesterday morning and is not covered here)

Our view on key sectors with specific reference to the stocks we currently own.

Banks; We have CBA, WBC & ANZ in the portfolio, probably one bank too many however we think share prices will tick higher in line with the broader market. At higher levels, we will look to trim our exposure, specifically with Westpac (WBC) if it trades over $32. Most of the focus this reporting season will be on capital & margins. The current environment remains tough for the banks, with low-interest rates and increased competition resulting in some margin pressure. Capital uncertainty continues to be a key negative for the sector, and unlikely to be a clear outcome until late CY16 or early CY17. If the banks can reprice their loan books, then margin pressure will be minimal. However, we’re not seeing signs of this yet (maybe August if we get a rate cut of 25bp banks may pass on 15/20bp).

Not a lot to like about the current operating environment for the banks, however, it seems to be in the price. Banks trade on 12.2 times v a market which trades on 16.4 times – so cheap in relative terms. Of course, there’s the argument that the market is expensive, which has merit relative to history however that can be countered by sighting low-interest rate – so it’s cheap on that metric. We prefer the latter view simply because the relevance of financial conditions now has a bigger bearing than historical measures do.

Resources; We have South 32 (S32) in the portfolio now and in the last few months we’ve also had Fortescue (FMG) and Regis Resources (RRL). Clearly, resources are back in favour, and we’re seeing money flow into the miners on the back of rejuvenated optimism. To be clear, we like the sector and will continue to look for opportunities to increase our exposure to it in the short term. We’ve written a lot about resources and their high correlation to emerging markets; we like emerging markets thus we like resources and vice versa. The main reason is simply that both resources & emerging markets have already undergone deep adjustment caused by external forces (capital flow/supply/demand etc.in) and are now coming out the other side. Compare that to what we see in developed economies where that adjustment simply has not happened, and it’s easy to be more optimistic on emerging market growth.

For example, (and as highlighted in a recent strategy piece by Morgan Stanley) Emerging Markets have had to adapt to an environment of collapsing commodity prices, USD strength and a tightening in financial conditions which spurred substantial capital outflows, sharp depreciation in EM currencies, accelerating inflation and a tightening in domestic monetary policy. When economies/stocks/sectors or even individuals stare down the abys, we often see major structural changes emerge that sets a better foundation for whatever happens in the future.

Looking at resource companies, they too have had to deal with an environment of weak demand, collapsing commodity prices, USD strength (which puts pressure on commodity prices), highly geared balance sheets in many instances and to top things off, a market that has been fixated with yield in a low interest rate environment which has forced dividends to stay unsustainably high until recently (think BHP + RIO’s progressive dividend policy).

In that hostile environment, miners have been forced to reduce CapEx, strip every conceivable cost from their business, de-lever their balance sheets and operate as efficiently as they possibly could. In short, the tough period has been a massive wake-up call for the sector (as was the case with many emerging markets). We now have a better operating environment, and we’re seeing miners generating significant free cash flow (FCF) courtesy of commodity and currency tailwinds since early 2016. The sector is now remarkably unleveraged, with >60% of major mining companies (S&P200) having NO debt and net cash, and of the companies that are indebted – BHP, RIO, NCM, FMG, AWC, WHC, IGO – all have identifiable and plausible pathways to retire debt. Interestingly, recent moves in commodity prices have underpinned significant FCF (FMG could be debt free in ~2 -3 years at current spot iron ore price) could reduce this list to just 2-3 names within a couple of years.

Telco’s; We have Vocus Communications (VOC) in the portfolio, and now have very little interest in Telstra (TLS) after trading it earlier in the year. We see VOCs recent acquisition with NextGen as positive, increasing the quality of VOC and extending its growth profile. Following a Q4 trading update on June 29th, we expect few surprises at the result on the 23rd of August. Core VOC business continues to grow very strongly at ~20% and believe it can close some of the valuation gap with TPG which is trading at 22x 2018 earnings versus VOC on 16.5x.

TLS looks less appealing despite their strong positon in the Telco market. In the post-NBN world they lose much of their competitive advantage (being better network coverage), and will therefore struggle to retain their premium pricing model – margins will come under pressure. Furthermore, they lose $2-3bn in earnings from the nationalization of their network and although they were/will be compensated handsomely, they still need to replace that ongoing earnings stream. On a macro level, TLS has being supported by the yield trade, with low-interest rates globally inflating asset prices. As interest rates rise, we think Telstra comes under added pressure.

Register now for 14 days free access to our Platinum level membership and to discover the 3 stocks we’re buying today: (VIEW LINK)

Energy; We have Origin Energy (ORG) in the portfolio targeting $6.20 and have traded Oil Search (OSH) in recent months. We like the sector and see Oil tracking higher in the months ahead – towards $US60. Origin Energy (ORG) is a more complicated story than most and will release their 4th quarter production report and reserves today (29th July ) before reporting full-year numbers on the 18th August. The energy markets business is performing well – similar to AGL with higher electricity prices translating to higher earnings. Look for guidance around debt, their dividend (which could be cut) and importantly commentary on APLNG train 2.

Insurance & Diversified Financials; We have Suncorp (SUN) in the portfolio and have often written about QBE Insurance (QBE) under $10 (however having two insurance companies we feel is too much). Most of the insurance companies report in August. and we’re comfortable with the markets expectations for Suncorp. The key for this stock over the next few years is to lift it’s insurance margin back to 12% - which should be achievable despite difficult operating conditions. Suncorp remains cheap trading nearer 13 times v IAG which is on 16 times. The valuation gap is a result of SUN’s banking division, so any commentary on a potential spin off there would be taken favourably by the market. Furthermore, we’ll be watching for any indication of insurance cycle turning and premium rates increasing.

In terms of diversified financials, we have Henderson Group (HGG) and Macquarie (MQG) in the portfolio. Henderson reported overnight and the result in terms of earnings was lower than expectations – largely a result of weaker than expected management fees and performance fees however these were largely offset by lower costs. Interestingly + pleasingly, 2Q institutional flows were positive and the CEO made some reasonable commentary, saying ‘the impact of the surprise BREXIT will only last a few quarters’. The result in terms of profit was a miss, but not huge and the stock has been sold down a long way since BREXIT.

Macquarie reconfirmed FY17 guidance at their AGM yesterday – the stock moved higher on the news. FY17 will continue to be a tough year for this area of the market and we think exposure should be kept reasonably low. MQG is cheap in an expensive market and now generates 70% of their earnings from annuity style income, rather than transactional based business – which makes earnings less volatile. More broadly for the funds management sector, flows and performance fees are pretty much known for the stocks prior to results, so the scope for earnings surprise lies mostly on the margin and cost sides. Most managers are facing fee margin compression as the larger industry funds continue to use their scale and buying power to lower fees across the industry.

Healthcare; We hold CSL in the portfolio and have recently sold out of Healthscope (HSO). We have discussed Ramsay Healthcare (RHC) many times and unfortunately missed a very good trade in RHC recently. These companies have a tendency to beat market expectations around earnings season and we continue to like all three, however they’re very expensive. Should CSL report good numbers we’ll look to exit our position in the mid $120’s. RHC and HSO can be bought on any reasonable pullback however if the market continues to rally, healthcare will underperform in a general sense. Although we have no exposure here, the Aged Care sector is interesting and looks to be bottoming after a poor year. The key issue for the sector centres on funding after govt changes to the aged care funding instrument (ACFI). Answers to this at the reporting season are unlikely given the political factors that still have to play out, however, there will be some discussion

Technology; We recently sold Seek (SEK) and the stock has since moved higher. We think the underlying business is starting to lose some momentum and although this is being offset by EPS accretive acquisitions, that trend makes us wary. The other stock we like in the sector is REA Group (REA) however both are trading on their highest multiples in two years (REA – 38x, SEK – 31x). and both REA and SEK have suffered sell offs through their two previous full year results. Both stocks have outperformed since the half year results season in February 2016 without any significant company updates to the market that have caused upgraded forecasts. They remain impressive businesses and are forecasted to grow at double-digits again for FY17 pre results, which continues to show their resilience in a low growth market. However, this growth comes at a cost to investors and due to the lack of earnings updates through the 2H16 we think caution is warranted.

Property; We do not hold property stocks in the portfolio at this juncture although concede the sector has performed very well over the past 12 months. Earnings are fairly predictable and the yield offered by the sector was very attractive, however the sector is trading at a 50%+ premium to last stated net tangible assets (NTA), and its forecast FY17 DPS yield of 4.4% represents just a 2.44% premium over the 10 year bond. We think property values are high and the sector is at risk as interest rates (eventually) start to rise. Most focus during reporting season will be on the residential developers like ABP, LLC, MGR and SGP – specifically in terms of settlement volumes, prices, margins, pre-sales and exposure to “the foreign buyer”.

Infrastructure/Industrials; We think ‘bond like’ infrastructure stocks are now too expensive and are at risk of decline when interest rates start to rise. We may be early on this call, however, we think the market will start to price any interest rate increase (globally) ahead of time. We have building products company CSR in the portfolio and are comfortable with this exposure for now. This stock is cheap relative to the sector and we think the market is too negative on earnings expectations. This stock could surprise to the upside in our view.

Register now for 14 days free access to our Platinum level membership and to discover the 3 stocks we’re buying today: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self Managed Super Fund (SMSF). As a member, you will receive twice daily and weekly trading and investment advice focusing primarily on ASX equity investments. Additionally, we share his market positions and provide an ongoing outlook on key stocks and markets that matter. We provide clear share trading and investment buy and sell recommendations with the clear aim of outperforming the market. https://marketmatters.com.au/

1 topic

9 stocks mentioned

Nicholas Forsyth

Director

Market Matters

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self...

Expertise

No areas of expertise

Nicholas Forsyth

Director

Market Matters

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment