The secret of sound investment in three words

People familiar with the teachings of Warren Buffett may be unaware of his mentor, Benjamin Graham (1894-1976). Buffett attributes a significant part of his investment success to the lessons he learned from his friend and mentor.

In fact, many professional investors still refer to him as the father of value investing. His two best-known books are the investment classics Security Analysis (1934) and The Intelligent Investor (1949).

Ben Graham’s insights into investment decisions were unprecedented at the time, but they reflect the breadth of his interests and strength of his intellect. He was an interesting man, having graduated from Columbia University in 1914 at the age of 20 with the offer of teaching positions in three different faculties – Greek and Roman Philosophy, English and Mathematics.

He chose instead to head to Wall Street seeking income to support his family. He returned to Columbia to teach in their business school, where he guided several significant investors to stellar careers, including Buffett.

He maintained an interest in the classics, and was said to enjoy a regular pastime of translating the works of Virgil from Latin to Greek and the works of Homer from Greek to Latin. He spent his final years in the idyllic south of France, where he died in 1976.

The secret of sound investment in three words

As Graham notes in Chapter 20 of The Intelligent Investor,

“Confronted with a challenge to distill the secret of sound investment into three words, we venture the motto, MARGIN OF SAFETY”

Graham discusses the concept of the margin of safety as it relates to investing in shares aka ordinary common stock.

“In the ordinary common stock, bought for investment under normal conditions, the margin of safety lies in an expected earning power considerably above the going rate for bonds.”

He thinks of the margin of safety being the excess earning power of a stock over its holding period above a 10-year government bond. The expected earning power is derived by taking the inverse of the price to earnings multiple. For example, a stock trading on a price to earnings ratio of 10x has an earnings yield of 10% i.e. 1 divided by 10.

“Over a ten year period, the typical excess of stock earning power over bond interest may aggregate 50% of the price paid. This is sufficient to provide a very real margin of safety, which, under favourable conditions, will prevent or minimise a loss.”

What would Ben Graham be buying today?

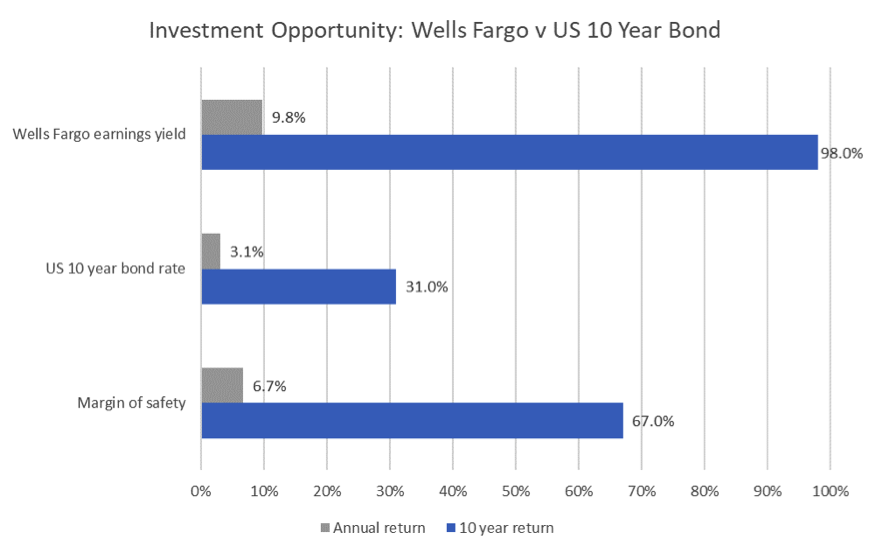

Let’s consider the application of this principle in the context of current market conditions. The current US 10 year bond rate is 3.1%. If you held the 10-year bond from today to maturity, you would receive a return of 31% i.e. 3.1% x 10 years.

Now, consider the return on common stocks. We have selected a large US bank, Wells Fargo, to illustrate this concept. Wells Fargo currently trades on a price to earnings multiple of 10.2x next years earnings. This means Wells Fargo will return 98% over the next 10 years (9.8% earnings yield x 10 years) even if its earnings failed to improve over this time horizon. This equates to a margin of safety of 67% over a 10 year US government bond (98% less 31%).

If you are investing for the long term, the question you must ask is this: do I want to own a high-quality US bank such as Wells Fargo for 10 years earning 10% per annum, or do I want to own a 10 year US government bond till maturity earning 3% per annum?

Despite the US economic recovery being late in the cycle, a 10-year investment would be more prudently applied to the purchase of Wells Fargo over the 10-year US government bond. The margin of safety is a whopping 67% (98%-31%), and a dilemma in the short term becomes a no-brainer in the long-term. It is unsurprising to have seen Buffett add to his US bank stocks during October’s market turmoil. He presumably still applies Graham’s lessons.

Investing is more successful when we think about it over the long-term as it allows for more rational decisions. It may mean we buy too early, but if we focus on the long-term, we will do well in the long term, and can choose to ignore short-term market movements which are unknowable.

If you haven’t delved into Graham’s work, I recommend adding The Intelligent Investor to your holiday reading list. It’s sold more than a million copies since first published in 1949 and remains the benchmark for value investing principles for anyone keen to profit from shares.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Lachlan is the founder and CIO of Swell Asset Management, a boutique investment manager specialising in global equities.

4 topics

Lachlan is the founder and CIO of Swell Asset Management, a boutique investment manager specialising in global equities.

Expertise

Lachlan is the founder and CIO of Swell Asset Management, a boutique investment manager specialising in global equities.

Expertise

Comments

Comments

Sign In or Join Free to comment