This earnings season question: to virus-adjust earnings or not?

Very few companies are currently experiencing what could be regarded as a normal operating environment. Other than utilities and other providers of staple goods or services, companies are experiencing conditions dramatically outside what could be considered normal.

Most companies have been hit hard and have been experiencing trading levels well below normal, but some have actually been enjoying a tail wind, largely from increased online activity, pantry stocking, or healthcare spend. The consequence is that this earnings season is delivering a very high number of adjustments for the impact of the virus on trading over the past few months.

A question that sharemarket investors face, then, is to what degree should they incorporate the effects of Covid-19 into their valuation assessments. Those effects look like they will be present for years not months, but they are not forever.

For an investor, the long-term outlook should be more important. However, the sharemarket tends to place greater significance on near to medium-term numbers and trends than the long-term ones.

On the negatively affected side, they do not come much more affected than Auckland Airport. Last week’s full-year result was a sombre affair.

The international services that remain represent 3% of pre-Covid-19 levels while international retail is 0%. When you consider that about 90% of retail earnings came from the now-absent international travellers, you quickly get a sense of the hugely negative impact on revenues that Covid-19 is having on Auckland Airport.

Management is acting sensibly and responsibly by extending bank debt facilities, managing costs, and deferring the majority of planned capital expenditure projects. And, of course, cancelling the dividend. The result also included a $0.5 billion write down of the value of the retail and car park assets because of the lowered trading outlook, further underlining the gravity of the situation.

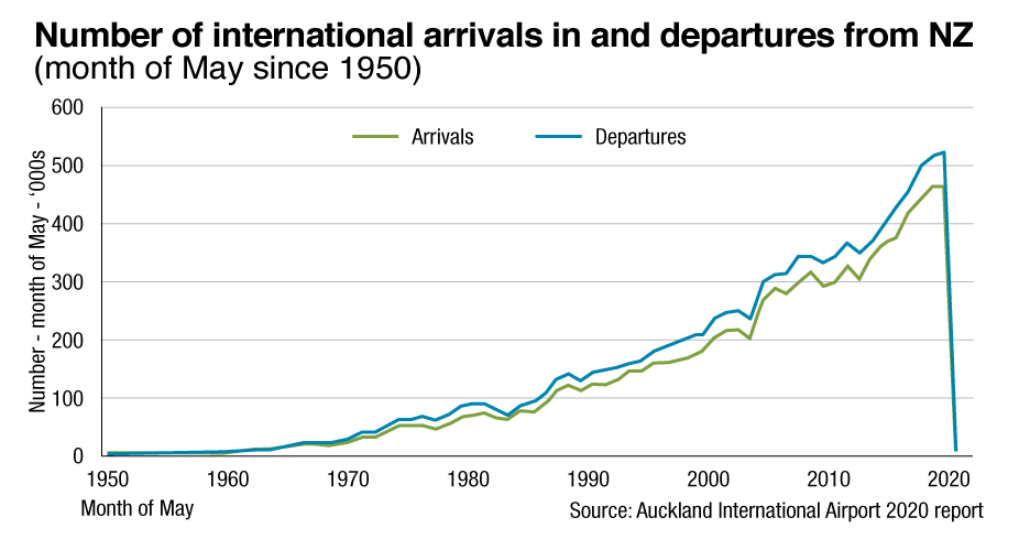

Overall, the current situation is neatly summed up by this chart that Auckland Airport released in its 2020 Annual Report.

So, with current earnings non-existent, investors must set aside the impacts of Covid-19 and look to future earnings to justify any share price over net tangible assets, which is currently about $4.50 per share. Management made it clear in their guidance that, in that case, “the future” is not next year or the year after.

In Auckland Airport’s result, management felt the International Air Transport Association (IATA) prediction of a recovery in global international flight volumes in three years’ time was optimistic in a New Zealand context. There was also a strong inference from the annual result commentary that a great deal hinges on the emergence of a trans-Tasman and Pacific travel bubble.

Basically, if that does not get up and running before June next year, Auckland Airport will be on track to breach banking covenants once again.

So, the fact that, on the day of this result, Auckland Airport shares traded up to close the day at $6.45, more than 40% above book value, is a very clear indication the majority of investors are discounting the effects of Covid-19 and are prepared to look through at least three, perhaps four, years into the future for decent earnings numbers. This may be a perfectly valid approach and one that might be expected to be a consistent theme across the sharemarket, as it weighs up this heavily Covid-19-adjusted earnings season.

Consistency, though, is not something the sharemarket is renowned for. Metaphorically speaking, while on one side of town investors are ignoring the short to medium-term effects of the virus, on the other side of town, they are embracing them as the new normal.

No better example of this was the response last week to the Fisher & Paykel Healthcare AGM trading update. Its clinical respiratory division is seeing a major spike in the demand for some of its products that are used in the treatment of Covid-19 patients who end up being hospitalised. Demand for its hospital hardware is seeing dramatic revenue growth, +390% versus the same period last year, while hospital consumable revenue also saw strong growth, up 48% on last year. These sales have been driven in large part by the recent resurgence in new virus cases in the United States that occurred as restrictions were relaxed too quickly.

Given that sales to hospitals account for nearly two-thirds of revenue, the growth in that division is driving significant earnings upgrades for the company. So much so that if the market were to strip out the virus-related boost to revenues and earnings, growth levels would drop to near negligible levels, given the very modest growth in the OSA division. This might infer that the introduction of an effective vaccine would see a very considerable reduction in sales of clinical consumables, which would lead to considerable downgrades as the Covid-19 adjustment unwound.

Overall, if the market was treating F&P Healthcare the same as Auckland Airport, assuming the Covid-19 effect will be temporary, it may well have traded down on its latest trading update, rather than its share price rising to $36.50, close to all-time highs. In a bull market all news is good news and in a bear market all news is bad news. This is unsustainable in the long run, but be careful, as John Maynard Keynes famously said, “the market can stay irrational longer than you can stay solvent”.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

........

Castle Point has taken all reasonable care in the preparation of these articles, however accepts no responsibility for any errors or omissions contained within. Past performance is not necessarily an indication of future performance. Opinions expressed in these articles are our view as at the date of issue and may change

4 topics

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Comments

Comments

Sign In or Join Free to comment