Three More Small Cap Recovery Stocks

After a strong rally the so-called ‘easy money’ has been made. From here, it is a stock pickers market as each business and industry is going to recover (and, for some, thrive) at different points in the cycle.

Following on from last month’s wire, here is 3 more small cap recovery stocks that look good value.

Prophecy International (ASX:PRO) - $45m Market Cap

PRO is a software company with a global presence riding two massive multi-year tailwinds – cyber security and the shift to cloud-based call centre operations.

Snare is PRO’s cyber security software product suite that provides cyber threat detection, security information & event management (SIEM) and centralised log management.

Clients of Snare include Fortune 500 companies, Federal & State Government departments, corporates and not for profits. It was originally developed by defence personnel for the defence industry and has its origins in open source software.

The market for cyber security was already growing rapidly prior to COVID-19 but the current environment has given it a massive boost.

Firstly, with more people working from home, IT systems are at greater risk of intrusion. Businesses and governments have been already been actively seeking ways to adapt to the new ways of working while maintaining adequate security.

And if they haven’t been proactive in sourcing the latest cyber security software themselves, they now have the government encouraging them to do so.

Last week ScoMo told all businesses to upgrade their cybersecurity to the latest available solutions after a "state-based actor with very, very significant capabilities" conducted a nationwide hack.

This is about to be channeled into strict rules and standards around minimum levels of cyber security required by businesses and organisations.

This saw the share prices of a number of ASX listed IT security companies rise strongly as it is almost certain to lead to a wave of new demand, but the market has yet to price in the potential benefit to PRO.

While the recent attack was isolated to Australia the problem is an international one and Snare has sales globally. We are going to see more frequent and more damaging cyber threats in future and products like Snare will continue to be in demand.

The other point worth noting is the release in late April of the new version of Snare Central. SIEM solutions can often be complex and difficult to manage or require specialized (and expensive) resources to do so. Snare Central solves this problem.

PRO have 3,500 Snare customers of which 400 already use Snare Central, which is an additional product. The latest version of Snare Central targets those Snare customers who don’t already have a centralized log management solution in place.

This is a potential US$10,000 upsell to those existing 3,100 Snare customers not already using Snare Central, or a US$30m opportunity in existing customers. Snare was already on track to deliver a record year and notwithstanding the short term interruption in March it is hard to see how that momentum slows down from here.

The other piece of the PRO story is eMite which is contact centre analytics software. This business has recently transitioned to a SaaS model, is majority recurring revenue and makes up just under half of PRO’s $15m annualised sales.

Two of the large players in this space are Amazon Connect and Genesys. Both are vendor partners for eMite.

Amazon Connect, which is Amazon’s cloud-based call centre platform, is the growth engine. I suspect if the market recognised that PRO’s growth was leveraged to the rapid growth of Amazon in this space, the stock would trade a lot higher on that basis alone.

The revenue model for eMite & Amazon Connect is volume based. The more minutes delivered over the platform the higher the revenue for PRO. So, the key metric to track is the growth of Amazon Connect.

And that business is booming.

The Amazon AWS CEO said this week about Connect:

“We launched it about three years ago in 2017 and it’s just gotten so big so quickly with companies like CapitalOne, Intuit, John Hancock, Citi Group, Johnson & Johnson, Hilton and Best Western, which is a really broad array of enterprises using it…It’s just incredible how many companies have spun up Connect to help them deal with all their calls from customers.”

This growth is intuitive. Call centre staff have been unable to work in tightly contained offices under current social distancing restrictions. Yet demand for call centre support for many businesses has been booming – just ask the army of day traders trying to call CommSec in March and April.

It should be noted that when a customer decides to shift from on-premise to cloud the migration of call volumes can take between 6-36 months as the call centres need to remain operational during the transition.

This means there is substantial embedded growth for eMite from recently won customers that have yet to hit a normal revenue run rate, but they will in time and it is likely that COVID has accelerated this.

Once on the Amazon Connect platform these customers won’t leave. That makes them very sticky for PRO too. COVID-19 has simply accelerated this shift to cloud-based operations.

Meanwhile, PRO remains completely under the radar to investment markets.

Revenue and cash profit was run-rating at annualised $15m & $1.5m at the first half, with roughly half of that revenue recurring and the stated outlook for further revenue and profit growth. Net cash was $4.6m at March 2020 (COVID update) and the company recently paid a dividend.

1H20 represents an inflection point in earnings where we should see strong operating leverage from here. The accounts are clean too, as all R&D spend is expensed.

With both products experiencing multi-year tailwinds and having strong market positions I think PRO can grow at c.20% per annum for the next 3-5 years. The cloud-based contact centre market itself is growing at 25% CAGR ($15b by 2021) and pretty much all segments of cyber security are growing at double digit rates.

In that context, 20% top line growth per annum should be achievable for a company starting from a relatively low base.

If they can achieve c.20% pa, then PRO should be generating $5-$10m EBITDA in 3-5 years. The excitement around these sectors are such that the market is likely to trade it on a lofty multiple, and that combination of earnings growth and multiple expansion would make the current price look like a bargain.

AMA Group (ASX:AMA) - $420m Market Cap

AMA is the largest smash repairer in Australia with last year’s transformational acquisition of Capital SMART putting daylight between AMA and their next largest competitor. This in a market that, for various reasons, is primed for consolidation and winner-take-most dynamics.

They raised money at $1.15 for this deal late last year, guiding to $100m+ of EBITDA once all synergies were achieved and with a long list of M&A opportunities that they began executing on immediately. The business has also been surrounded by interest from private equity, due to the attractive economics for the largest operator in this market.

But then COVID-19 hit and we were all told to stay at home. Road traffic plummeted and so did the number of car accidents and repair volumes for AMA.

AMA was heavily geared going into the crisis with $250m net debt. In a normal market with the business doing $100m+ of EBITDA that is comfortable gearing for a relatively recession proof business like this. But when revenue basically falls off a cliff like it did in March, it becomes worrying, and that saw the stock fall all the way to 15c.

Since then road traffic has increased and is almost back to where it was pre-crisis for Australia as a whole. It differs by state, as somewhere like Sydney seems to be above baseline levels while Melbourne (unsurprisingly) still remains well below.

AMA have provided a couple of recent market updates over the period stating that:

1) the company has the support of their bankers, which helped remove the concern around the debt and allowed them time to return to normal operating conditions. They have said there is no need to raise additional capital;

2) trading, while materially down, has been better than expected;

3) volumes are now improving significantly (in line with traffic data) and they expect it to return to normal levels by September this year.

On a recent conference call management said the business does about $100m EBITDA in a ‘normal year’ so you’d expect that run-rate to be achievable from September onwards based on their guidance. That works out to a PE of about 9-10x, which is too cheap.

Further, they recently renegotiated pricing with their major insurer customers and there is a substantial amount of synergies from the Capital SMART acquisition that kick in from 1st of July. Given the nature of that business (previously owned by SunCorp) there is good chance they’ll find more synergies over time.

The crisis forced AMA to lean down so they’ll emerge from this with a lower cost base. While volumes are almost back to normal the share price is still half where it was pre-COVID and I think this presents an opportunity.

The reason the stock is still cheap likely has to do with concerns around a second wave delaying the return to normal volumes. If that happens it is a real risk. But ScoMo continues to push the ‘we are open’ message and any ongoing fear or uncertainty around COVID increases the likelihood that commuters choose their car over public transport, which could actually lead to road traffic rising above baseline levels, as we’ve seen in a number of other countries.

Further, the company’s informal guidance of volumes returning to normal by September still leaves room for possible delays to opening up and I think leans towards being conservative given traffic volumes are already near baseline.

Directors have been aggressively buying this one for months, millions of dollars worth, so it could be a case of follow the money. And private equity interest in the business is unlikely to have disappeared. If a takeover emerged it wouldn’t be surprising at all.

There is always the chance of a capital raise to reduce debt and fund M&A (although note management have explicitly said no need to raise money here), but if it does happen it is likely to be strongly supported and with a growth focus as they consolidate the industry.

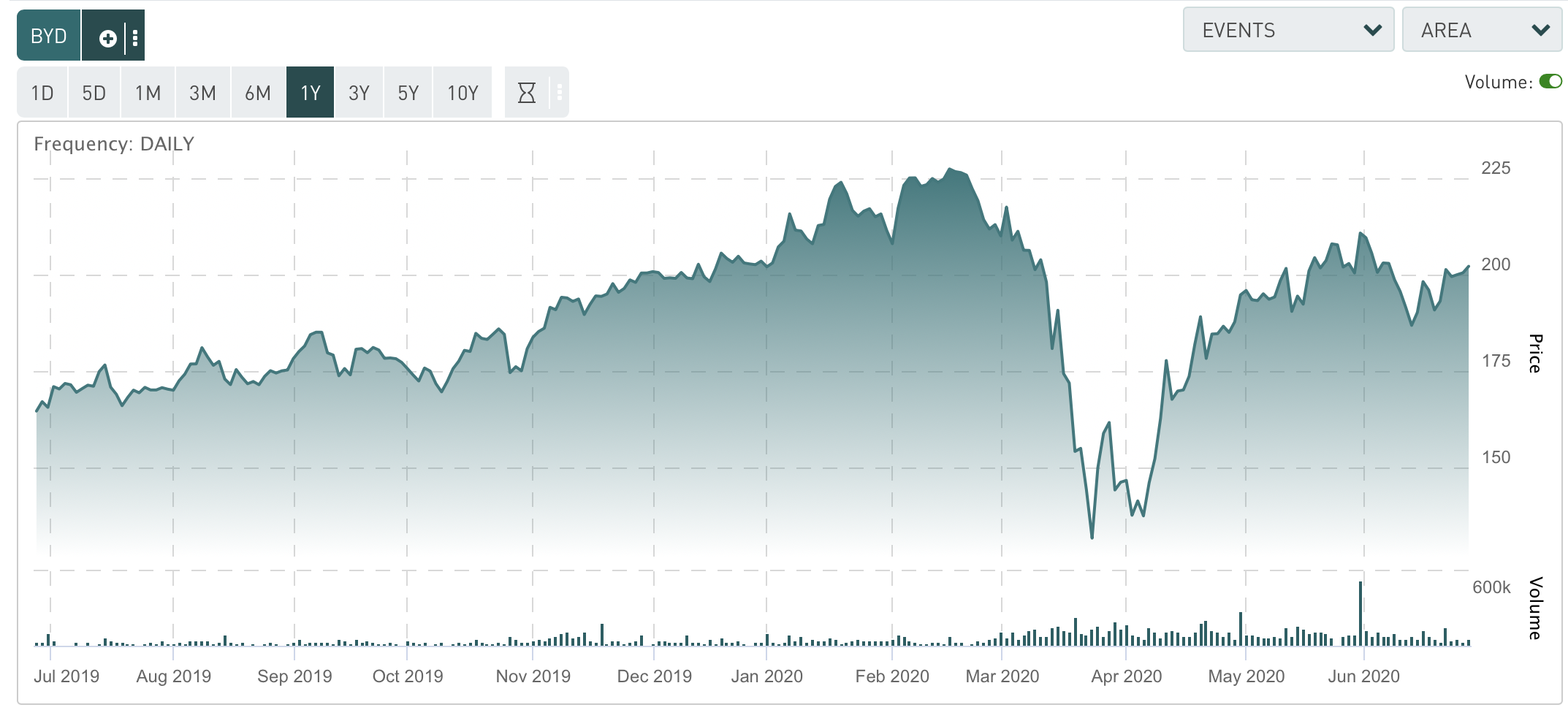

Boyd Group over in North America runs a very similar model to AMA and their share price (see below vs AMA) has recovered back to near all-time highs. I don’t see any reason why AMA can’t do the same in coming months.

MCS Services (ASX:MSG) - $3.5m Market Cap

MSG is a security & guarding company capped at a tiny $3.5m but with $25m of annual revenues, c.$2m net cash, self-funding and with a dominant position in WA (they service 85% of retail shopping centres). With organic growth likely to continue that provides a nice platform for M&A.

Capital H owns just under 20% of this company, so you should be aware that I am talking my own book here. We were also recently appointed corporate adviser. We are in it for the long haul.

I intend to explain our thesis in more detail at another time, but the basic summary is that MSG management have delivered a solid track record of growth since listing in 2015, with revenues growing from $15m to c.$25m today. That includes one bolt-on acquisition.

The MD owns just under 20% of the company himself, showing good alignment with shareholders.

They’ve emerged from COVID-19 in a healthy position. While event work dropped off (e.g stadiums and concerts) the core retail shopping centre work remained healthy and additional work for things like quarantine hotels bolstered the top line.

MSG know how to run a quality security operation and I think they have a real opportunity to expand their successful operating procedures into the much larger East Coast market where they now have John Portoglou, who has successfully built and sold security businesses, in charge of the Eastern States.

This expansion can be achieved either organically through leveraging relationships with the same clients on the West Coast that have larger operations on the East, or through M&A.

There is now a gap in the market for an Australian owned security provider with a national presence. All the majors – SNP Security, MSS, Wilsons & SecureCorp - are now foreign owned. It will no doubt take time and plenty of work but I don’t see any reason why MSG can’t grow to fill that gap.

In the context of the strategic value of their dominant position in WA, the c.$2m of cash on the balance sheet and the attractive platform for M&A, the market cap of $3.5m looked completely disconnected from true value, and we acquired a significant stake as a result. We have a good relationship with management and that led to us becoming more actively involved in trying to help grow the business.

So, don’t rush out and buy the stock just because we own it. But over the next 12-24 months put it on your watch list and see if MSG can deliver on the strategy, because if they do I believe the upside is substantial.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund.

Previously worked for Pie Funds and Bligh Capital.

........

The above is not financial advice. The author owns shares in PRO, AMA and MSG through the Capital H Inception Fund.

3 topics

4 stocks mentioned

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment