This isn't stimulus... it's compensation

Alex Cowie

Whether you think the pandemic was a black swan, a white swan or a pink one, the fact is that no one started 2020 with their portfolios positioned for a bowl of bat stew to trigger the worst quarter in 23 years. Nick Griffin from Munro Partners put it well:

"We did not see this coming. A virus developing from bats in Wuhan that would affect the world, and keep us all trapped at home... this was not in my outlook statement for 2020".

But as Greek philosopher, Epictetus wrote, "It's not what happens to you, but how you react to it that matters", and against a backdrop of ubiquitous market carnage, the quarterly gain of +7.6% Munro just posted suggests that Nick and the team have reacted rather well.

To hear how they managed that at a time like this, I tuned in to their recent webinar on 8th April and pulled out some of the gems for you below, including where they are investing now, what they expect from markets next and why you should view the stimulus as compensation.

When will we get to see Collingwood lose another Grand Final..?

A key point that Nick made was that the vast fiscal and monetary packages being rolled out globally do not represent stimulus but compensation aimed at bridging the growing chasm where the economy used to be. The scale of these packages have been astonishing, but the question is whether they will be enough. As Nick put it:

How big is the bridge? And I suppose this is the reason why we're still a little bit conservative, because the reality is, we just don't know how big the bridge is going to be. I think the best way to think about this is to think about how long is it going to be before I'm back at the MCG watching my beloved Collingwood lose another grand final... Ultimately all the money that comes in is probably not going to be enough to replace the money that's lost. So, it's a net negative. It's helpful, but it's not going to save you from a recession on the other side.

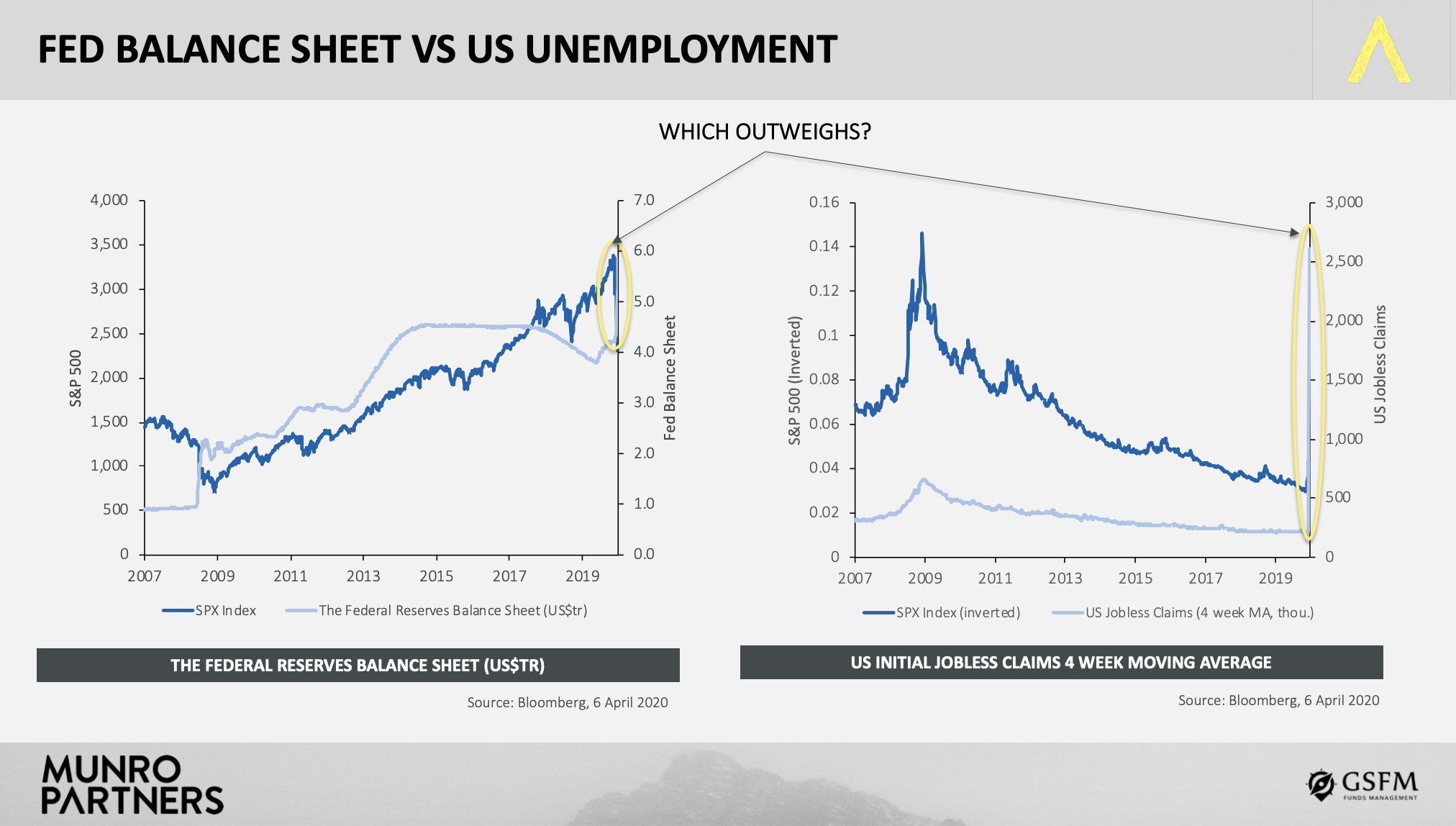

The chart on the left shows the Federal Reserve balance sheet versus the S&P 500 over time, and the one on the right is US jobless claims versus the U.S S&P inverted. The point illustrated here is that the diversion between the indices in the latter chart is far greater than that on the former chart, which together would imply the S&P500 could have a decent way to fall just yet.

Nick made the point that none of this liquidity solves the real issue, which is that this is a solvency crisis. Businesses are struggling to maintain revenue and stay afloat, and excess capital in this system doesn't fix that:

The fed and central banks are doing everything they can to provide liquidity to the market and the ability to access capital. But the problem is not liquidity, the problem is solvency. So, you have these huge jobless claims that far outweigh anything we saw in the financial crisis. And so, from that point of view, you can make money as cheap as you want, it's not really going to solve the problem for the economy here, because the problem is solvency. It'll lessen the blow, but it won't solve it.

Companies have already flocked to the equity capital markets to raise money to alleviate this issue, and this is expected to accelerate aggressively over the next few weeks. This will inevitably be dilutive to shareholders, and will likely put a firm lid on the market for now. Like the massive monetary and fiscal packages, these capital raises are just another form of life support designed to keep the patient alive, regardless of how unpleasant the side effects might be. Nick put it thus:

"...it's important to remember that as shareholders we are the last people that anyone is thinking about right now. These bailouts are to save jobs. These bailouts are to save businesses. They're not there to save shareholders.

Bear markets have a habit of making you look stupid

With over 20 years in markets, Nick has been through a few rodeos already and shared some of the lessons on bear market duration and timing here. With the market currently so fiercely divided into the bull and the bear camps, it's good to step back and remind ourselves that we are only 6 weeks into this, and that bear markets usually take far longer than that. Nick said:

This will be my third bear market and I'm just passing on lessons that I learned from people who told me about bear markets before them. Bear markets just have a habit of making you look really stupid... So, we do think there's a good opportunity to buy things here, we're just being a bit prudent about being fully invested, because these things generally drag out for a while.

He added that to be prudent, it pays to wait a few months for the confirmation that the bottom is in, as bull markets are long, so even missing the first quarter can still afford massive upside.

Even if you bought the last bull market three months after the bottom, there were still handsome returns to be made. And so from our point of view, the trick here is to not suffer from FOMO. The trick here is to be prudent and to be patient, because ultimately the bull market will come back and ultimately there'll be good times to be had again

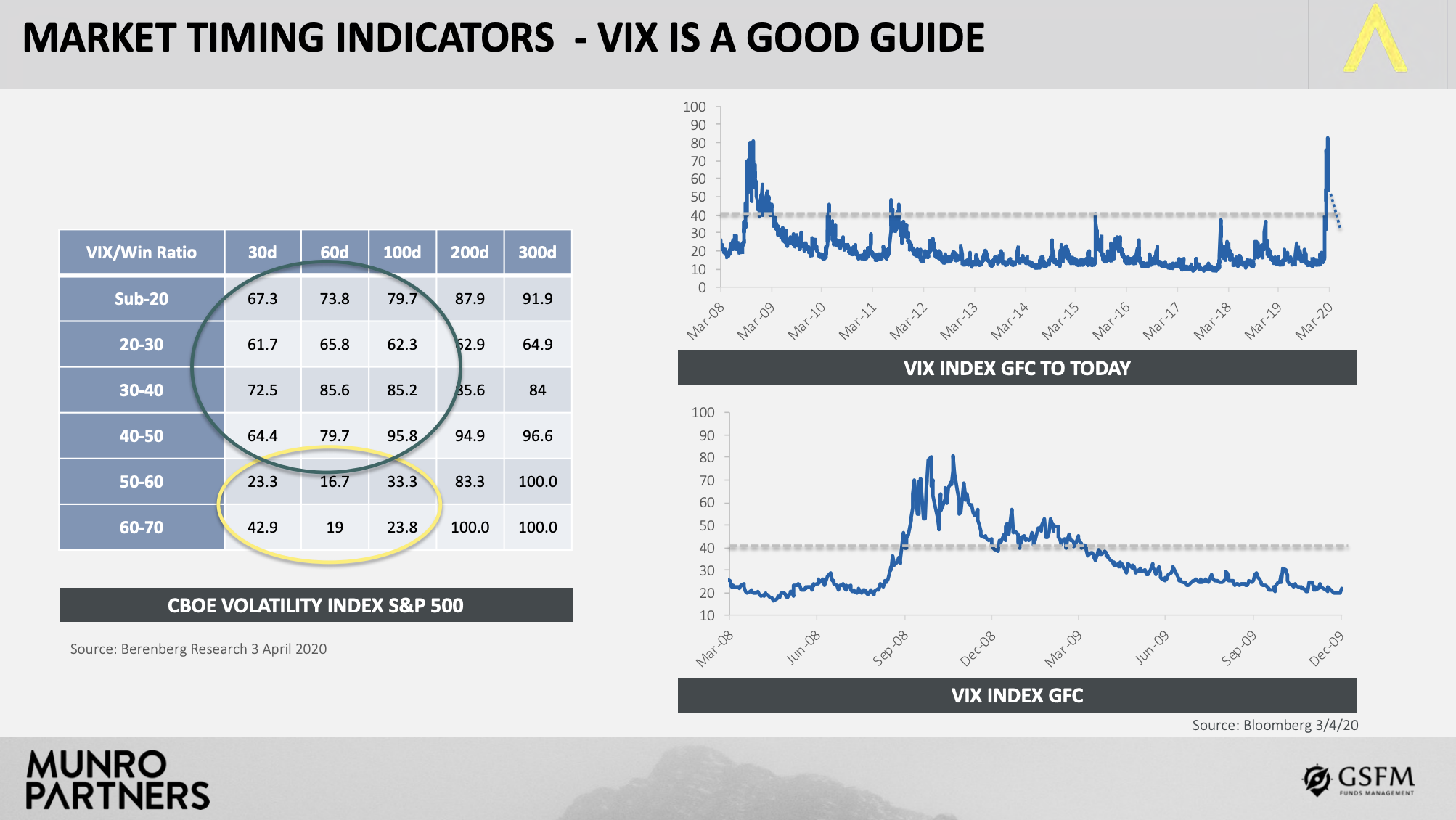

One really useful and simple tool Nick shared was the use of the VIX index as a timing tool. The data showed that by waiting for the VIX to settle down in the 30-40 range, or lower, (it is currently 38.8) sees the win ratio jump to 85.6 at 60 days, versus a VIX in the 60-70 range (it peaked above 80) where the win ratio is 16.7 days. By waiting for this confirmation, you may miss some of the gains, but you will reduce your risk significantly.

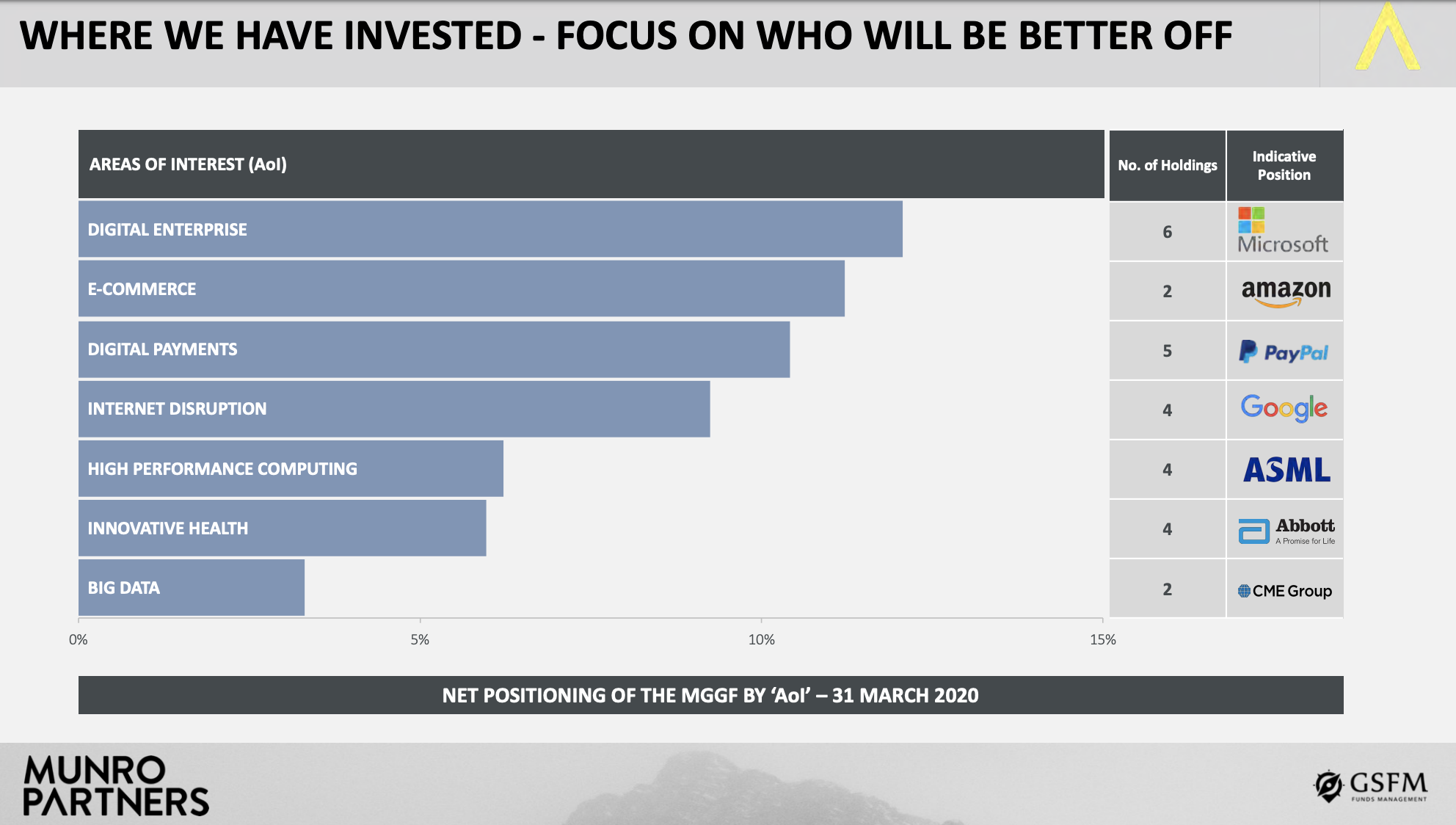

Where Munro is investing now

Nick emphasised one of his favourite mantras that: earnings growth drives stock prices. Pointing at the slide below he stated that every single company below should see earnings growth over the next three to five years.

On digital enterprise:

"We've got Microsoft and our other software companies. We talked about them a lot, we were already positioned with them going into this. If anything, the shift to the cloud will accelerate from here. I think we're all getting used to Microsoft Teams. All of our children moving to online learning. And so, the shift to the cloud, the shift to software, will accelerate".

On E-commerce

We've always thought you'd shift to e-commerce. If anything, this crisis means you shift faster. And so, from that point of view, Amazon and Alibaba are still good.

On digital payments

Digital payments will take a hit this year because commerce is slower, but ultimately the shift to digital will accelerate here, partly because you're going out less than second because cash is not necessarily hygienic anymore.

On high-performance computing

High performance computing semiconductors. Okay, so there's one thing I know about COVID-19, it gets solved with technology. The social distancing issue will be solved with technology. It will be solved with the internet of things and it will be solved with the cloud. And semiconductors are effectively the weapons manufacturers in the war here.

On healthcare companies

Clearly we're going to have to be more prepared on the other side of this. All of these companies were in the fund before the crisis hit. So all of these, we had strong structural views on before the crisis hit. If anything, we are happier now than we were pre the crisis. And so, we think their outlook actually looks better.

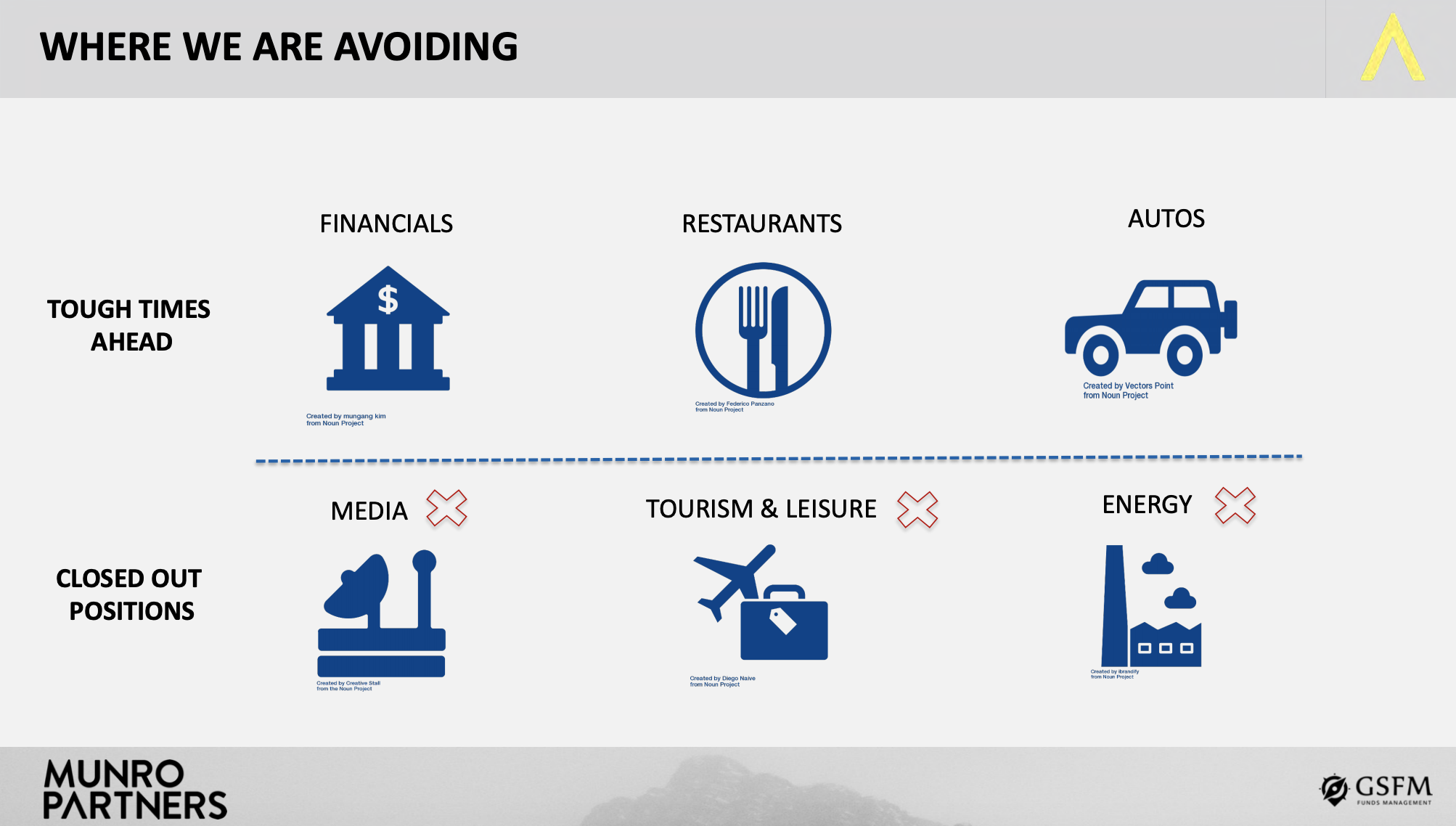

Areas they are avoiding

Nick touched on a few areas that the fund has already sold out on, which include aerospace and luxury goods, which is easy to understand given what has happened in both of those sectors.

Climate change investment is an area that the fund is passionate about, but they have mostly sold out from this as well. With many businesses drastically shrinking in size, hitting lower emission goals is not the stretch it once was.

On Energy

"We were short. What we thought would happen in 18 months happened in three weeks. We have closed out those positions. We still think it's challenged, but we wouldn't be in the long or short there".

On Tourism and leisure

We still think it's challenged. It's probably a great opportunity for the value managers and they're very good at digging around that, but it's not something we're going to be doing.

On financials

Main Street or small businesses or individuals are the ones who are going to suffer here the most. And so, there was this structural shift occurring and it's now happening faster. And so, it's the Main Street guys that are suffering. And so, ultimately that affects financials, which is an area that we have some selective shorts on at the moment.

On restaurant franchises

Unfortunately, these franchisees are going to get themselves into trouble and the restaurant labels have to bail them out.

On autos

They have dealers, the car companies are going to have to bail those guys out as well.

Strong gains in a time of crisis

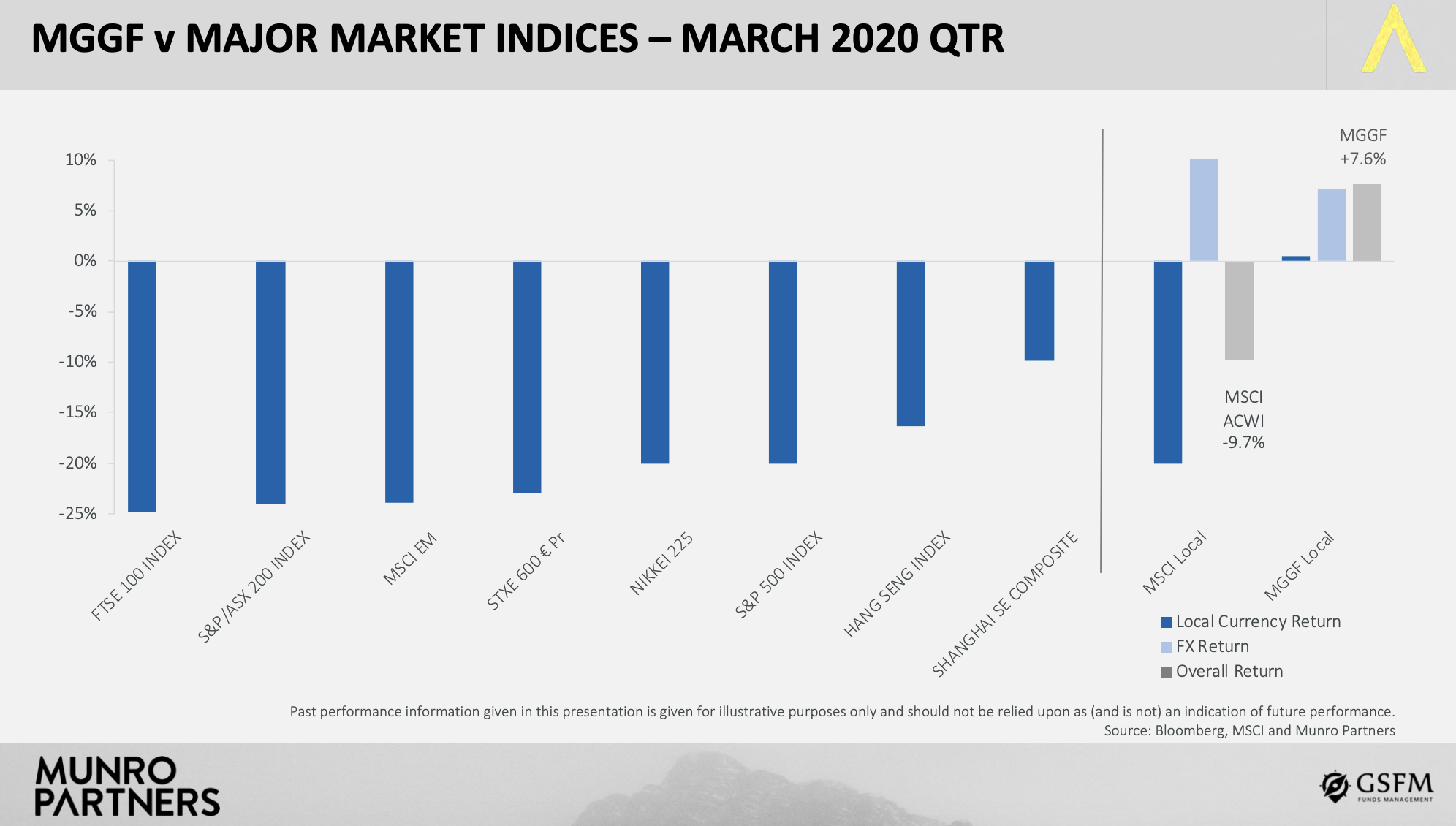

Given the March quarter was the worst one for markets for nearly a quarter of a century, with most markets losing more than 20%, Munro's gain of 7.6% for the quarter was quite remarkable, not least that this was done with a billion dollars of capital. I've summarised below how they achieved this.

While the long equity portfolio lost 12.6%...

Most stocks we held went down roughly 12.6% was the loss on our long equity portfolio. So, it was a lot less than the index, mainly because of the things like Amazon and Microsoft in the fund, but also because we observed our stop-losses on things like Airbus, or some of our luxury good companies, which we sold quite early on in the sell off, and so we did have some cash through that first quarter.

... the short portfolio and the hedging positions gained 13.1% between them...

One of the things that offset the losses was obviously the short equity return. So, shorts added 6.4% to return during the quarter. Our hedging returns from put options or futures that we use to hedge the underlying long only portfolio, added 6.7% return.

... and currency moves added 7.1%

And then foreign exchange added +7.1%. So, like the index we gained from FX, not as much, because we only had a roughly 55-60% US dollars through the period and the index is more 100% hedge.

There are only a handful of funds right now in the black for the year, and this highly unusual result has puts Munro in a somewhat unique position to capitalise on the opportunities ahead.

Find out more about Munro

Munro focuses on identifying and investing in companies that have the potential to grow at a faster rate and on a more sustainable basis than the peer group. To find out more, hit CONTACT below.

--

Disclaimer

The material contained in this publication is being furnished for general information purposes only as is not investment advice of any nature. The information contained in this document reflects, as of the date of publication, the views of Munro Partners and sources believed by Munro Partners to be reliable. There can be no guarantee that any projection, forecast or opinion in these materials will be realised. The views expressed in this document may change at any time subsequent to the date of issue.

This information has been prepared without taking account of the objectives, financial situation or needs of individuals. Before making an investment decision, investors should consider the appropriateness of this information, having regard to their own objectives, financial situation and needs.

Past performance information given in this document is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance. No representation or warranty is made concerning the accuracy of any data contained in this document.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Featuring

Nick Griffin,

Munro Partners

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has over 20 years of financial services experience and over 14 years managing absolute return mandates focused on global growth equities.

2 topics

1 contributor mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment