The Value Case for Uber Technologies

“I have no way to value it and neither does Steve because they need to increase prices to have a sustainable (presumably smaller) business … I just see that y’all are long garbage like that and [Forager is] plainly uninvestable for me unless you get your act together.”

That’s one investor’s feedback on our recent investment in Uber. He isn’t alone. We’ve never had a more visceral response to a new portfolio addition.

Uber is not the first unprofitable company we’ve invested in. In fact, some of our International Fund’s most successful stocks, Lotto24, Bonheur, Blancco Technologies and Betfair were loss-making at the time of investment. But Uber seems to be the most controversial.

Perhaps that is part of the opportunity. But I’ll come to that at the end.

The aim of this blog is to raise and address some of the key questions. And get some considered feedback (I’m guessing there will be plenty of feedback, considered or not).

Here are my answers to the main issues people have with the investment.

Issue 1: This business shouldn’t even exist. People only use it because it is cheap. The service is only cheap because Uber subsidises it.

Forget about all the economic rationale Uber puts forward for its existence. There might be some benefits to utilising a car fleet that is mostly idle. There are definitely benefits to a workforce that can flex depending on demand, as anyone who has tried to get a cab home on New Year’s Eve can attest. But these are not the main reasons ridesharing has a place in the world.

The ridesharing segment exists for two reasons.

One is regulatory arbitrage. Prior to the arrival of Uber in Sydney, a set of taxi plates cost as much as $400,000 to buy. That’s a lot of money for two small pieces of aluminium. They were worth so much because their supply was constrained by the NSW government and the pricing of taxi rides artificially inflated.

For a driver who wanted to lease some taxi plates, the going rate was $300 a week (roughly a 4% annual return for the plate owner). So before worrying about fuel, depreciation, Cabcharge’s take, insurance and the like, a driver had to earn $300 in fares just to cover the economic rent.

Along comes ridesharing and says “how about we split this $300 between customers (lower prices), drivers and the booking platform?” Wherever supply of taxi plates is constrained (everywhere, basically), you can offer lower fares and still make a profit.

The second is because it is a better service. I’m guessing you’ve had the same taxi experiences as me. Bookings that don’t turn up. Drivers that don’t know the way. Drivers that do know the way but intentionally take you the long way around. Drivers that won’t take you at all because it’s a busy night and the fare isn’t long enough. Cars that stink and rattle.

I’ve had the odd bad experience with Uber, too. But they are few and far between. For the most part, from booking to leaving the car, the experience is seamless.

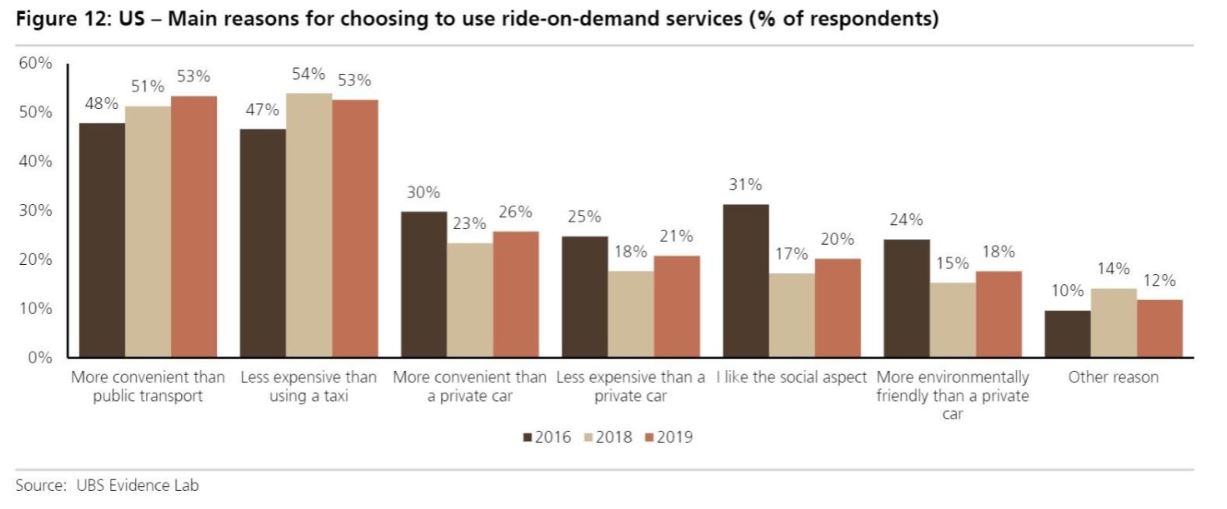

According to a recent UBS survey, only half of users cite cost as the main reason for using a ridesharing service:

Convenience matters, a lot. With the recent addition of government charges, it is hardly cheaper for me to use Uber relative to a cab. I do it because I prefer it.

More than 100 million different people used an Uber service in the last quarter of 2019, suggesting I’m not the only one who values it.

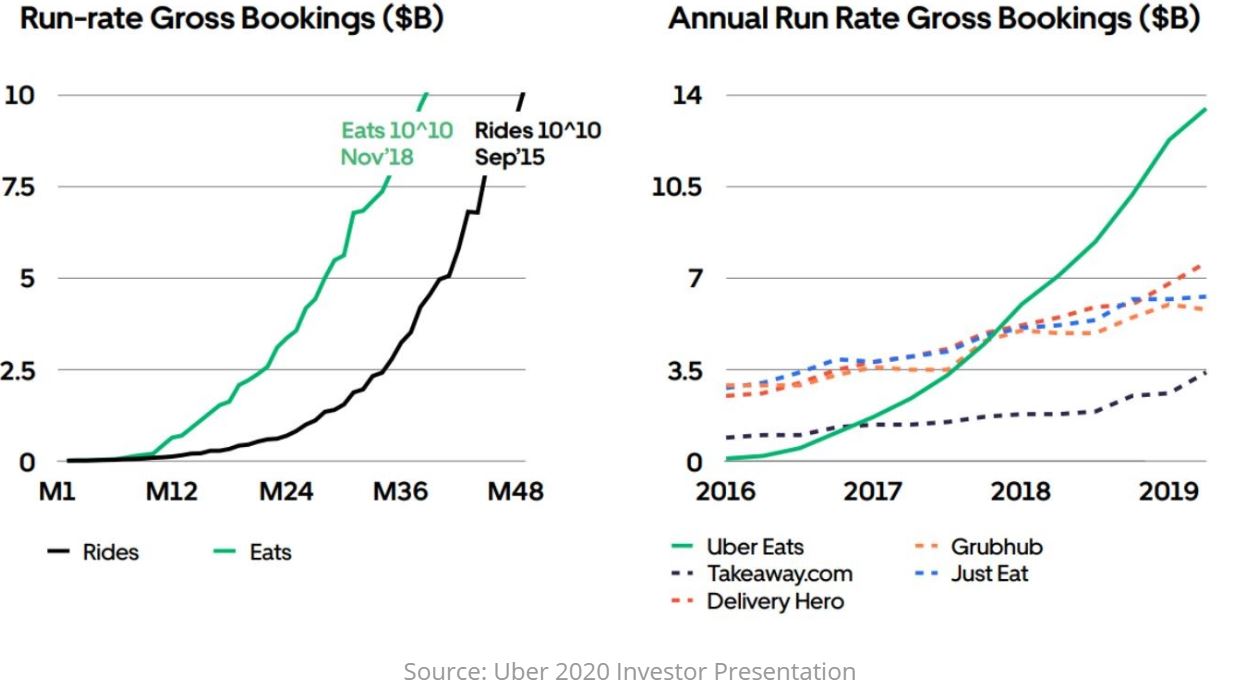

Issue 2: There are no barriers to entry. A constant stream of new competitors means Uber is always losing money.

It’s true. Pay a driver enough and they will put your app on their phone and a sign in the back window. Offer free rides and you will undoubtedly get a few users to try your new ridesharing service. That bit is not difficult. But this is a scale game.

Very small differences in UI and UX (user interface and user experience) matter immensely … if you are 0.5% better, that can be the foundation of hundreds of billions of dollars in market value.

– Gavin Baker on the Invest Like the Best Podcast

To offer a competing service, you need the same infrastructure as the large, established player. You need an app that is at least as good. Useability is hugely underrated, difficult and only noticed when it is bad. You need the same number of drivers, so that there is always availability. You need marketing, distribution and customer services teams.

If one participant can reach a dominant market share, they are almost impossible to dislodge. With roughly similar overheads, the largest player makes more money (or loses less) at every single pricing level.

That’s why every city ended up with one highly profitable newspaper in the twentieth century. It’s why Virgin Australia could never make a profit. And it’s why Uber’s competitor Lyft, with roughly one third of the ridesharing market, is struggling in the US.

It’s also why the competition is so ferocious in the early years. Everyone knows that only the largest player is going to make money at maturity, so they are willing to spend a fortune trying to get there.

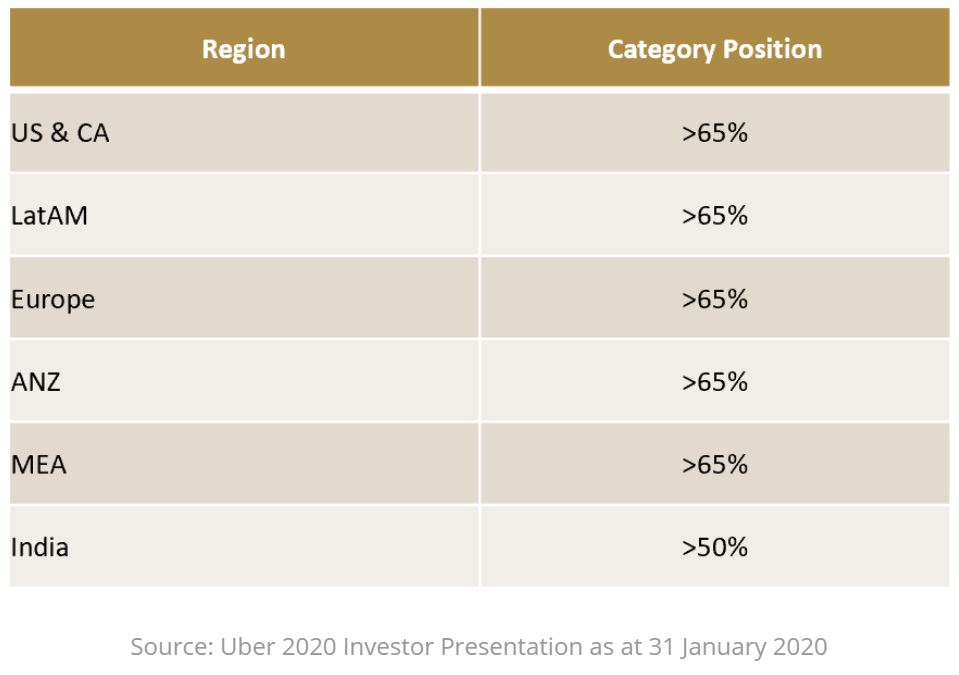

It’s a fight that Uber has won in most of the western world.

Having withdrawn from expensive forays into Asia, Uber is now number one in every market that it operates in, with market shares higher than 65%. Trying to dislodge them now is pointless, and that’s why you are seeing a lot fewer companies try.

Issue 3: They are just going to waste money on hare-brained schemes like driverless cars.

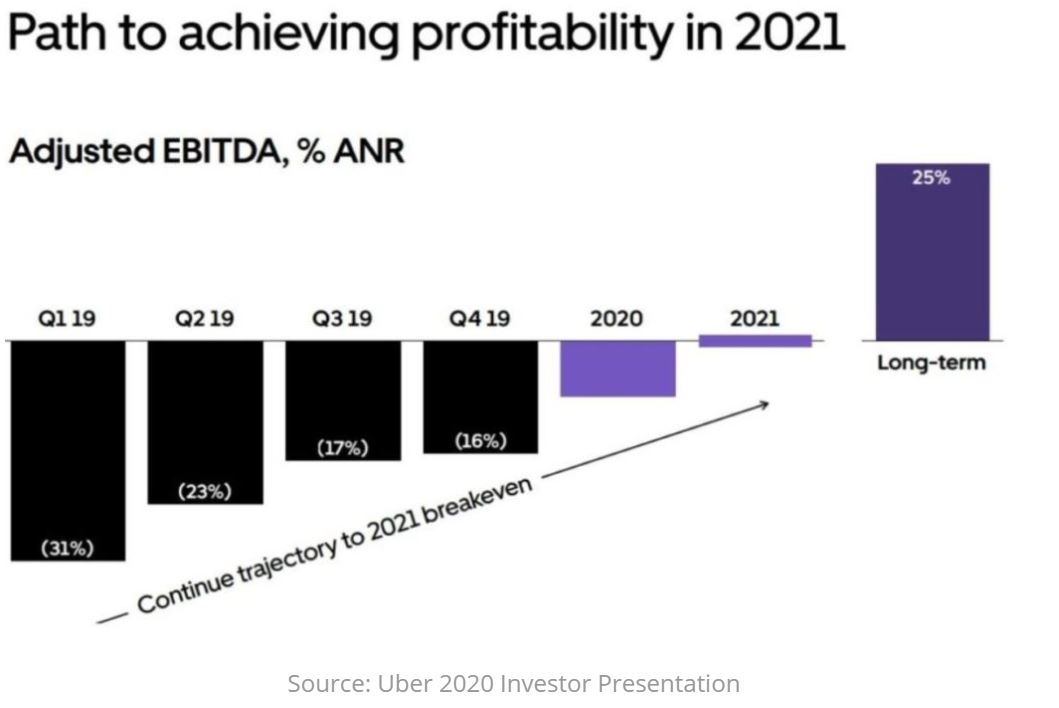

This is going to surprise quite a few people. Uber’s ridesharing business (Rides) is already profitable. And not just a little bit. It contributed $742m of EBITDA (earnings before interest, tax, depreciation and amortisation) in the December 2019 quarter, almost four times the $195m it made in the same period the previous year.

Yes, there is $644m in corporate expense. And there’s another $350m of operating expenses that come underneath the EBITDA line. But the profitability of Rides was growing fast prior to COVID-19. It will resume growing fast once the world economy starts to recover. The business as a whole was expected to break even at the EBITDA level in 2020, thanks to significantly reduced losses in its Eats business (see below).

This is not the Uber of old. It is not the Uber most people think it is.

Uber was founded by, Travis Kalanick. Uber would not be what it is without him. First mover advantage was crucial and his single-minded vision of global domination meant that it was Uber, not one of its many copycats, that ended up dominating most Western markets.

Backed by seemingly unlimited funds from Softbank’s Masayoshi Son, Kalanick’s ego became a significant liability from 2016 on. His attempts to dominate eastern markets and build driverless cars were costing a fortune. His disrespect for drivers, customers and anyone else who crossed him was a giant public relations disaster.

It was the middle of winter of 2017, and Jeff Jones, the man responsible for Uber’s public perception, was trying to shake everyone in the top ranks of the company awake. Uber didn’t have an image problem. Uber had a Travis problem.

– Super Pumped: The Battle for Uber by Mike Isaac

You might not have read much about Uber lately. I doubt many would be able to cite its CEO’s first name, let alone his surname. That’s a good thing.

Kalanick has been out the door since August 2017. Masayoshi has his tail between his legs after the meltdown of his futuristic Vision Fund.

Uber’s other shareholders were fed up with the damage Kalanick was doing to their investment and appointed Dara Khosrowshahi to point the company on a path to profitability and respectability.

Dara has been delivering. Uber has exited markets where it doesn’t see a clear path to being the number one player. In most cases, that has been in exchange for a significant percentage of the remaining dominant player. Today the company owns stakes in market leading regional players such as Didi (China), Grab (South East Asia), Zomato (India) and Yandex (Russia). Uber recently announced a COVID-19 related writedown of these investments, but still pegs their collective value at more than $10bn.

He has worked tirelessly to improve the company’s public reputation and relationship with drivers, introducing tips for drivers (something Kalanick refused to budge on) and working on new legislation to provide drivers and passengers more protection. The more this industry is regulated, the higher the barriers to entry.

The path to profitability and beyond has been clearly, transparently and consistently presented to investors.

The last remaining significant impediment to profitability is its food delivery business, UberEats. Progress has been highly encouraging.

The South Korean and Indian food delivery landscapes have already rationalised over recent months, thanks to Uber’s sale to Zomato. The Indian business alone was costing Uber $350m of annual losses. Its sale was the reason for EBITDA breakeven being brought forward by one year to the end of 2020 (prior to the impact of COVID-19).

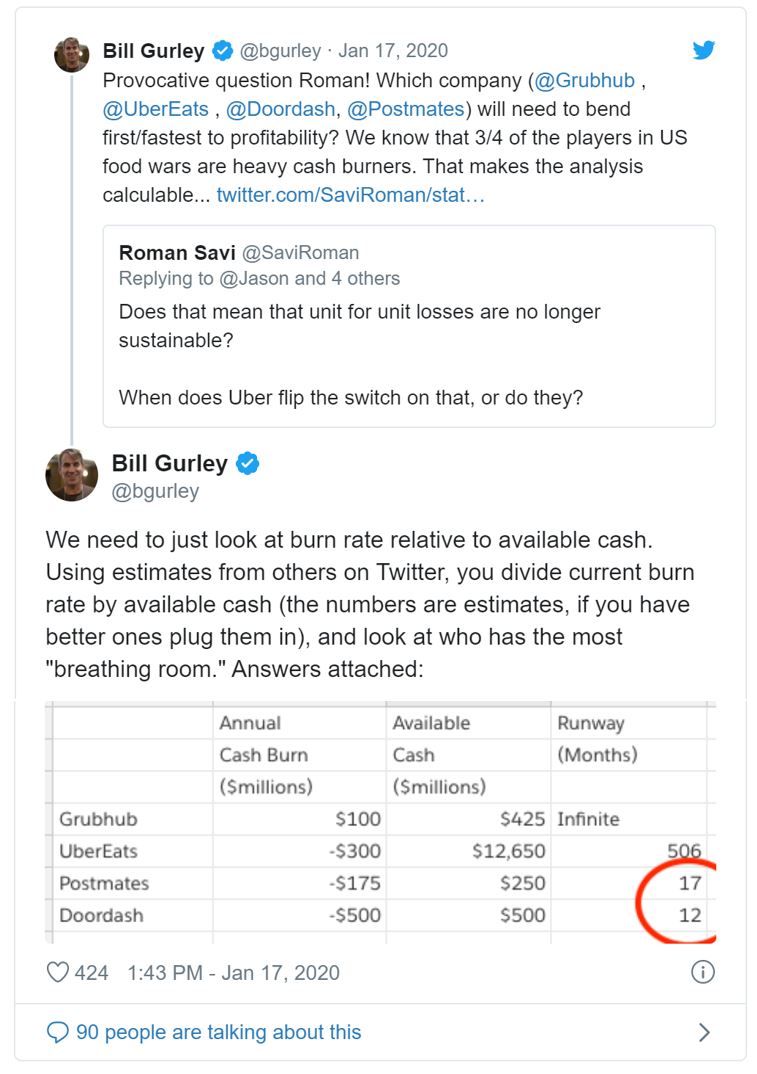

UberEats’ key market is the US where there are four large players and consolidation is likely, perhaps even accelerated by the current environment. Two of the four (Postmates and DoorDash) are private. Postmates has attempted to IPO twice, unsuccessfully, and there is a clear urgency to sell or merge given it is a sub-scale player in a highly competitive, cash-burning market.

DoorDash has been aggressively using discounting to drive growth, all funded by cheap venture capital money. The company had raised a total of $2bn through December 2019 and lost $450m of EBITDA in 2019. Estimates suggest that Doordash is likely to have at most $550-650m of cash as of the start of 2020 and, given the COVID-19 situation, they are likely to be forced to merge or raise further capital at a discount and attempt to become more price rational.

In January 2020 GrubHub said they are considering alternative strategies including a possible sale of the business amid increasing competition and continued share loss to the likes of Uber.

This theme is unfolding the same way in other key markets around the world. And when the war ends, industry profitability changes dramatically. China’s Meituan went from losing $200m per quarter to making $300m per quarter following industry consolidation (it took just 12 months). Uber’s CFO recently said that Eats is already profitable in more than 100 cities, and that just 15% of bookings contribute half of its EBITDA losses in that segment.

Rationalisation is well under way and, in a few years’ time, this market will be no different to ridesharing. There will be one or two profitable players in each geographic market, and Uber will own more than a few of them.

I’d argue the permanently loss-making question was still open for debate at the time of Uber’s IPO in May 2019. But the steps taken in the 12 months since leave no room for doubt. Shareholders and management are committed to making money. They are on a very clear path to doing so.

Issue 4: How can you possibly buy Uber and call yourselves value investors?

This question perplexes me somewhat. It’s ok to buy Facebook at $190 a share now that it is profitable, but it wasn’t ok to buy it at $25 when it was losing money?

Uber is no different to any other investment we have made. We estimate how much it is worth, based on future cashflows the business is expected to generate, and compare that to the current share price.

The IPO price was $45 a share. At that price (and at that time), you needed a lot of growth and/or optimistic profit margins in the near future. You also had a lot of unanswered questions, particularly whether management’s focus on profitability was genuine.

We missed the bottom by a couple of days, but our entry price into Uber is approximately $23 a share. We have had a year of disposals, exits and improving margins. Governance and capital allocation gets a tick. And at half the price, the assumptions are a lot less heroic.

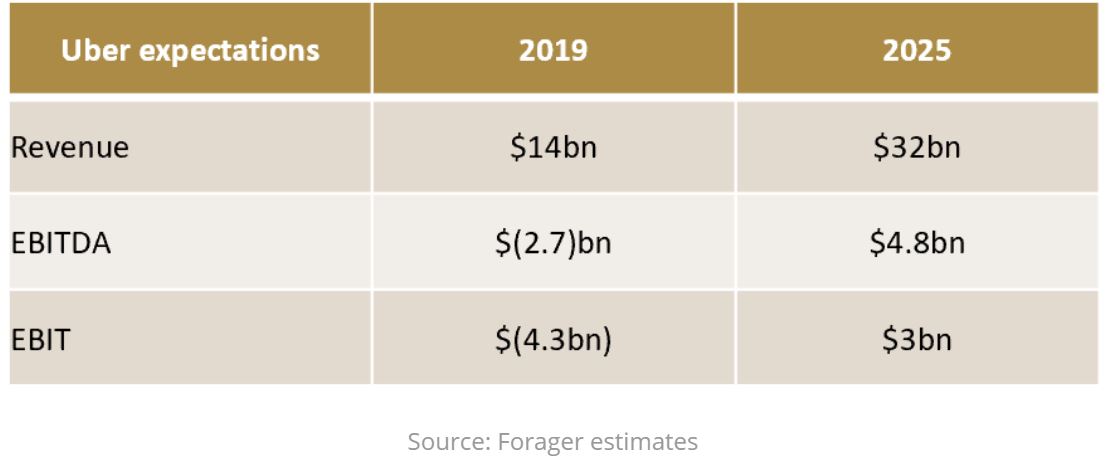

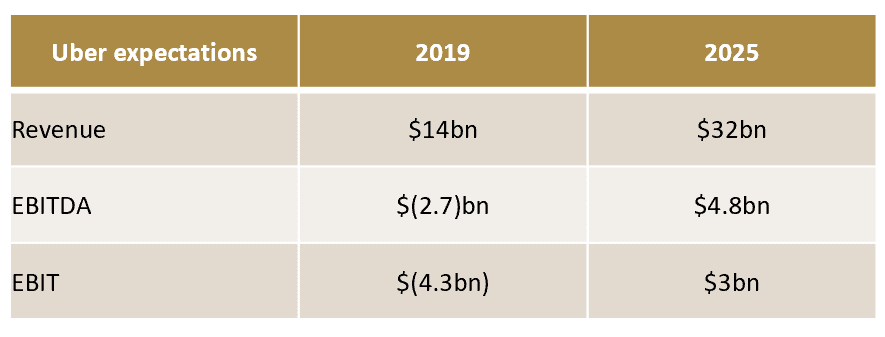

Here’s our base case. That $23 share price equates to a market capitalisation of about $40bn. Those minority shareholdings in Didi, Grab, Yandex and Zomato are worth $10bn, leaving us with a $30bn purchase price for the core Uber business.

Our expectation is that revenue will double over the next five years to more than $30bn. EBITDA margins will continue rising to 15% or more. That’s $4.8bn of EBITDA, from which we subtract $1.8bn of share based compensation and depreciation. We’re expecting at least $3bn of EBIT by 2025, flowing into the coffers as cash.

There is clearly a wide range of potential future outcomes. That’s why Uber is 3% of our portfolio, a relatively small weighting. But those are numbers you can hold us to. I expect the business to do better. And, if it is making $3bn of EBIT and still growing, it is going to be worth a lot more than $30bn in 2025.

A stock that people love to hate

None of this is wildly different to analyst expectations on the stock. Almost all investment banks have valuations of $40 or more. Which makes you wonder why it was selling for $23.

We’re about to experience a gigantic global recession and Uber’s Rides business will suffer accordingly. There’s one good reason. But I think it’s more than that.

The views of our critics are widely held. The perception is that Uber is an uneconomic business run by a nutter who is happy to lose money forever. I’ve engaged with a few of our clients who feel this way, and haven’t yet come across one who has read last year’s annual report.

It’s a view that was accurate three years ago. The fact that Uber has changed so much is where the opportunity lies.

If we’re wrong, we’re going to get crucified. That’s a risk I’m happy to take.

*All currency is USD unless otherwise stated

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and redemptions. Steve focuses on long-term investing in undervalued, underappreciated and sometimes unloved companies.

.jpg)

{kind=link}

3 topics

.jpg)

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management