The uncertain road ahead for residential property

Given some recent potential headwinds, Livewire recently reached out for my thoughts on the residential property market, specifically what new drivers have emerged, what their implications are, and what data investors should be keeping a close watch on.

What recent event could have the biggest implications in property?

By far the most stirring news in recent weeks has been the announcement by APRA of a new 'speed limit' on interest-only mortgages in Australia, with the regulator now aiming to limit the flow of new interest-only loans to 30 per cent of total new residential mortgage lending.

Although the share of interest-only loans had already pulled back from the astonishing 2015 peak, in aggregate lenders will need to tighten up further to meet the proposed cap, while strict internal limits will be required for interest-only loans at loan-to-value ratios (LVRs) of above 80 per cent.

Henceforth, new owner-occupiers wanting to use this type of loan product may be given their marching orders, and possibly aged borrowers too.

Some Australian banks have been rolling over interest-only loans quite effortlessly at the end of the interest-only period, and these lenders will almost certainly now require a far more stringent assessment, while some investors may be offered incentives to switch to principal and interest mortgages.

The Federal Budget papers also proposed some unwelcome changes for landlords, with the Government limiting plant and equipment depreciation deductions to only those expenses directly incurred by investors, while travel costs will also be disallowed prospectively. These may prove to be sound measures which improve the integrity of negative gearing claims.

In an environment where both wages and rental price growth are tracking at multi-year lows, diminished after-tax cash flows could prune the investor segment of the market at the margin.

What are some of the potential implications for investors and the wider economy?

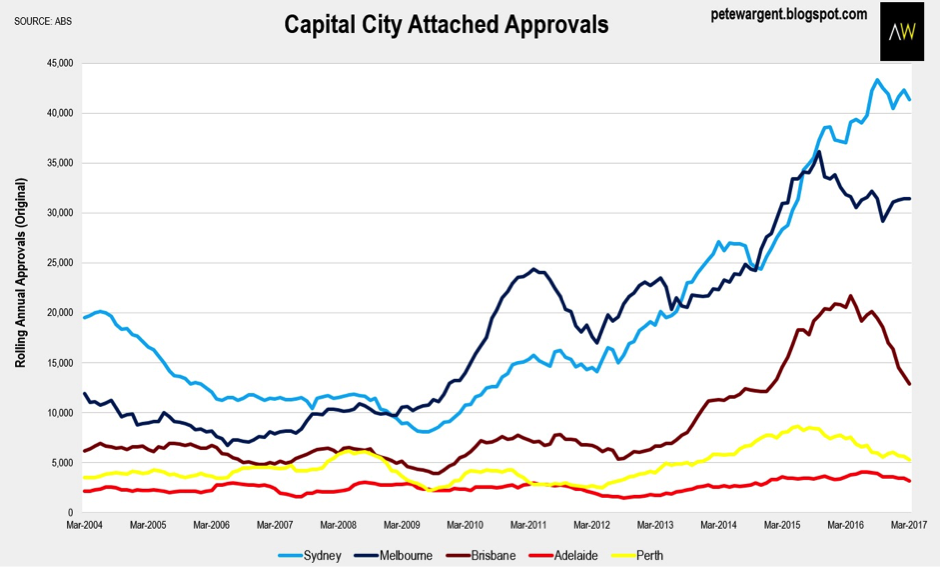

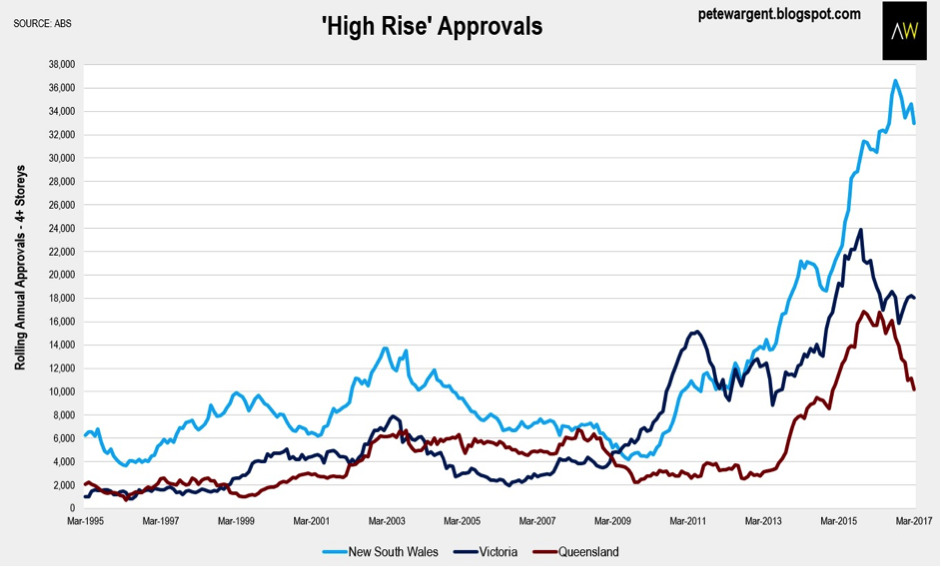

We have been reporting to our subscription clients over the past year that the sharp downturn in Brisbane unit approvals foreshadows a correction in prices and rents in the Queensland capital’s inner-city apartment market.

Indeed, nationally high-rise apartment approvals have at last turned down sharply from blistering heights, indicating that the residential construction boom has peaked.

Reserve Bank estimates have gauged that residential building accounts for about three quarters of employment within Australia’s massive construction industry. Given that residential building permits could yet fall by a quarter from their current levels the impact of the looming downturn could be significant, particularly after accounting for the known multiplier effect of residential construction.

Our research suggests that the winding down of construction activity could ultimately see cyclical businesses across a range of sectors come under pressure, including apartment developers, materials companies, some banks, real estate agencies, mortgage brokers, and retailers of household hardware and goods.

What do investors need to watch for in coming months, and why?

As noted, market participants should continue to survey changes to lending criteria and mortgage rates over the months ahead.

In the property investment sphere, it has also been fascinating to note that vacancy rates - reported here as online rental listings advertised for three weeks or more compared to the total number of established rental properties - have remained remarkably tight in Sydney and Melbourne, even at this advanced stage of the construction cycle when record new supply is being delivered.

In part this reflects that the rate of net overseas migration into Australia has quietly accelerated to its highest level in four years, with Sydney and Melbourne attracting the bulk of new settlers, while at the same time record numbers of international students are crowding into these respective inner-city hubs.

Apartment vacancy rates will be a trend to watch closely across H2 2017 as developers chew their way through the enormous construction pipeline. With Melbourne also attracting migrants from interstate, against the odds demand from searing population growth is outpacing supply, in turn forcing vacancy rates to half-decade lows.

If vacancy rates in the two most populous capital cities remain contained as the year progresses, then the recent moves to curb investor activity could even result in the return of rental price growth in 2018-19. Brisbane’s median apartment rents are already fading, however, and our on-the-ground experience suggests that declines are likely to continue doing so for some time to come.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of AllenWargent Property Buyers - "the better way to buy property".

Veteran property market analyst & investor.

1 topic

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Comments

Comments

Sign In or Join Free to comment